The British Virgin Islands’ Business Companies Act, 2004 (As Revised) (the “Act”) permits a company incorporated in a jurisdiction outside the British Virgin Islands (“BVI”) (a “Foreign Company”) to migrate to and continue operations in the BVI as a company incorporated under the Act if the laws of the foreign jurisdiction in which it is registered permits it to continue in another jurisdiction, including the BVI. This Legal Briefing summarises the key eligibility requirements and outlines the process for applying to continue as a company in the BVI.

Why Migrate to the BVI?

Migration (or continuation) allows a company to maintain its existing legal identity while changing its jurisdiction of incorporation. As a result, the company continues as the same legal entity and retains its name (subject to availability in the BVI), assets, rights, liabilities, and obligations. The advantages of migrating to the BVI include:

- there are no taxes on income, profits, or gains of the company or its shareholders in the BVI;

- the annual maintenance fees applicable in the BVI are very competitive when compared with many other jurisdictions;

- BVI laws afford more flexibility to facilitate a wide range of corporate, finance and investment transactions, for example in the digital assets space or fintech industry;

- BVI has a reputation as an international offshore financial centre and migrating there can enhance the company’s reputation, for example, as part of a fundraising effort or to consolidate, rationalize or reorganize a group structure under one BVI holding company.

What are the Pre Application Requirements?

Before submitting an application for continuation of the Foreign Company to the BVI, several statutory requirements under the Act must be satisfied:

- There must be no provision under the laws of the jurisdiction from which the Foreign Company is migrating which prohibits its continuation into the BVI. Evidence confirming permissibility under the applicable foreign law should be provided.

- The Foreign Company must not be subject to any pending liquidation or insolvency proceedings and must not be in liquidation in any jurisdiction.

- No receiver or manager must have been appointed over any of the Foreign Company’s assets.

- The Foreign Company must not have entered into any arrangement or composition with creditors which at the time of migration is unresolved.

- The Registrar of Corporate Affairs in the BVI (“Registrar”) must be satisfied that the continuation would not be contrary to the public interest.

What are the Key Provisions and Application Process?

The application to the BVI Registry of Corporate Affairs must include the following documents:

- a certified copy of the Foreign Company’s certificate of incorporation (or equivalent);

- the form of the BVI law compliant Memorandum and Articles of Association to be adopted;

- evidence that the application to continue and the proposed form of Memorandum and Articles of Association have been approved (i) by a majority of the directors (or other persons who exercise the power of the company), or (ii) in such other manner as may be established by the Foreign Company for exercising the powers of the Foreign Company; and

- evidence that the company is not prohibited from migrating to the BVI.

If the Registrar is satisfied that the requirements of the Act in respect of continuation have been complied with, upon receipt of the documents listed above, the Registrar will then:

- register the documents;

- allot a unique number to the company; and

- issue a certificate of continuation in the approved form to the company.

A certificate of continuation issued by the Registrar is conclusive evidence that: (i) all the requirements of the Act as to continuation have been complied with; and (ii) the company is continued as a company incorporated under the Act under the name designated in its Memorandum of Association on the date specified in the certificate of continuation.

What is the Effect of Continuation?

When a Foreign Company is continued under the Act:

- the Act will apply to the company as if it had been incorporated originally under the Act after the date upon which the continuation is approved;

- the company is capable of exercising all the powers of a company incorporated under the Act;

- the company is no longer to be treated as a company incorporated under the laws of a jurisdiction outside of the BVI; and

- the Memorandum and Articles and Association adopted and filed under section 181(1) of the Act become the Memorandum and Articles of the company

The continuation of a Foreign Company under the Act does not affect:

- the continuity of the company as a legal entity; or

- the assets, rights, obligations or liabilities of the company

It is also important to note that:

- no conviction, judgement, ruling, order, claim, debt, liability or obligation due or to become due, and no cause existing, against the company or against any member, director, officer or agent thereof, is released or impaired by its continuation as a company to the BVI under the Act; and

- no proceedings, whether civil or criminal, pending at the time of the issue by the Registrar of a certificate of continuation by or against the company, or against any member, director, officer or agent thereof, are abated or discontinued by its continuation as a company under the Act, but the proceedings may be enforced, prosecuted, settled or compromised by or against the company or against the member, director, officer or agent thereof, as the case may be.

- all shares in the company that were outstanding prior to the issue by the Registrar of a certificate of continuation are deemed to have been issued in conformity with the Act.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Briefing, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E. elizabeth.kenny@loebsmith.com

E: vanisha.harjani@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

The rapid advancement of artificial intelligence (AI) continues to raise complex questions about the applicability of intellectual property (IP) laws to AI and AI-generated works.

IP remains one of the leading and most contentious issues in respect of AI governance. AI adoption continues to grow, and this year is already showcasing a wider range of commercial applications across all sectors. In light of the IP related challenges, businesses leveraging AI technologies must strategize to navigate the evolving intellectual property landscape. As the legal framework around AI continues to develop, businesses need to ensure that they avoid copyright infringement while also effectively safeguarding their own IP assets. Developing a clear understanding of how existing laws apply to AI technology and staying updated on legal developments will be crucial for companies seeking to innovate responsibly and protect their intellectual property in an AI-driven economy.

How is Intellectual Property protected in the Cayman Islands and the BVI?

