This article will provide a general overview of the steps involved in the formation and running of a closed-ended investment fund in the Cayman Islands pursuant to the Private Funds Act (As Revised) (the “Act”).

Type of legal entity used in formation of a private fund

Whilst there are no statutory requirements as to the type of legal entity that should be used in the establishment of a closed-ended fund pursuant to the Act, the type of entity most commonly used for this purpose is the Exempted Limited Partnership (“ELP”). Whilst other types of corporate vehicles can be used, such as a Cayman Islands Exempted Company, these are more commonly deployed in the context of an open-ended investment fund pursuant to the Mutual Funds Act (As Revised).

Who runs a private fund?

If a closed-ended fund (referred to under the Act as a private fund) is structured as an Exempted Company, it will be the directors of that company who operate it. However, as part of the registration of the fund with the Cayman Islands Monetary Authority (“CIMA”), it will be necessary to ensure that there are at least two directors appointed; this is known as the “four eyes principle” to ensure proper corporate governance and investor protection and is a prerequisite for registration as a private fund with CIMA.

If the fund is established as an ELP, the two-director rule does not apply directly to the ELP as ELPs do not have separate legal personality and therefore do not have directors. An ELP must, however, have a qualifying “general partner” who operates the ELP on behalf of the limited partners. It is at the general partner level that the “four eyes principle” will apply in this context and so a general partner must also have at least two directors.

Presently, it is not necessary for the directors of a private fund (or the directors of a general partner of an ELP which is registered as a private fund) to be registered pursuant to the Directors Registration and Licensing Act (As Revised).

Private Funds Act – obligation to register as a private fund

Only closed-ended funds that fall within the definition of a “private fund”, as defined in the Act, will be required to register with CIMA under the Act as a private fund and will be regulated as such. The Act defines a “private fund” as:

“…a company, unit trust or partnership that offers or issues or has issued investment interests, the purpose of effect of which is the pooling of investor funds with the aim of enabling investors to receive profits or gains from such entity’s acquisition, holding, management or disposal of investments, where –

(a) the holders of investment interests do not have day-to-day control over the acquisition, holding, management or disposal of the investments; and

(b) the investments are managed as a whole by or on behalf of the operator of the private fund, directly or indirectly…”

The term “investment interest” is defined in the Act as an interest in the issuing vehicle which carries an entitlement to participate in the profits or gains of the vehicle and which interests are not redeemable or re-purchasable at the option of the investor.

Whether a particular structure will fall within this definition and be subject to regulation can be highly nuanced. We therefore recommend that you speak with an experienced Cayman Islands investment funds attorney to determine whether your proposed project would be regulated or whether an exemption from registration might be available.

For example, the Act itself contains a list of “non-fund arrangements” which are not considered to be “private funds”. The list of non-fund arrangements is extensive and quite broad in remit but we would specifically highlight the following non-fund arrangements:

- Joint ventures;

- Proprietary vehicles;

- Holding vehicles;

- Debt issues and debt issuing vehicles;

- Structured finance vehicles; and

- Sovereign wealth funds.

It should also be noted that single investor funds will also fall outside of the remit of the Act on the basis that where there is only one investor, there will not be any “pooling of investor funds” as required by the above quoted definition of “private fund”.

Registration as a Private Fund under the Act

Where a particular project falls within the definition of a “private fund” and where it is not a “non-fund arrangement”, the corporate vehicle will be required to apply to CIMA for registration as a private fund under the Act.

In order to be registered under the Act, the fund will need to submit a completed application to CIMA via its online portal together with supporting documentation, including its offering document (which should contain, as a minimum, the information specified by CIMA in its Rules on Content of Offering Memorandum) and evidence of the appointment of an auditor and an administrator.

The application must (per section 5 of the Act) be submitted to CIMA (together with payment of the applicable registration fee) within 21 days after its acceptance of capital commitments from investors for the purposes of investments (although the application can be submitted at any time before capital commitments are received). The fund must be registered with CIMA as a private fund before it receives any capital contributions from investors.

Regulatory obligations of private funds

In addition to the above, there are certain other key obligations with which private funds must comply.

Where the fund makes any change (or becomes aware of any change) which materially affects any information that was delivered to CIMA as part of the fund’s registration as a private fund, it must file details of the change with CIMA within 21 days of the change taking effect or of the fund becoming aware of the change. Whilst the Act only requires ‘material’ changes to be notified to CIMA, in practice CIMA tends to be notified of all changes given what is ‘material’ is open to interpretation.

Private funds must also file an annual return with CIMA and pay an annual registration fee in order to maintain its registration.

Ongoing requirements

The Act requires that private funds have in place certain mechanisms and safeguards relating to an annual audit of the fund, the valuation of the fund’s assets, the safeguarding of the fund’s assets, cash monitoring and the identification of securities.

- Audit – the fund must engage an approved Cayman Islands auditor to prepare its audited financial statements annually. CIMA maintains a list of the approved auditor firms who are able to provide this service. Such audited financial statements must be filed with CIMA within six (6) months of the end of each financial year of the fund.

- Valuation of fund assets – the assets of a private fund must be valued periodically. What is considered to be an appropriate period between valuations will depend on the asset class(es) in which the fund is invested. However, valuations should, as a minimum, be carried out at least annually. Each valuation must be carried out by an independent and suitably qualified professional valuer who is familiar with the relevant asset class. If the valuer is not independent, then CIMA reserves the right to have the valuation independently verified at the cost of the fund. Otherwise, if the valuation of assets is carried out by the fund itself or by its investment manager, the valuation function must be independent from the portfolio management function of the fund and any conflicts of interest are required to be identified, managed, monitored and disclosed to investors.

- Safeguarding of the fund’s assets – private funds are, generally speaking, required to appoint a custodian to hold, in segregated accounts maintained in the name of the fund, the fund’s assets which are capable of physical delivery or capable of registration in a separate account except that the private fund shall not be required to appoint a custodian if it has notified CIMA and it is neither practical nor proportionate to do so, having regard to the nature of the private fund and the type of assets it holds. The duty of custodian appointed is to verify the fund’s title to its assets based on information provided by the fund together with any externally available information. If a custodian is not appointed, the verification of the fund’s title to its assets must be carried out either by the fund’s administrator or by the fund itself or its investment manager. In the case of title verification by the fund or its investment manager, the title verification function must be independent from the portfolio management of the fund and any conflicts of interest are required to be identified, managed, monitored and disclosed to investors in the fund.