Copyright protection in the BVI (for “qualified persons”) and in the Cayman Islands (for “qualifying persons”) is automatic when such person creates an original work (once the work is recorded, in writing or otherwise) such as sound and music recordings; films; when you write a book or poem; or when you develop new software. By virtue of the Copyright (Cayman Islands) Order 2015 and Order 2016 (as amended), Part 1 of the U.K.’s Copyright, Designs and Patents Act 1988, subject to certain exclusions and modifications, was extended to the Cayman Islands. The BVI has implemented its own legislation in the form of the Copyright Act (Revised 2020) which is very similar.

Patent protection in the two jurisdictions is quite similar. As it is in other jurisdictions, in order to get patent protection, the invention must be: (i) new – i.e. the first in the world, (ii) useful – i.e. the invention must serve a purpose or provide a solution, and (iii) inventive – i.e. the invention must not be obvious to persons in the industry in which the invention is intended to be used.

Both the BVI and the Cayman Islands allow for the indirect registration of patents. Once a U.K. patent is granted, an application can be made in either of the Cayman Islands or the BVI to extend the scope of protection. In the Cayman Islands, there is no deadline for the filing of the application to extend rights, whereas in the BVI, rights must be extended within three years from the date of issue of the UK patent.

AI-generated works, AI-inventions and other AI-outputs and infringement

IP laws are designed to protect human creations. Generative AI (AI which generates text, images, speech, video or technical inventions based on user-inputted instructions) continues to increase in capability and grow in adoption. However, most copyright and patent laws, for example, do not yet explicitly address AI’s role in authorship or inventorship, leaving a legal void requiring attention. Traditionally, the author or inventor is the person or organisation that creates the works. If now AI is responsible for content creation autonomously without any human input, the question is who owns the copyright protecting such content.

- For countries, such as the UK, this may be answered by the fact that computer-generated works will be owned by the person who made the necessary arrangements for the creation of the work.

- An overwhelming view in the E.U. is that AI cannot be a legitimate author. However, specific ways of using AI may result in a work that is protected for the user.

How does Artificial Intelligence affect Intellectual Property Protection?

We expect to see governments across the world grappling with balancing strategies aimed at encouraging the development of AI and innovation while, at the same time, attempting to modernize IP and AI legal frameworks to account for AI.

Training generative AI involves using large bodies of IP-protected works/ data in ways that may be infringing under current laws. Governments seeking to “unlock” the potential of generative AI are now more often looking to legislate to permit text and data mining (TDM) of IP-protected data in order to train AI. The intellectual property in the data used to train AI models is growing as a subject of legislative discourse and is now a key issue in matters that have flooded courts across the world, whether use of copyright-protected materials to train AI models infringes copyright.

Training AI using personal data or protected IP also provides challenges to legislators worldwide. Over the next 2-3 years we expect to see increased regulatory scrutiny of companies that create or use AI technologies which have been trained using (i) personal data and/or (ii) information/data protected by IP rights. Regulators worldwide are now paying greater attention to balancing the benefits of AI against concerns about personal data and the protection of IP, and we expect that this will continue in the next few years.

Copyright

AI programs usually qualify as IP with software or computer programs being literary works. In some countries however, copyright protection will not apply for functional aspects of AI such as algorithms or system designs. AI systems function however by processing human-provided instructions to generate problem-solving outcomes. This capability makes AI-based programs highly valuable from an IP perspective, as their innovative nature and diverse utility underline their significance of IP protection.

Who owns the copyright?

Copyright laws often require that there must be a natural person to whom copyright can be attributed and many jurisdictions including the Cayman Islands and the BVI, do not provide for “computer generated” works where no human author is involved. This creates a gap in the protection of AI-generated works, which are typically produced autonomously with little or no human intervention. Many copyright laws also require that “sufficient effort” must be expended to make any literary, musical, or artistic work original in character – which involves time, human labour, and skill. What constitutes sufficient effort for AI-generated content remains largely untested, raising debates about whether crafting prompts or editing AI output meets the thresholds. Additionally, if non-human entities are recognized as “authors” then copyright duration may become complex. Generally, copyright protection is granted for an author’s lifetime plus a period of time following, potentially leading to indefinite protection for AI-generated works.

The duration of copyright protection in the Cayman Islands varies depending on the nature of the work at issue. For example:

- For Literary, Dramatic, Musical or Artistic Works: copyright expires at the end of 70 years from the end of the calendar year in which the author dies. However, if the author is unknown, copyright expires at the end of 70 years from the end of the calendar year in which the work was made or first made public

- For Computer Generated Literary, Dramatic, Musical or Artistic Works: copyright expires at the end of 50 years from the end of the calendar year in which the work was made.

- For Sound Recordings: copyright expires at the end of 50 years from the end of the calendar year in which the sound recording was made or first made public.

- For Films: copyright expires at the end of 70 years from the end of the calendar year in which the film/movie was made or first made public.

- For Broadcasts: copyright expires at the end of 50 years from the end of the calendar year in which the broadcast was made.

Copyright Protection and Deepfakes

Most IP laws are ill-equipped to address the challenges posed by digital replicas or deepfake technology. Copyright law generally is not fit for purpose in respect of deepfakes as the source material for many deepfakes either falls outside the scope of copyright protection or the copyright owner is not the individual who is harmed by the infringement. Possible causes of action presented by deepfakes include (1) copyright infringement (if a deepfake involves unauthorized use of copyrighted material), (2) trademark infringement (if it uses a registered trademark without permission), (3) the tort of passing off (if it misrepresents a product or service as endorsed by a well-known individual), (4) personal data privacy violations or (5) defamation (if the content defames an individual). The issue of whether the outputs of AI models – particularly where they substantially reproduce source materials – may infringe copyright and who may be responsible for such infringement, is also unresolved.

Is the person who infringed: the user of the AI generated work without the rights holder’s consent or the AI developer or AI system owner? This ambiguity poses risks for businesses. If there is no clear proprietary right in AI-generated works, businesses may be exposed to unnecessary risk.

AI programs usually qualify as IP with software or computer programs being literary works. In some countries however, copyright protection will not apply for functional aspects of AI such as algorithms or system designs. AI systems function however by processing human-provided instructions to generate problem-solving outcomes. This capability makes AI-based programs highly valuable from an IP perspective, as their innovative nature and diverse utility underline their significance of IP protection.

Fair dealing exceptions

With respect copyright infringement, some jurisdictions such as the Cayman Islands, BVI, U.S., U.K., Australia, Hong Kong and Singapore provide fair dealing exceptions for particular activities, despite the fact that many other jurisdictions do not.

Under Cayman Islands law and BVI law, some of the fair dealing exceptions permitted are:

- Personal copying for private use

- Non-commercial research and private study

- Text and data mining for non-commercial research

- Criticising, reviewing and reporting current events

- Use for parody, caricature and pastiche

- Making backup copies, de-compilation, observing, testing and studying, and correcting computer programme errors.

Patents

Who is the inventor? Will the requirement for “novelty” remain?

Many patent laws require the inventor to be a natural person. This requirement could exclude AI from being independently recognized as an inventor. AI-driven innovations, such as those involving algorithms and machine learning processes, face challenges in meeting the criteria for protection as an invention. Under US patent law, for example, absent at least one human inventor, an invention is not patentable. Also, the criteria for patentability in many jurisdictions (including the Cayman Islands and the BVI) usually involves requirements for novelty, an inventive step and industrial applicability. These criteria raise questions about whether AI-generated inventions can ever meet the inventive step requirement, traditionally linked to human ingenuity. AI relies on algorithms and datasets to mimic human cognitive functions, enabling it to generate patentable inventions.

We expect to see a continuing updating of guidance as to the level and type of human contributions that are necessary to support patentability as new cases make their way through courts in various jurisdictions. A vital question that arises is whether AI can be regarded as a legitimate author of content that it generates or an inventor in case of patents, given the want of legal personality of the AI itself.

AI-Driven Entity – Cayman Islands Foundation Company

A particularly effective legal structure for an AI-driven entity is the Cayman Islands foundation company. Such foundation companies do not require shareholders, allowing them to function with a governance model that can be tailored to an AI’s decision-making models. Key advantages of using such foundation companies include the following.

- Legal recognition: foundation companies can provide a defined legal entity that can interact with traditional financial institutions, sign contracts and meet compliance obligations.

- Decentralised governance: the ability to structure the foundation company without shareholders allows for governance mechanisms that can adopt smart contract-based decision-making or AI-driven decision-making.

- Asset protection and Tax mitigation: foundation company can be tax resident in the Cayman Islands, hold and manage assets and ensure legal clarity in asset ownership.

- Regulatory compliance: foundation companies can be designed to comply with regulations, including AML and CFT requirements, making them suitable for global transactions.

- Economic substance rules: foundation companies limited by guarantee are specifically exempted from the economic substance rules and can therefore hold and even make profits from intellectual property without coming under the relevant economic substance compliance regime.

This publication is not intended to be a substitute for specific legal advice or a legal opinion. For specific advice on the matters covered above, please contact your usual Loeb Smith attorney or any of the following:

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: vanisha.harjani@loebsmith.com

E: edmond.fung@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

E: yun.sheng@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

I. What is a VISTA Trust?

A VISTA trust is a special type of trust established pursuant to the Virgin Islands Special Trusts Act, 2003 (as amended) (“VISTA“), being a trust regime specifically designed for holding shares in British Virgin Islands (“BVI“) companies. VISTA came into force on 1 March 2004, primarily to address the structural impediments faced by traditional BVI trusts when holding shares in family businesses. It is important to note that the direct assets of a VISTA trust are, and can only be, the shares in the underlying BVI company. The design of the VISTA trust regime is therefore centered upon this kind of asset class.

II. Overview and Legislative Background of VISTA Trusts

To appreciate the value of the VISTA regime, we must first understand a fundamental tension inherent in the traditional trust structure under common law. English trust law has long recognized a fiduciary standard known as the “prudent person of business rule”. This standard requires a trustee to supervise and manage trust property as a prudent business person would manage their own affairs. This means that, under a traditional trust, the trustee owes a duty to diversify investments, avoid speculation, and continuously monitor investment performance. Where the principal assets of the trust comprise a controlling shareholding in a family business, a trustee may, by virtue of its duty to diversify risk and pursue stable returns, be compelled to dispose of the family business shares or, out of concern for compliance, to prevent the company from engaging in speculative or hazardous investment activities.

This directly conflicts with the settlor’s desire to preserve the family business as a legacy asset to be held over the long term. The VISTA trust resolves this conflict by establishing, at the legislative level, a safe harbour that permits the trustee to adopt a “passive holding” role.

III. What are the Key Distinctions Between VISTA Trusts and Traditional BVI Trusts?

As noted above, the VISTA trust alters the role of the trustee as conceived under traditional trust law. In a traditional BVI trust structure, the trustee enjoys broad powers of administration over the trust assets, including the duty to actively supervise the conduct of the underlying BVI company’s business, to intervene where necessary, and to dispose of trust assets in the best interests of the beneficiaries. Under the VISTA trust regime, the trustee’s role is transformed from that of an active manager to that of a custodian of the trust assets, with the trustee owing, in principle, no fiduciary responsibility or duty of care in respect of the affairs of the BVI company whose shares are held in the trust.