- Cash monitoring – private funds are required to appoint any of an administrator, custodian or the investment manager to (1) monitor the cash flows of the fund; (2) ensure that all cash has been booked in cash accounts maintained in the name of the fund; and (3) ensure that payments made by investors to the fund for the purposes of investment have been received. If such monitoring is not undertaken by an independent third party, CIMA reserves the right to have the cash monitoring verified at the cost of the fund. In the case of cash monitoring undertaken by the fund or its investment manager, as above, the cash monitoring function must be independent from the portfolio management of the fund and any conflicts of interest are required to be identified, managed, monitored and disclosed to investors in the fund.

- Identification of securities – if the private fund in question regularly trades securities or holds them on a consistent basis, it must keep records of the identification codes (such as ISIN codes or CUSIP codes) of those securities that it trades and holds, and such records must be made available to CIMA on request.

Other obligations

In addition to its obligations under the Act and guidance issued by CIMA, private funds are also subject to other obligations under the laws of the Cayman Islands in relation to matters such as FATCA / CRS compliance and, in respect of anti-money laundering legislation and regulations.

- FATCA / CRS – Private funds tend to be classified as ‘Reporting Financial Institutions” for the purposes of FATCA and CRS. Each private fund is therefore required to undertake detailed due diligence on each of its investors (which is typically undertaken on its behalf by its administrator). The fund must also provide information to the Tax Information Authority of the Cayman Islands in respect of each of its investors who constitute ‘reportable accounts’.

- Anti-money laundering – Private funds conduct “relevant financial business” for the purposes of the Proceeds of Crime Act (As Revised) and the Anti-Money Laundering Regulations (As Revised) (being together the “AML Requirements”). Private funds are therefore required to have robust policies and procedures in place to ensure that the AML Requirements are adhered to. The fund must have a detailed Anti-Money Laundering Compliance Manual which contains detailed guidance on the policies and procedures that must be followed in carrying out the fund’s activities, ranging from the onboarding process for investors, record-keeping, processes for the reporting of suspicious activity and other risk management matters.

- Beneficial ownership – The Beneficial Ownership Transparency Act (“BOTA”) requires Cayman Islands exempted companies, ELPs, and limited liability companies to maintain a beneficial ownership register unless an alternative route to compliance applies. Under the BOTA, alternative routes to compliance are available to categories of legal persons such as private funds and each private fund will be required to provide its corporate services provider in the Cayman Islands with:

- written confirmation of the category into which it falls; and

- the required particulars specific to it.

The private fund is required to appoint a principal point of contact (“PPoC”) who is responsible for responding to any request for beneficial ownership information received from the Cayman Islands Competent Authority (“Competent Authority”) in relation to the private fund. The PPoC must be licensed in the Cayman Islands and will be required to provide the requested beneficial ownership information to the Competent Authority within 24 hours of a request being made, or such other timeframe as may be stipulated in the request.

Each private fund must also appoint three (3) officers to assist with compliance with the AML Requirements; these are the anti-money laundering compliance officer, money laundering reporting officer, and deputy money laundering reporting officer.

Economic Substance

On the basis that private funds are a form of investment fund, private funds that are registered under the Act are not ‘relevant entities’ for the purposes of the International Tax Co-operation (Economic Substance) Act (As Revised). Whilst, therefore, private funds will not be required to demonstrate the extent of their ‘substance’ in the Cayman Islands, they will nonetheless be required to make an annual notification under this legislation to confirm their status as an investment fund.

Conclusion

If you are considering establishing a private fund in the Cayman Islands, it is imperative that you have experienced Cayman Islands legal counsel by your side to assist you in navigating the legislative, regulatory, and compliance landscape. We have a strong reputation for our technical excellence, responsive, forward-thinking and insightful approach to advising clients on offshore Investment Funds and would be happy to be your trusted advisor on the formation, launch and ongoing advisory of your Cayman Islands private fund.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Briefing, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: vanisha.harjani@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

A Captive insurance company is a wholly-owned subsidiary insurer that provides risk mitigation services for its parent company or related entities. In its simplest form, the “Captive” wholly-owned subsidiary is incorporated to insure against one or more risks to which its parent company is exposed. It is essentially a form of self-insurance which is put in place within a group corporate structure for a number of reasons. Captives are usually established in the context of a company’s risk management strategy and are typically put in place because those risks which are looking to be insured by the Captive are either non-insurable or priced too high in the current market.

Captives in the Cayman Islands

The Cayman Islands has historically been a jurisdiction for Captive insurance companies and is currently one of the leading Captive hubs in the world, both in terms of number of Captive insurance companies and total assets under management, owing to Cayman’s world-wide reputation as a highly professional, yet business friendly and well-regulated environment with a philosophy of imposing proportionate, risk-based regulations and rules backed by consistency of enforcement. In particular, the Cayman Islands is the absolute leader domicile for healthcare sector Captives, with healthcare-related Captives taking up over a third of Cayman’s Captive industry. According to data released by the Cayman Islands Monetary Authority (“CIMA”) there were 693 captives) in the Cayman Islands as at the close of 2025 which accounted for 96.25% of all international insurer licensees in the Cayman Islands.

Types of Captives

Single parent Captives (more commonly known as “Pure Captives”), Segregated Portfolio Companies (“SPCs”), and Captives with two or more shareholders (“Group Captives”) make up the largest part of Captives in the Cayman Islands.

SPC’s growing popularity in the Captive insurance industry is partly owed to the fact that such structures allow insurers to add additional participants in a reinsurance programme without risk of cross liability. A distinctive feature of all SPCs, in fact, is that the assets and liabilities of each segregated portfolio (also referred to as ‘cells’) are, as the name suggests, segregated from one another. Each SPC cell, however, does not have legal personality and ownership of the underlying assets in the cells is through classes or series of shares in the SPC which are designated to that particular cell.

The SPC structure is often seen in the context of the so-called ‘Rent-A-Captives‘ whereby those wishing to reap the benefits of a Captive insurance company (either for their own insurance or reinsurance) whilst minimizing matters such as time, upfront costs and maintenance, can simply become shareholders in an existing SPC and ‘rent’ a cell. The participants in a rent-a-Captive structure pay premiums and service fees into the cell and in return they get access to the capital base they need to underwrite the risk as well as an entitlement to any distributions made out of that cell.

There are also Portfolio Insurance Companies (“PICs”) which can be seen as a slight variation of the SPCs mentioned above. A PIC is similar to an SPC except that its cells have separate legal personality.