The VISTA regime applies only where the trust deed expressly directs that it shall apply, and it affects only the administrative duties of the trustee, leaving the beneficial provisions unaffected. VISTA may therefore be combined with various forms of beneficial arrangements, including discretionary trusts, life interest trusts, purpose trusts, and reserved powers trusts.

Compared with traditional trusts, VISTA trusts are more closely aligned with the expectations of modern entrepreneurs regarding family wealth succession and the manner in which trust assets are to be managed.

IV. What are the Core Legal Mechanisms of VISTA Trusts?

1. Primacy of the Duty to Retain Shares. The VISTA regime establishes a statutory rule within the trustee’s duty framework that takes precedence over other obligations. Specifically, the trustee must treat the “continued retention of the BVI company shares” as its core duty, and the performance of this duty is expressly accorded priority over any other general duty to preserve or enhance the value of the trust property. In other words, even if, from a purely commercial perspective, a sale of part of the shareholding would optimise asset allocation or generate higher returns, the trustee has no power to dispose of the trust shares on such grounds, unless the trust deed expressly reserves a specific power of disposal to the trustee by way of explicit provision.

2. Non-Intervention by Trustee. Except as otherwise provided in the trust deed, the trustee must not exercise voting rights or any other powers to intervene in the management of the company or the conduct of its business. The trustee owes no fiduciary duty or duty of care in respect of the assets of the company or the conduct of its affairs. The operation and management of the company rest entirely with its board of directors.

3. Office of Director Rules. The trust deed may contain detailed “Office of Director Rules”, which set out precisely how the trustee is to exercise voting rights to appoint and remove directors and to determine directors’ remuneration. The settlor may, through such rules, control the composition and operation of the company’s board of directors, and the trustee must strictly adhere to these rules when exercising its voting rights.

4. Intervention Call. While, as explained above, the trustee of a VISTA trust may not, broadly speaking, actively intervene in the management of the BVI company, the regime does not entirely preclude trustee intervention. The trustee is obliged to investigate a complaint and, if satisfied that it is well-founded, to take appropriate action only where an “interested person” makes an intervention request based on “permitted grounds for complaint” as set out in the trust deed. The scope of interested persons is determined in accordance with the provisions of the trust deed and may include beneficiaries of the trust, a protector with supervisory powers, an enforcer of a purpose trust, and an “appointed enquirer” designated by the settlor through a special authorisation mechanism.

V. What are the Essential Requirements for Establishing a VISTA Trust?

1. Core Parties

Like traditional trusts, a VISTA trust comprises three core parties: the settlor, the trustee, and the beneficiaries. It is noteworthy that the trustee of a VISTA trust may be either a (i) BVI licensed trust company, or (ii) a private trust company (“PTC“). While VISTA trusts typically appoint a licensed trust company as trustee to satisfy the trustee requirements under the VISTA legislation, following the enactment of the BVI Financial Services (Exemptions) Regulations, 2007 (as amended) (the “PTC Regulations“), the use of a PTC has become an increasingly common choice in VISTA trust structures. The PTC Regulations exempts a PTC from the requirement to obtain a trust license under the BVI’s Banks and Trust Companies Act, 1990 (as amended) (the “BTCA”). The key advantages of a PTC are:

(i) lower costs compared with engaging a professional licensed trust company; and

(ii) the ability for the settlor to enhance control over the trust by establishing a PTC. For example, the settlor and his/her family members may serve on the board of directors of the PTC, thereby participating substantively in decision-making at the trustee level and achieving comprehensive control over the governance of the trust.

Additionally, the settlor may appoint a protector of the trust. The protector primarily serves a supervisory and safeguarding role in respect of the trustee’s administration of the trust, and the trust deed may even confer upon the protector the power to appoint and remove trustees. As regards beneficiaries, a question often raised by settlors when establishing a trust is whether they themselves may also be a beneficiary. The answer is yes, provided that the settlor is not the sole beneficiary of the trust.

2. Trust Deed

The core document of a VISTA trust is the trust deed entered into between the settlor and the trustee, which sets out matters including the manner in which the trust assets are to be administered, the classes of beneficiaries or the mode of beneficial entitlement, and the manner in which the trustee may be appointed and removed. A trust deed of VISTA trust must be in writing and must state that this trust is a VISTA trust. The trust deed may also be created by will.

VI. What are the Key Advantages of VISTA Trusts?

1. Retention of Control. The settlor may, by virtue of the legal mechanisms of the VISTA trust, retain a certain degree of control over the trust. By serving as a director of the BVI company to be settled into the trust or by designating the composition of the board through Office of Director Rules, the settlor may, following the transfer of the BVI company shares into the trust, continue to retain effective control over the operation of the company. The VISTA trust builds upon this foundation by providing, through dedicated legislation, a response to the particular needs of family business succession.

2. Asset Protection. The BVI Trustee Act (2020 Revision) contains comprehensive “firewall” provisions, which also apply to VISTA trusts and serve to protect the trust from the impact of foreign laws (such as forced heirship rules, or claims arising from marriage or civil partnership). All matters relating to the validity, interpretation, and administration of the trust are governed exclusively by BVI law.

3. Avoidance of BVI Probate. Once the shares of a BVI company are validly settled into a VISTA trust, they are held by a trustee, meaning they are no longer considered part of the settlor’s personal estate upon his/her death, and will pass directly to the beneficiaries in accordance with the provisions of the trust deed, without the need for BVI probate proceedings, thereby avoiding the protracted and complex process of probate.

4. Holding High-Risk Assets. As the prudent person of business rule does not apply to VISTA trusts, the trust may hold shares in companies engaged in high-risk activities without the trustee being required to diversify investments or to intervene on prudential grounds, and the trustee is thereby absolved of potential legal liability arising from holding such assets.

5. Exclusion of the Rule in “Saunders v Vautier”. VISTA permits the exclusion of the rule in Saunders v Vautier (the common law rule whereby beneficiaries, if all sui juris and absolutely entitled, may unanimously agree to terminate the trust) for a period of up to 20 years, providing additional safeguards for long-term family asset planning. Furthermore, the statutory perpetuity period for a VISTA trust is up to 360 years, rendering it suitable for multi-generational succession planning.

6. Tax Treatment. As with traditional BVI trusts, VISTA trusts are not subject to BVI capital gains tax, inheritance tax, or income tax. It should be noted, however, that whether trust distributions to beneficiaries are subject to tax will require case-by-case consideration by reference to the particular tax residence status of the beneficiary.

VII. What are the Common Uses of VISTA Trusts?

As noted above, the assets of a VISTA trust are shares in a BVI company. However, through appropriate structuring of the shareholding chain, a settlor may, via a VISTA trust, indirectly hold equity interests in other offshore companies, thereby achieving global asset structuring. Accordingly, in light of the principal advantages of VISTA trusts outlined above, such trusts are broadly suited to the following applications:

(1) intergenerational succession of family business shareholdings, enabling shares to be held in trust so as to avoid probate;

(2) holding high-risk investment portfolios, where the non-intervention principle applicable to the trustee effectively reduces the friction costs that might otherwise arise from a trustee pursuing overly conservative investment strategies; and

(3) serving as the top-tier holding structure within a listing structure. Through the establishment of a trust structure, the VISTA trust holds a BVI company which, in turn, acts as a holding company through successive layers to hold the shares of an underlying entity intended for listing.

VIII. Conclusion

The VISTA trust, through legislative innovation, achieves a delicate balance between the fiduciary duties of the trustee and the settlor’s desire to retain control. For modern entrepreneurs who wish to pass on their family business as a core legacy asset across generations while retaining decision-making authority over its operations, the VISTA trust offers a solution that combines legal certainty with operational flexibility.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Briefing, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E. elizabeth.kenny@loebsmith.com

E: vanisha.harjani@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

E: yuri.zhang@loebsmith.com

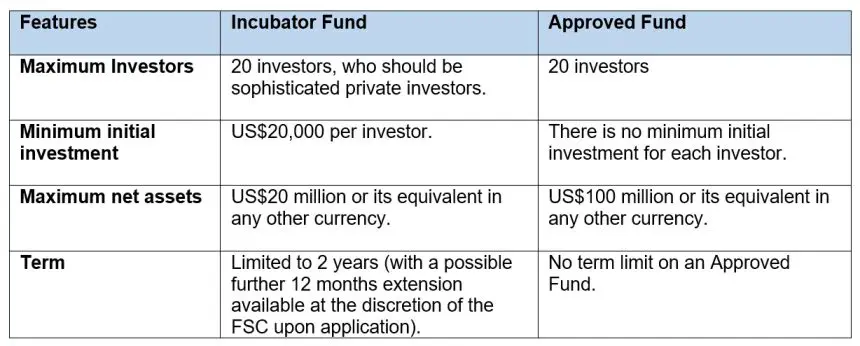

Among the many investment fund structures provided by the Financial Services Commission (“FSC”) of the British Virgin Islands (“BVI”) under the Securities and Investment Business Act (As Revised) of the BVI, Approved Funds and Incubator Funds have for a number of years been very attractive options for Start-up Fund Managers and Emerging Fund Managers. Introduced in 2015 by the BVI’s Securities and Investment Business (Incubator and Approved Funds) Regulations (the “Regulations”), these two open-ended fund structures offer reduced regulatory burden and lower operational costs for Fund Managers to test their investment strategies and abilities. Recognising the inherent limitations of these two fund structures, there are built-in provisions in the Regulations that allow for and facilitate conversion into more robust fund structures (i.e. Private Fund or Professional Fund) upon specific trigger events.

In our previous Legal Briefings, we have discussed in detail the key features and benefits of Incubator Funds and Approved Funds Key Features and Benefits of the BVI Incubator Fund | Loeb Smith, Key Features and Benefits of a BVI Approved Fund | Loeb Smith. As a recap, we set out below the key features of these two categories of BVI funds.

Trigger Events for Conversion

Trigger events are directly linked to the key features of these funds. For an Incubator Fund, the most common triggering event for conversion is the expiration of its Term. At the end of the initial 24 months (“Validity Period”) of the Term, there is a decision to be made in terms of whether the Incubator Fund wishes to terminate its business or continue operation as an investment fund. The other triggering events include (i) the total number of investors close to exceeding 20 and (ii) the net assets exceeding US$20 million over a period of two consecutive months.

For an Approved Fund, as there is no limit on the Term for the Approved Fund, the only triggering events for conversion are the total number of investors exceeding 20 or the net assets exceeding US$100 million over a period of two consecutive months.

When and how to apply for conversion?

Incubator Fund

Upon occurrence of a triggering event, if the Incubator Fund decides to continue its operation as a mutual fund, an application for conversion must be submitted by the Incubator Fund to convert into and be recognised as a Private Fund or a Professional Fund or be approved as an Approved Fund either at least 2 months before the expiry of its Validity Period, or within 7 days after the end of the second month where its number of investors or the net assets exceed the threshold.