Other forms of Captives include “Association Captives” which are insurance companies owned by an association to meet the insurance needs of its members, and “Agency Captives” which are insurance or reinsurance companies owned by one or more insurance agents and are used to insure against the risks of those agents or any of their clients.

Benefits of a Captive

The potential benefits of having a Captive insurance company include:

-

- lower insurance costs,

- tax advantages,

- underwriting profits,

- ability to tailor coverage for hard to insure or emerging risks,

- ability to apply alternative strategies to deal with insurance market cycles,

- ability to allocate costs to business units,

- provide financial incentives for loss control,

- offer flexibility in managing risk,

- offer creative insurance solutions, and consolidate risk management, and

- greater control over coverage.

Establishing a Captive: regulatory framework

As with any other industry, the Cayman Islands is a dynamic jurisdiction and strive to offer cutting edge solutions to industry problems owing to the strong relationship and continuous dialogue between the regulator and the private sector. This is no different when it comes to the insurance industry. Captives in the Cayman Islands are principally governed by the Insurance Act, 2010 (the “Act”).

To establish a Captive in the Cayman Islands CIMA will require a formal application for a Class “B” Insurer’s Licence. This application is prescribed in the Act, and requires, among other things, the following information:

-

- Name of applicant. This refers to the name that the Class “B” Insurer company will bear, which should be pre-approved for use by CIMA and the Registrar of Companies.

- A detailed business plan. CIMA will expect to see from the business plan that the proposed Captive operation has been thoroughly researched and properly planned with, among other things, feasibility studies and risk management studies supporting the proposal. It is a requirement of the Act that all Captive insurance companies appoint a local insurance manager and the appointed insurance manager is usually integrally involved in the application process.

- Three (3) years’ financial projections.

- Personal details and references for proposed directors and shareholders. A completed Personal Questionnaire should be provided in respect of ALL proposed Directors, Officers and Managers. A “police clearance certificate” is also required, but CIMA will accept a sworn Affidavit as an acceptable “other certificate”.

- Last two (2) years’ audited statements and/or notarised net worth statement of ultimate beneficial owners.

- Confirmation of appointment from a Licensed Insurance Manager and Approved Auditor.

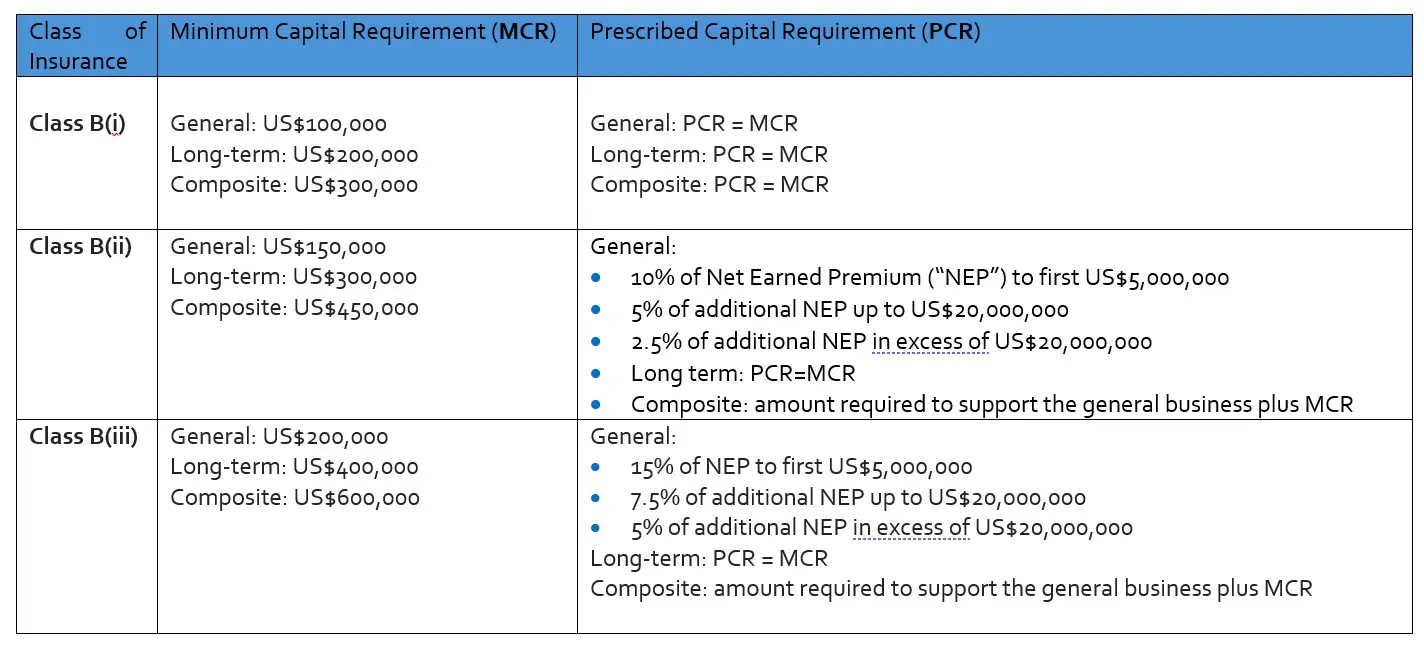

Under the Act, the Class B insurer license is reserved to Captives and is sub-divided into three sub-groups, each relating to a different percentage of the insurer’s related business underwritten by it by reference to net premiums (i.e. Class B(i) 95% or more, Class B(ii) over 50%, and Class B(iii) equal or less than 50%, respectively).

These subdivisions allow CIMA to provide for different thresholds as to (a) Minimum Capital Requirement (“MCR”), (b) Prescribed Capital Requirement (“PCR”) and, consequently, (c) margin of solvency, under The Insurance (Capital and Solvency) (Classes B, C And D Insurers) Regulations, 2012 (the “Regulations”).

a. Minimum Capital Requirement

Under the Regulations, the MCR, which is described as the minimum capital that an insurer must maintain in order to operate in accordance with the Act, for each Class B licensee is as follows:

b. Prescribed Capital Requirement

Under the Regulations, the PCR, which is described as the total risk-based capital that an insurer must maintain in order to operate in a safe and sound manner, is the same as the MCR when it comes to Class B(i) licensees, however, for Class B(ii) and Class B(iii) licensees, it is determined as a percentage by reference to the net-earned premium, which is the net written premium applicable to the expired part of the policy period or reinsurance agreement period.

c. Margin of solvency

Under the Act, margin of solvency is defined as the excess of the value of prescribed assets over prescribed liabilities. In terms of what the margin of solvency should be for each Class B licensee, the Regulations provide that it must be the same as the PCR for all three Class B sub-groups.

CIMA may impose an additional regulatory capital requirement depending upon the business plan submitted. Given the popularity of SPC structures, it is worth noting that the SPC regulatory regime which, owing to its particular stratified structure, differs slightly from the above. Under the Act, in fact, there is no MCR or PCR for cells within an SPC Captive. However, the Regulations provide that the margin of solvency requirement for cells is met so long as each cell passes both cashflow and balance sheet solvency tests.

Once the application with all requisite documentation has been submitted, the Insurance Supervision Division of CIMA will review the application and raise questions if necessary, which can be directed to the appointed insurance manager or Cayman legal counsel. Once CIMA is satisfied that the proposal is sound, a letter can be provided, addressed to the Cayman Registrar of Companies, in order for the company to be incorporated. Simultaneously, a submission for licensing will be made to CIMA’s Management Committee (MC). If approved by the MC, the licence will be issued subject to confirmation that CIMA has received the final copy of the Memorandum and Articles of Association of the company, the Certificate of Incorporation issued by the Registrar of Companies, evidence that the agreed capital has been received by the insurance manager and any other documentation previously identified by CIMA as being required.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to Captive insurance in the Cayman Islands or setting up a Captive, please contact us. We would be delighted to assist.

Subscription credit facilities – also known as “sub-lines” or “capital call facilities” – have gained prominence in recent years as flexible financing options for private equity sponsors and fund managers operating within the Cayman Islands and British Virgin Islands (BVI). This article highlights key features, legal considerations and strategic advantages associated with these structures.

Overview

Subscription credit facilities are secured credit arrangements that enable fund managers to access short-term financing (i.e. short-term loans) against the capital commitments of fund investors.

Unlike traditional fund financing, these facilities are typically structured as revolving credit lines, allowing funds to bridge capital calls, manage liquidity, or seize investment opportunities, therefore allowing quick access to cash for investment without having to call on capital commitments from investors immediately.

Cayman BVI subscription facilities: structuring essentials

- Security and collateral arrangements. The foundation of subscription credit facilities is the security interest over the fund’s unfunded capital commitments. Under Cayman Islands and BVI law, the enforceability of security interests such as a pledge and/or charge over unfunded capital commitments (as collateral for a loan) relies on the proper drafting of security agreements and registration procedures. It is crucial to clearly define the scope of security, including any guarantees or other security interests created to ensure priority and enforceability.

- Intercreditor arrangements. Given that subscription credit facilities often coexist with other fund financing or investor arrangements, establishing clear intercreditor agreements is vital. Intercreditor agreements safeguard funds and investors by defining the payment hierarchy and security rights among multiple lenders. These agreements are essential for ensuring orderly enforcement and mitigating conflicts, particularly in multi-lender scenarios. Offshore jurisdictions facilitate sophisticated intercreditor arrangements, supported by well-established legal frameworks.

- Fund governance and limited partnership agreements. Cayman Exempted Limited Partnerships (ELPs) or BVI Limited Partnerships (LPs) are the typical structure, offering flexibility and strong creditor protections. A fund’s constitutional documents determine the scope of authority its general partner or manager has. In the case of an ELP or LP, this is detailed in the limited partnership agreement (LPA).

Accordingly, to ensure compliance and mitigate legal risks, a fund’s LPA must explicitly authorise the general partner or manager to pledge investor capital commitments as security. It is advisable to include provisions that address the express borrowing authority, mechanics of security, enforcement procedures and investor consent processes (such as through side letters) and any transfer restrictions. - Regulatory and Anti-Money Laundering (AML) considerations. The BVI and Cayman Islands have AML regimes requiring the appointment of AML officers. As subscription facilities often involve large capital commitments from institutional investors, enhanced customer due diligence may be required, in addition to measures such as verifying the source of funds, sanctions screening, record keeping and reporting obligations. Proper due diligence, know your customer procedures and compliance measures are essential to prevent regulatory issues and ensure legality of security interests and transaction structure.

Cayman BVI subscription facilities key advantages

Flexibility and speed. Offshore jurisdictions have efficient legal processes and flexible corporate structures, enabling funds to implement subscription credit facilities swiftly. This agility is critical in investment environments.

Tax neutrality and confidentiality. Both the Cayman Islands and BVI offer tax-neutral regimes and strong confidentiality protection, which are attractive for international fund managers seeking discreet and efficient financing arrangements.

Legal certainty and established frameworks. With mature legal systems, both jurisdictions provide a high degree of legal certainty for security enforcement, contractual validity and dispute resolution, backed by a wealth of case law and legal expertise. The final court of appeal for both is the Privy Council in the UK.

Tips for structuring

- Draft clear security documents. Ensure security interests over capital commitments are precisely defined and properly registered.

- Obtain investor consent. Incorporate provisions in the LPA or side letters to facilitate or confirm investor approval for security grants.

- Plan for enforcement. Establish enforcement procedures like notice periods and rights of first refusal.

- Co-ordinate with creditors. Negotiate intercreditor arrangements early to prevent conflicts.

Conclusion

Subscription credit facilities represent a powerful tool for offshore funds seeking liquidity and operational flexibility, offering a flexible and efficient mechanism aligning well with the governance and operational frameworks of private equity funds in the Cayman Islands or BVI.

The article was first published by Asia Business Law Journal – https://law.asia/cayman-bvi-subscription-credit-facilities/

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Legal Insight, please contact:

Partner: Vanisha Harjani

E: vanisha.harjani@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

The Cayman Islands Government has issued the International Tax Co-operation (Economic Substance) Act (2026 Revision) (the ES Act). This new updated legislation in respect of economic substance consolidates previous amendments made up to 31 December 2025 and replaces the 2024 Revision of the ES Act as the current authoritative version of the legislation.

The new 2026 Revision does not introduce substantive changes to the economic substance regime. Rather, it consolidates prior amendments and updates statutory cross-references, ensuring alignment with related Cayman Islands corporate legislation amended during 2024 and 2025.