In the application, the Incubator Fund should:

-

-

- complete the application form and submit the updated fund documentation for the Fund to be recognised as a Private Fund or a Professional Fund or be approved as an Approved Fund;

- if the Incubator Fund intends to be converted into a Private Fund or a Professional Fund, prepare and submit to the FSC an audit of its (i) current financial position; and (ii) compliance with the requirements of the Regulations. The aforesaid audit should be performed by either a person approved by the FSC under SIBA or pursuant to section 56 of the Regulatory Code, 2009, as an auditor, or a person, if not an approved auditor, who is independent of the Incubator fund and whose normal duties include the performance of such an independent audit function; and

- in case of conversion to a Private Fund or Professional Fund, appoint an auditor, a fund manager, and a custodian pursuant to Mutual Funds Regulations (As Revised) of the BVI (the “MFR”) if it does not have these roles already filled (which in most cases it will not have had filled as they are not compulsory for an Incubator Fund). It may apply for exemption from the custodian or fund manager requirement along with the conversion application.

-

Where an Incubator Fund converts into an Approved Fund, the existing sophisticated private investors in the Incubator Fund shall be treated like any other investor in the Approved Fund.

Where an Incubator Fund converts into a professional fund, the existing investors are grandfathered and do not need to comply with the minimum initial investment amount requirement of US$100,000. This requirement would only apply to new incoming investors.

Approved Fund

Similar to the Incubator Fund, upon a triggering event, if the Approved Fund decides to continue its operation as a mutual fund, an application for conversion must be submitted by the Approved Fund to the FSC to convert into and be recognised as a Private Fund or Professional Fund within 7 days of the end of the second month where its total number of investors or the net assets exceed the threshold.

When filing the application, the Approved Fund should:

-

-

- complete the applicable application form and submit the updated fund documentation for the Fund to the FSC to be recognised as a Private Fund or Professional Fund; and

- appoint the auditor, the fund manager, the fund administrator and the custodian, or apply for applicable exemptions as mentioned above.

-

Different to that for an Incubator Fund, an Approved Fund is not, at the time of applying for conversion, subject to a statutory requirement to submit an audit of its current financial position and compliance with the Regulations.

If the Approved Fund converts into a Professional Fund, each investor is required to demonstrate that it is a professional investor and has a minimum investment amount of US$100,000. There is no exemption for existing investors as in the case of an Incubator Fund.

The Incubator Fund or the Approved Fund should notify all of its investors of the conversion and keep them informed about the proposed change of regulatory status. The FSC may also raise queries about the details of the trigger event and the current circumstances of the Fund.

Options other than conversion

When a trigger event occurs, if the Incubator Fund or Approved Fund decides not to proceed with conversion as discussed above, under the Regulations, it should:

-

-

- commence the process for a voluntary liquidation under the BVI Business Companies Act (As Revised); or

- take necessary steps to amend its constitutional documents to cease to be a Fund and remove all references from its constitutional documents to being an Incubator Fund or Approved Fund (as applicable).

-

This publication is not intended to be a substitute for specific legal advice or a legal opinion. For specific advice on the matters covered in this Legal Insight, please contact your usual Loeb Smith attorney or any of the following:

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: vanisha.harjani@loebsmith.com

E: frost.wu@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Subscription credit facilities – also known as “sub-lines” or “capital call facilities” – have gained prominence in recent years as flexible financing options for private equity sponsors and fund managers operating within the Cayman Islands and British Virgin Islands (BVI). This article highlights key features, legal considerations and strategic advantages associated with these structures.

Overview

Subscription credit facilities are secured credit arrangements that enable fund managers to access short-term financing (i.e. short-term loans) against the capital commitments of fund investors.

Unlike traditional fund financing, these facilities are typically structured as revolving credit lines, allowing funds to bridge capital calls, manage liquidity, or seize investment opportunities, therefore allowing quick access to cash for investment without having to call on capital commitments from investors immediately.

Cayman BVI subscription facilities: structuring essentials

- Security and collateral arrangements. The foundation of subscription credit facilities is the security interest over the fund’s unfunded capital commitments. Under Cayman Islands and BVI law, the enforceability of security interests such as a pledge and/or charge over unfunded capital commitments (as collateral for a loan) relies on the proper drafting of security agreements and registration procedures. It is crucial to clearly define the scope of security, including any guarantees or other security interests created to ensure priority and enforceability.

- Intercreditor arrangements. Given that subscription credit facilities often coexist with other fund financing or investor arrangements, establishing clear intercreditor agreements is vital. Intercreditor agreements safeguard funds and investors by defining the payment hierarchy and security rights among multiple lenders. These agreements are essential for ensuring orderly enforcement and mitigating conflicts, particularly in multi-lender scenarios. Offshore jurisdictions facilitate sophisticated intercreditor arrangements, supported by well-established legal frameworks.

- Fund governance and limited partnership agreements. Cayman Exempted Limited Partnerships (ELPs) or BVI Limited Partnerships (LPs) are the typical structure, offering flexibility and strong creditor protections. A fund’s constitutional documents determine the scope of authority its general partner or manager has. In the case of an ELP or LP, this is detailed in the limited partnership agreement (LPA).