No Changes to the Core Substance Test

The scope and operation of the regime remain unchanged. The definitions of “relevant entity” and “relevant activity” continue to apply as set out in the previous ES Act. Relevant entities carrying on relevant activities must continue to satisfy the economic substance test by demonstrating that they are directed and managed in the Cayman Islands, conduct core income generating activities in the Cayman Islands, and maintain adequate operating expenditure, physical presence and personnel in the Cayman Islands, having regard to the level of relevant activity carried on.

The reduced requirements applicable to pure equity holding companies and the enhanced requirements applicable to high-risk intellectual property businesses remain in force.

Reporting and Record-Keeping Obligations

The 2026 Revision confirms the continued application of existing compliance obligations. Relevant entities must submit annual Economic Substance Notifications and, where required, file an Economic Substance Return with the Tax Information Authority within twelve months after the end of the relevant financial year.

Entities are required to retain records and supporting documentation for a period of six years. Maintaining appropriate documentation remains essential to demonstrating compliance with the economic substance test.

Enforcement and Penalties

The enforcement framework under the ES Act remains unchanged. The Tax Information Authority retains statutory powers to review Economic Substance Returns, require the production of information, determine whether an entity has satisfied the economic substance test, and issue notices where it determines that the test has not been met.

Administrative penalties may be imposed for failure to satisfy the economic substance test or for failure to submit a required Economic Substance Return within the prescribed timeframe. The ES Act provides for higher penalties in respect of failures occurring in a subsequent financial year following an earlier determination of non-compliance. Continued failure may also result in additional consequences under the ES Act, including further regulatory action and the exchange of information with overseas competent authorities.

Practical Implications

Although the 2026 Revision does not introduce new substance thresholds or filing deadlines, it reinforces the continued application of the economic substance framework. In-scope entities should ensure that governance arrangements, operational structures and supporting documentation remain consistent with statutory requirements.

This publication is not intended to be a substitute for specific legal advice or a legal opinion. For specific advice on the matters covered above, please contact your usual Loeb Smith attorney or any of the following:

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: vanisha.harjani@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

The Cayman Islands Monetary Authority (“CIMA”) published a Statement of Guidance – Outsourcing Regulated Entities in April 2023 (“Guidance”), which applies to all CIMA regulated entities, including investment funds and managers. The Guidance is principles-based and sets out CIMA’s minimum expectations on the outsourcing of material functions and outsourcing activities by CIMA regulated entities.

Essentially, the Guidance requires regulated entities to maintain the same level of oversight and accountability over outsourced service providers (“OSPs”) as they would over internal functions, to ensure that the outsourcing arrangement does not materially increase the regulated entity’s net risk.

The Guidance dovetails the CIMA Rule on Corporate Governance for Regulated Entities and Statement of Guidance for Mutual Funds and Private Fund also published in April 2023 (Legal Update) – together, they underscore the responsibility of the Directors of a regulated entity to demonstrably exercise prudent monitoring and management oversight over the regulated entity’s business.

What does outsourcing cover?

Outsourcing is the use by a regulated entity of a third party to perform functions or activities on a continuing basis, which would normally be undertaken by the regulated entity – in the context of an investment fund, the key outsourced functions are the Registrar/ NAV Calculation function and independent AML officers. For an investment manager, the AML officer roles and certain operational or back-office administrative support are typically outsourced to third party services.

The Guidance carves out purchasing contracts i.e. a purchase of services, goods and facilities (without the transfer of non-public proprietary information pertaining to clients/ business activities) from the scope of the Guidance.

What does a regulated fund or manager have to do to comply with the Guidance?

1. Prepare an Outsourcing Policy

This must include all items required in accordance with the Guidance. This is not just a one-time tick the box exercise – the Directors of the regulated entity must review and approve the Outsourcing Policy, ensure it is complied with and monitor any changes which are required to be made. Any Board approval, review and amendments to the Outsourcing Policy (including approval of any risk assessment and outsourcing agreement) should be documented to create a clear audit trail of the Board’s monitoring and oversight.

Regulated entities which are part of a wider corporate group may rely on group-level governance structures – however, it is first advisable that they carry out a gap analysis to ensure these frameworks are suitable for local operations and are compliant with the Guidance.

2. Perform a Risk Assessment for each outsourcing service provider

As the regulated entity (including the Directors and Senior Management) remain fully responsible and accountable to CIMA for all outsourced material functions, it is critical that a risk assessment is carried out on all outsourced service providers OSPs before they are engaged to minimize exposure to risk.

A risk assessment should be carried out prior to engagement of the OSP and should consider:

- whether the outsourced services relate to a material function or activity (“Material OSP”). Any material OSP will need to have comprehensive insurance in place;

- the level of due diligence checks carried out on the OSP;

- the impact of the outsourcing arrangement on the finances, reputation and operations of the regulated entity;

- the ability to oversee and maintain appropriate internal controls over the OSP;

- the risk of potential loss of access to important data; and

- the degree of difficulty and time required to find an alternative service provider or to bring the business activity ‘in-house’.

3. Outsourcing agreement

The Guidance is very prescriptive as to the items which need to be covered in the written agreement with a Material OSP. For example, in addition to standard contractual provisions such as scope of work, term and remuneration, the agreement with the Material OSP must include:

- the Material OSP’s conflict of interest management policy;

- the Material OSP’s insurance coverage;

- an obligation of the Material OSP to disclose any material adverse changes, which impact its ability to carry out the outsourced function or activity

- access rights of the registered entity to relevant systems and documents maintained by the Material OSP relating to its outsourced material function or activity;

- access to data and premises of the Material OSP for the purposes of inspection by the regulated entity and/ or CIMA; and

- limitations on use of data of the regulated entity’s proprietary information by the Material OSP.

4. Ongoing monitoring

- Risk assessments and due diligence checks should be completed at least once a year on each Material OSP on an ongoing basis, or on a more frequent basis if determined by the Board (having regard to the risk and materiality of the outsourcing arrangement). Any deficiencies should be addressed promptly.

- A list of Material OSPs engaged should be maintained and approved by the Board of the regulated entity.

- The Board must ensure that there is a contingency plan and exit strategy in place in the event that a Material OSP can no longer perform the outsourced service.

- The regulated entity shall notify CIMA of the appointment of a Material OSP, including details of the location of where the outsourced activity will be carried out and the main reason for outsourcing the activity. The obligation of the regulated entity to notify CIMA also extends to the termination of any outsourcing arrangement with a Material OSP.

CIMA Thematic Review on Outsourcing

In 2025, CIMA conducted a thematic review of the outsourcing arrangements (“Review”) carried out by 16 cross-sector entities (including Investment and Securities) focused on evaluating the effectiveness of governance structures, risk assessment practices and oversight controls relating to outsourcing arrangements. The key findings of the Review were published in January 2026.

In particular, CIMA assessed whether the regulated entities selected implemented the Guidance in proportion to the size, complexity and risk profile of their operations and whether the outsourcing arrangements were structured so as to preserve CIMA’s ability to conduct effective supervision.

While examples of good outsourcing practices were highlighted in the Review, the Review identified the following key deficiencies in the outsourcing arrangements:

- 98% were missing required provisions in the outsourcing agreements;

- 50% did not notify CIMA of the approval or termination of outsourcing arrangements with Material OSPs;

- 45% did not evidence the due diligence assessments were conducted prior to commencing the outsourcing arrangement;

- 36% did not perform risk assessments that took into account all the minimum risks required by the Guidance – in particular, in relation to country, strategic and exit risks;

- 34% of the outsourcing agreement demonstrated deficiencies as to adequacy and effectiveness; and

- 22% conducted insufficient reviews of policies and procedures by the Board of Directors.

Key takeaway from the Review

The Review highlights the necessity for the Directors of a Cayman Islands investment fund and manager to continually monitor the adequacy of any outsourcing arrangement entered into – from both an internal risk management and regulatory perspective.

The key takeaway of the Review is that any outsourcing agreement should be reviewed and approved by the Board at the outset, in line with the Outsourcing Policy (including any entry to the Material OSP log/ notification to CIMA, as required) and re-assessed on an ongoing basis, at least annually. Outsourcing should be a standalone item on the agenda for any board meetings of the regulated entity and any potential delinquencies promptly brought to the table to be remedied.

While the Guidance does not have the same legal status as a CIMA Rule, a finding of non-compliance with the Guidance upon a CIMA inspection is indicative that a regulated entity is not meeting the expectations of the regulator and that the Board of Directors may not be effectively monitoring the business activities of the fund or manager, which is likely to warrant further scrutiny, monitoring and follow up from CIMA.

Legal assistance

For assistance in relation to your regulated entity’s outsourcing arrangements, including drafting/ reviewing outsourcing agreements, carrying out a gap analysis, or preparedness audit in readiness for a CIMA inspection, please reach out to the Loeb Smith contact below:

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Legal Briefing, please contact:

Partner: Elizebth Kenny

E: elizabeth.kenny@loebsmith.com

Liz is a Partner in the Corporate and Funds Group and is also Head of Regulatory and Risk in which capacity she is key thought leader on regulatory licence applications, virtual assets, crypto and fintech regulation, corporate governance reviews, anti-money laundering compliance frameworks, regulatory audits, Corporate Governance, CIMA inspections and remediations, sanction reporting and licencing, data protection laws, regulatory enforcement notices, administrative fines and on mandatory information exchange requirements.

Available corporate structure

What are the main corporate structures used to set up a retail fund? How are they formed?

The statutory and regulatory frameworks that apply to investment funds in the Cayman Islands do not distinguish between retail funds and non-retail funds as the Cayman Islands is not primarily known as a retail fund jurisdiction. Its laws and regulations applicable to investment funds are geared mainly towards attracting institutional investors. Accordingly, the legal structure used for an investment fund is typically based on whether the fund’s strategy will be open-ended or closed-ended. The exempted company (which includes the segregated portfolio company) is the most commonly used legal structure for open-ended funds and the exempted limited partnership is the most commonly used legal structure for closed-ended funds. Both types of legal structures are formed by filing formation documents with the Companies Registry and paying the requisite government fee. There are no special requirements that apply to managers or operators of retail funds (which for present purposes are taken to mean funds that permit an investor to invest an initial minimum amount of less than US$100,000) as distinct from the specific rules, dues and guidances that (i) apply to all Cayman Islands’ domiciled managers and (ii) apply to operators of all Cayman Islands investment funds.

Laws and regulations

What are the key laws and other sets of rules that govern retail funds?

As stated above, the statutory and regulatory frameworks that apply to investment funds in the Cayman Islands do not distinguish between retail funds and non-retail funds. Under section 4(1)(b) of the Mutual Funds Act, a mutual fund can register with the Cayman Islands Monetary Authority (“CIMA”) and permit its investors to each invest an initial minimum amount of less than US$100,000. This type of fund is often referred to as a ‘retail’ fund. However, the regulatory framework that applies to this category of mutual fund (referred to as an administered fund which comprises approximately 1.92% of Cayman Islands’ mutual funds as at 31 December 2025) is pretty much the same as is applicable to other mutual funds registered with CIMA. Closed-ended funds that fall within the scope of the Private Funds Act and are, therefore, registered with, and regulated by, CIMA do not have a minimum initial investment threshold set by law and, therefore, investors will simply have to comply with the investment limits and restrictions set by the manager or operator of the fund.

The Retail Mutual Funds (Japan) Regulations are an exception to the above in that they effectively make a distinction between retail funds and non-retail funds by providing a compliance framework for certain licensed funds under section 4(1)(a) of the Mutual Funds Act that will market to retail investors in Japan, enabling these funds to automatically comply with the applicable securities laws and regulations in Japan. However, these funds are merely a sub-set of licensed funds, which themselves only comprise approximately 0.33% of Cayman Islands’ mutual funds as at 31 December 2025.

Authorisation

Must retail funds be authorised or licensed to be established or marketed in the Cayman Islands?

All mutual funds which fall within the scope of the Mutual Funds Act and all closed-ended funds that fall within the scope of the Private Funds Act are required to be registered with, and be regulated by, CIMA.

Marketing

Who can market retail funds? To whom can they be marketed?

Investment funds (whether structured as an exempted company or a limited liability company (LLC)) are restricted from making an offer of shares of the company or interests of the LLC to the public in the Cayman Islands to subscribe for such securities unless those securities are listed on the Cayman Islands Stock Exchange. There are no similar restrictions in the laws governing limited partnerships or unit trusts. The term “public in the Islands” excludes certain entities and residents, including other Cayman Islands exempted companies, LLCs, exempted limited partnerships, any exempted or ordinary non-resident companies, foreign companies registered in the Cayman Islands and foreign limited partnerships. It also excludes sophisticated persons and high net worth persons (as defined under the Securities Investment Business Act (SIB Act)), which means that making an offer of securities to “private funds” (as defined in the Private Funds Act) in the Cayman Islands is not restricted. Private funds would most likely qualify as sophisticated persons or high net worth persons, or both. An overseas investment fund that wishes to make an offering of its securities to the public in the Cayman Islands will need to either (1) register with CIMA as a mutual fund under the Mutual Funds Act or a private fund under the Private Funds Act or (2) market its securities through a person who is appropriately licensed or authorised by CIMA under the terms of the SIB Act (provided that the securities being offered to the public in the Cayman Islands are listed on a stock exchange approved by CIMA or the investment fund is regulated by a recognised overseas regulatory authority approved by CIMA). However, there is no legal requirement for a local entity to be involved in the fund marketing process.