Accordingly, to ensure compliance and mitigate legal risks, a fund’s LPA must explicitly authorise the general partner or manager to pledge investor capital commitments as security. It is advisable to include provisions that address the express borrowing authority, mechanics of security, enforcement procedures and investor consent processes (such as through side letters) and any transfer restrictions. - Regulatory and Anti-Money Laundering (AML) considerations. The BVI and Cayman Islands have AML regimes requiring the appointment of AML officers. As subscription facilities often involve large capital commitments from institutional investors, enhanced customer due diligence may be required, in addition to measures such as verifying the source of funds, sanctions screening, record keeping and reporting obligations. Proper due diligence, know your customer procedures and compliance measures are essential to prevent regulatory issues and ensure legality of security interests and transaction structure.

Cayman BVI subscription facilities key advantages

Flexibility and speed. Offshore jurisdictions have efficient legal processes and flexible corporate structures, enabling funds to implement subscription credit facilities swiftly. This agility is critical in investment environments.

Tax neutrality and confidentiality. Both the Cayman Islands and BVI offer tax-neutral regimes and strong confidentiality protection, which are attractive for international fund managers seeking discreet and efficient financing arrangements.

Legal certainty and established frameworks. With mature legal systems, both jurisdictions provide a high degree of legal certainty for security enforcement, contractual validity and dispute resolution, backed by a wealth of case law and legal expertise. The final court of appeal for both is the Privy Council in the UK.

Tips for structuring

- Draft clear security documents. Ensure security interests over capital commitments are precisely defined and properly registered.

- Obtain investor consent. Incorporate provisions in the LPA or side letters to facilitate or confirm investor approval for security grants.

- Plan for enforcement. Establish enforcement procedures like notice periods and rights of first refusal.

- Co-ordinate with creditors. Negotiate intercreditor arrangements early to prevent conflicts.

Conclusion

Subscription credit facilities represent a powerful tool for offshore funds seeking liquidity and operational flexibility, offering a flexible and efficient mechanism aligning well with the governance and operational frameworks of private equity funds in the Cayman Islands or BVI.

The article was first published by Asia Business Law Journal – https://law.asia/cayman-bvi-subscription-credit-facilities/

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Legal Insight, please contact:

Partner: Vanisha Harjani

E: vanisha.harjani@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

This article looks briefly at how an application can be made to the court in the British Virgin Islands (BVI) to restore a BVI company to the Register of Companies (Register), and aims to provide some practical insight into the restoration process.

Application for BVI company restoration

An application to restore a dissolved company to the Register may be made where:

- The company was struck off the Register and dissolved following the completion or termination of its liquidation (whether voluntary or involuntary);

- On the date of dissolution, the company was not carrying on business, or in operation;

- The purpose of restoration is to:

-

- initiate, continue or discontinue legal proceedings in the name of or against the company; or

- make an application for the company’s property that has vested in the Crown bona vacantia to be returned to the company; or

-

- In any other case, or where an application cannot be made to the Registrar of Corporate Affairs (Registrar), the court considers that it is just and fair to restore the company to the Register.

An application has to be made within five years of the date of the company’s dissolution.

Who can apply to restore a dissolved BVI company

The application is made by way of a fixed date claim form together with an affidavit (by the claimant), exhibit and a draft order. The affidavit should set out, inter alia, the purpose of the restoration, and the claimant’s standing to restore the company.

Examples of those who have standing to make an application include:

- A creditor, former director, former member or former liquidator;

- A person who, but for the company’s dissolution, would have been in a contractual relationship with the company;

- A person with a potential legal claim against the company, or its former directors or former members, or in respect of any assets of the company or issued shares; and

- Any other person who can establish an interest in having the company restored to the Register.

Where the purpose of the restoration is to make an application for the company’s property that has been vested in the Crown bona vacantia to be returned to the company, such application shall not be made unless it is accompanied by, in writing:

- Consent of the Crown, signified by the Financial Secretary, that the Crown has no objection to the company’s restoration;

- Response of the Financial Secretary objecting to the company’s restoration; or

- A declaration of the applicant that the Financial Secretary has not responded to a request for consent to the company’s restoration within seven days after receipt of the request.

Notice requirements for restoring BVI company to Register

Notice of the application must be served on the Registrar, the Financial Secretary and, where the company was a regulated person, the Financial Services Commission.

Court powers in the restoration process

Upon an application, the court may exercise its discretion and restore the company. The court may:

- Make an order to restore the company to the Register subject to:

- being satisfied that a licensed person has agreed to act as a registered agent (RA) of the company;

- the proposed RA making a declaration that the company’s records have been updated or an undertaking that the company’s records will be updated or procured and maintained within 14 days from the date of restoration of the company;

- the company filing, or undertaking to file, within 14 days from the date of restoration, copies of its register of members and register of directors; and

- the company paying the restoration fee and any outstanding penalties; and

- Give such directions or make such orders as it considers necessary.

Evidence from the RA should be included in the exhibit to the affidavit.

Steps and requirements for BVI company restoration order

The restoration will usually not take effect immediately when the court orders the restoration of the company to the Register (subject to the wording of the order in question). There are usually several steps that need to be taken before this can happen, including:

- Filing a sealed copy of the order with the Registrar; and

- Paying all outstanding fees and penalties due and payable to the Registrar.

To avoid any delays or complications in the restoration of a company, it is therefore prudent for the claimant to comply with the terms of the order once it has been made by the court.

The article was first published in Asia Business Law Journal. https://law.asia/bvi-company-restoration-court-process-requirements/ dated 11 Feb 2026.

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Insight, please contact us. We would be delighted to assist.

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Our firm has been ranked as Lexology Legal Influencer for Dispute Resolution – Central and South America for Q4 2025. We are proud that Loeb Smith’s articles were ranked as Legal Influencer in all quarters of 2025! Many thanks to our readers and to our contributing author colleagues for making it possible. Find out more about our Litigation and Disputes service.