Managers and operators

Are there any special requirements that apply to managers or operators of retail funds?

The statutory and regulatory frameworks that apply to investment funds in the Cayman Islands do not distinguish between retail funds and non-retail funds. There are no special requirements that apply to managers or operators of retail funds as distinct from the specific rules, dues and guidances that (i) apply to all Cayman Islands’ domiciled managers and (ii) apply to operators of all Cayman Islands investment funds.

Investment and borrowing restrictions

What are the investment and borrowing restrictions on retail funds?

There are no specific legal investment and borrowing restrictions on retail funds under Cayman Islands laws.

Tax treatment

What is the tax treatment of retail funds? Are exemptions available?

The tax treatments and exemptions available to non-retail funds apply equally to retail funds. See section on non-retail funds below.

Asset protection

Must the portfolio of assets of a retail fund be held by a separate local custodian? What regulations are in place to protect the fund’s assets?

Under CIMA’s Rule on the Segregation of Assets – Regulated Mutual Funds, a Cayman Islands mutual fund is required to do the following.

- Appoint a Service Provider (which includes an administrator, custodian, prime broker, or any of their delegates) with regard to ensuring safekeeping of the fund’s Portfolio (i.e. all financial assets and liabilities of an investment fund and any part thereof, including “investor funds” and “investments” as those terms are used in the definition of “mutual fund” in section 2 of the Mutual Funds Act).

- The Portfolio must be segregated and accounted for separately from any assets of any Service Provider.

- The fund must ensure that any Service Provider that holds or manages the Porolio complies with the requirement to ensure that the Portfolio is segregated and accounted for separately from any assets of any Service Provider.

- The overriding requirement of the Rule is that a fund must ensure that none of its Service Providers use the Portfolio to finance their own or any other operations in any way.

Closed-ended funds that fall within the scope of the Private Funds Act are required to appoint a custodian:

-

- to hold in custody, in segregated accounts opened in the name or for the account, of the private fund, the private fund’s assets that are capable of physical delivery or capable of registration (except where the private fund has notified CIMA and it is neither practical nor proportionate given the nature of the private fund and the type of assets held to do so); and

- to verify title to, and maintain records of, fund assets. However, there is no legal requirement for the custodian to be located in the Cayman Islands.

Where a private fund notifies CIMA of its intention not to appoint a custodian, the private fund is required to appoint one of the following persons to carry out the title verification:

-

- an administrator or another independent third party; or

- the manager or operator, or a person with a control relationship with the manager of the private fund, provided that:

- the title verification function is independent from the portfolio management function; or

- potential conflicts of interest are properly identified, managed, monitored and disclosed to the investors of the private fund.

Governance

What are the main governance requirements for a retail fund formed in the Cayman Islands?

CIMA’s Rule on Corporate Governance for Regulated Entities requires a Cayman Islands regulated investment fund to:

- establish, implement, and maintain a corporate governance framework which provides for sound and prudent management oversight of the regulated entity’s business and protects the legitimate interests of relevant stakeholders.

- establish a Governing Body (i.e. the Board of Directors where the entity is a corporation, the General Partner where the entity is a partnership, the manager (or equivalent) where the entity is a Limited Liability Company, and the Board of Trustees where the entity is a trust business) that is responsible for implementing a corporate governance framework that addresses, at a minimum:

-

- Objectives and strategies of the regulated entity;

- Structure of the governance of the Governing Body;

- Appropriate allocation of oversight and management responsibilities;

- Independence and objectivity;

- Collective duties of the Governing Body;

- Duties of individual directors of the Governing Body;

- Appointments and delegation of functions and responsibilities;

- Risk management and internal control systems;

- Conflicts of interest and code of conduct;

- Renumeration policy and practices;

- Reliable and transparent financial reporting;

- Transparency and communications;

- Duties of Senior Management;

- Relations with CIMA

CIMA’s Rule on Corporate Governance for Regulated Entities also sets out CIMA’s expectations with respect to certain baseline standards that a regulated investment fund should have in

place with respect to the matters listed above.

Reporting

What are the periodic reporting requirements for retail funds?

Mutual funds regulated by CIMA must, as long as there is a continuing offering, update their offering documents and prescribed particulars within 21 days of any material change, and are required to file the updated offering document or the prescribed particulars with CIMA within this 21-day period.

A private fund is required under the Private Funds Act to notify CIMA of any change that materially affects any information submitted to CIMA and of any change of its registered office or the location of its principal. The Private Fund will have 21 days aer making the change or becoming aware of the change to file details of the change with CIMA.

All funds regulated by CIMA (mutual funds and private funds) are required to have their accounts audited annually and such audited financial statements must be filed with CIMA within six months of the year end of the fund, along with a financial annual return form including prescribed details, signed by a director. These audited financial statements must be signed off by a CIMA approved Cayman Islands based audit firm.

Issue, transfer and redemption of interests

Can the manager or operator place any restrictions on the issue, transfer and redemption of interests in retail funds?

Restrictions can be contained in the constitutive documents of a fund or otherwise in the terms of issue of the relevant equity interests or investment interests of the fund.

Non-retail pooled funds

Available vehicles

What are the main legal vehicles used to set up a non-retail fund? How are they formed?

Open-ended funds

Exempt companies

Exempt companies are the most common legal vehicle for open-ended funds. The exempted company limited by shares and the exempted segregated portfolio companies (SPCs) make up the overwhelming majority of open-ended funds registered with the Cayman Islands Monetary Authority (CIMA) as at 31 December 2025.