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Loeb Smith Attorneys: Reflecting on a Remarkable 2025

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

The British Virgin Islands (“BVI”) is a very user-friendly jurisdiction for enforcing foreign judgments and arbitral awards. The Arbitration Act 2013 (as revised) (“Arbitration Act”) governs the enforcement of arbitration awards in the BVI. The Arbitration Act does not distinguish between domestic and foreign awards but does in relation to awards (“Convention Awards”) under the United Nations Convention on the Recognition and Enforcement of Foreign Arbitral Awards 1958 (“New York Convention”) and non-New York Convention awards (“non-Convention Awards”).

Arbitral awards

Convention awards. A convention award is enforceable in the BVI by either:

-

- instituting an action in court; or

- applying to seek leave of the court.

Non-convention awards. Non-convention awards can only be enforced by seeking leave of the court.

Leave to enforce arbitral awards. The requirements and procedures applicable to both a convention award and a non-convention award are the same. An application for the recognition and enforcement of a foreign arbitral award is made via a fixed date claim form, supported by affidavit evidence. The evidence must, among other things:

-

- Exhibit the original or a certified copy of the award (and, if relevant, a certified English translation); and

- Exhibit the original or certified copy of the arbitration agreement (where applicable).

The fixed date claim form must be served on the award debtor. If the award debtor is located outside the jurisdiction, the award creditor must serve out of the jurisdiction.

If leave is granted, the award has the same effect as a BVI court judgment or order and can be enforced using the remedies provided for under the Eastern Caribbean Supreme Court Civil Procedure Rules, which apply in the BVI. The order must be served on the award debtor. The award debtor has the right to apply to set aside the decision.

Refusal to enforce a convention award. The enforcement of a convention award may only be refused if the person against whom enforcement is sought proves one of the convention defences. The defences include:

-

- The arbitration agreement was invalid under the applicable law, or if there was no indication of the applicable law, under the law of the country where the award was made;

- The party was not given proper notice of the appointment of the arbitrator, or of proceedings, or was otherwise unable to present their case; and

- The award has not yet become binding on the parties or has been set aside or suspended by a competent authority of the country in which, or under the law of which, it was made.

The party against whom enforcement action is taken has the burden of proof to demonstrate that one of the applicable circumstances applies.

Refusal to enforce a non-convention award. The grounds for refusal of enforcement of a non-convention award are the same as for a convention award. However, there is the additional ground where the court has a wider discretion to refuse enforcement on its own volition if it considers it just to do so.

Enforcing arbitration awards

Once the arbitration award becomes a BVI judgment, it can be enforced by:

-

- a charging order;

- garnishee order;

- judgment summons;

- an order for the seizure and sale of goods; and

- an order for the appointment of a receiver.

From a practical standpoint, the enforcement of any arbitration award in the BVI is only effective if the judgment debtor has assets in the BVI against which the arbitration award can be enforced. This will usually be in the form of shares in a BVI company. The most common way to enforce is to seek a charging order over the shares in the relevant company owned by the judgment debtor.

Procedurally, this is done by joining the BVI company to the proceedings and applying for a provisional charging order (PCO). The PCO can then be made final. The application does not need to be served on the judgment debtor but the order, once granted, needs to be served. It should be noted that the judgment debtor can oppose the PCO being made final. If it is made final, the judgment creditor can apply for the appointment of a receiver and an order for sale.

Appointment of liquidator

Notwithstanding the above-mentioned, the judgment creditor can instead apply to appoint a liquidator over the judgment debtor (where the latter is a BVI company) to wind up the judgment debtor on the basis that the arbitration award is unpaid. The liquidator can then apply the proceeds of the liquidation to the satisfaction of the judgment debtor’s debts, including the arbitration award. It is normal to serve a statutory demand on the judgment debtor company first in such a situation (although this is not strictly required under the laws of the BVI).

This publication is not intended to be a substitute for specific legal advice or a legal opinion. For specific advice on the matters covered above, please contact your usual Loeb Smith attorney or any of the following:

This published by Asia Business Law Journal” with the link. (https://law.asia/enforcing-arbitration-awards-british-virgin-islands/)

Wonderful news: Loeb Smith Attorneys’ Cayman Islands team has once again been recognised in the rankings of Legal500, one of the top international publications that evaluates law firms and legal professionals worldwide.

In the 2026 edition, Loeb Smith Attorneys reaffirms its strong Cayman Islands positioning standing out in the Investment Funds practice top tier firms and receiving an accolade for Client Satisfaction.

This recognition highlights the trust our clients place in us, the depth of our expertise and the strength of our multidisciplinary teams focused on delivering outstanding client service.

We are very proud of our team and thankful to our clients for taking their time to talk to Legal500. Here is what our clients shared to Legal 500 about us:

‘Their deep knowledge of the nature of digital assets, wallet structures, and Web3 business

models is reflected directly in their drafting. Instead of relying on generic fund templates, they

proactively incorporate crypto-specific wordings and clauses into fund documents, making them

clear, accurate, and practical for all stakeholders, from fund managers to service providers and

even auditors.’

***

‘I’ve worked with Loeb Smith on a number of crypto fund matters, including fund formation,

regulatory compliance, and handling in-kind subscriptions using digital assets.’

***

‘Gary Smith is particularly impressive. He is not only highly knowledgeable on the legal side but

also well-versed in how crypto businesses operate in practice. Their ability to explain complex

regulatory matters in plain language makes decision-making much easier on our end and the

crypto client side.’

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.