It is possible to incorporate an exempted company limited by shares (including an SPC) on either a standard basis (which takes 4-5 business days after submission of formation documents to the Registrar of Companies) or on an express (same-day) basis subject to paying an additional express fee. Incorporation is effected by filing the company’s memorandum and articles of association and an affidavit sworn by the subscriber to the memorandum of association with the Registrar of Companies. Unless the company proposes to use a restricted word in its

name (eg, “bank” or “insurance”) no prior consent or approval is required from CIMA or any other government agency. The use of the word “fund” in the name is not restricted. The memorandum of association must contain certain basic information about the company, including its registered office address, its authorised share capital and the objects for which it is incorporated. Shares can be denominated in any currency and denomination. There is no minimum or maximum amount prescribed for authorised, issued or paid-up share capital (although at least one share must be in issue at the time of incorporation).

LLCs

A limited liability company (LLC) is a corporate entity that has separate legal personality to its members. Formation of an LLC requires the filing of a registration statement with the Registrar of Companies and payment of the requisite government fee. The LLC must have at least one member and it can be member managed (by some or all of its members) or the LLC agreement can provide for the appointment of persons (who need not be members) to manage and operate the LLC. The liability of an LLC’s members is limited and members can have capital accounts and can agree among themselves (in the LLC agreement) how the profits and losses of the LLC are to be allocated and how and when distributions are to be made (similar to a Cayman Islands exempted limited partnership). An LLC may be formed for any lawful business, purpose or activity and it has full power to carry on its business or affairs unless its LLC agreement provides otherwise. An LLC may (but is not required to) use one of the following suffixes in its name: Limited Liability Company, LLC or L.L.C.

The LLC structure is an attractive option for certain Cayman closed-ended investment funds (eg, they facilitate aligning the rights of investors in onshore and offshore investment funds in a main fund and sub-fund structures) as well as for general partner entities and other carried interest distribution vehicles.

Limited partnerships

Exempted limited partnerships (ELPs) are most commonly used for closed-ended funds and, to the extent that they fall within the scope of the Private Funds Act, are required to be registered with CIMA.

Unit trusts

Unit trusts are based on English trust law but are modified by the Trusts Act of the Cayman Islands for suitability as investment fund vehicles. Under a unit trust arrangement, investors contribute funds to a trustee that holds those funds on trust for the investors, and each investor is directly entitled to share pro rata in the trust’s assets. An advantage of the unit trust is that it may be structured as an ‘umbrella’ unit trust so that different investments may be allocated to different ‘sub-trusts’ with investors subscribing for units in a particular sub-trust. Unlike SPCs, however, there is no statutory segregation of assets and liabilities of each sub-trust.

A unit trust is formed through a declaration of trust by the trustee alone or by a trust deed executed by both the trustee and the investment manager.

Closed-ended funds

The legal vehicles that can be used for closed-ended funds are the same as for open-ended funds. The most popular vehicle used for closed-ended funds is the ELP. Cayman ELPs are governed by a combination of equitable and common law rules (based on English common law) and also statutory provisions, pursuant to the Exempted Limited Partnership Act (as revised). An ELP may be formed for any lawful purpose to be carried out and undertaken either in or from within the Cayman Islands or elsewhere upon the terms, with the rights and powers, and subject to the conditions, limitations, restrictions and liabilities set forth in the Exempted Limited Partnership Act.

An ELP is a legal arrangement and does not have separate corporate personality. The terms of the ELP are set out in a limited partnership agreement and registered in the Cayman Islands by

filing a registration statement with the Registrar of Exempted Limited Partnerships containing the following details:

- the name of the partnership;

- the general nature of the business and term of the partnership;

- the address of the registered office of the partnership

- the name and address of its general partner; and

- a declaration that the partnership shall not undertake business with the public in the Cayman Islands other than so far as may be necessary to conduct business outside the Cayman Islands.

Laws and regulations

What are the key laws and other sets of rules that govern non-retail funds?

Open-ended funds

The Mutual Funds Act (for open-ended funds) and the Private Funds Act (for closed-ended funds) are the two main statutes relevant to the regulation of investment funds in the Cayman

Islands. CIMA is the regulatory body responsible for compliance with these laws and related regulations and has broad powers of enforcement.

The Mutual Funds Act defines a mutual fund as [“a company, unit trust or partnership that issues equity interests, the purpose or effect of which is the pooling of investor funds with the aim of spreading investment risks and enabling investors in the mutual fund to receive profits or gains from the acquisition, holding, management or disposal of investments…”] The reference to “equity interests” means that debt instruments (including warrants, convertibles and sukuk instruments) are excluded and funds issuing such instruments will not be required to register with CIMA as a mutual fund. The scope of regulation extends to Cayman Islands incorporated or established master funds that have one or more CIMA-regulated feeder funds and hold investments and conduct trading activities. Under secon 4(4) of the Mutual Funds Act, limited investor funds (i.e. mutual funds which have 15 investors or less, the majority of whom have the power to appoint or remove the operators of the investment fund (the operator being the directors, the general partner or the trustee, as is relevant given the legal vehicle used for the fund)), are also required to be registered with CIMA with each investor being able to invest less than US$100,000. As at 31 December 2025 there

were 583 limited investors funds registered with CIMA. As at that same date, there were 8,840 registered funds and 3,164 master funds registered with CIMA.

Each CIMA-registered mutual fund is required to have its accounts audited annually by a firm of auditors on the CIMA approved list of auditors and file such audited accounts with CIMA

within six months of the end of each financial year of the mutual fund (along with a financial annual return in CIMA’s prescribed form).

Mutual funds that are established for a sole investor and do not involve the pooling of investor funds fall outside the regulatory framework of the Mutual Funds Act. Nonetheless, a

mutual fund with a single investor can apply for voluntary registration to, among other things, benefit from the status of being a regulated fund.

Cayman Islands laws and regulations do not impose restrictions on, or prescribe rules for investment strategies of open-ended funds, or their use of leverage, shorting or other techniques.

Closed-ended funds

The Private Funds Act requires the registration of closed-ended funds (typically, investment funds that do not grant investors with a right or entitlement to withdraw or redeem their shares or interests from the fund upon notice) with CIMA. The Private Funds Act applies to private equity funds, venture capital funds, real estate funds, and other types of closed-ended funds set up as Cayman Islands limited partnerships, companies (including SPCs), unit trusts and limited liability companies.

The Private Funds Act also applies to non-Cayman Islands private funds carrying on business or attempting to carry on business in or from the Cayman Islands. In addition to registration with CIMA, the Private Funds Act also imposes the following regulatory requirements to be met by private funds.

- Audit – Each private fund is required to have its accounts audited annually by a firm of auditors on the CIMA-approved list of auditors and file such audited accounts with CIMA within six months of the end of each financial year of the private fund (along with a financial annual return in CIMA’s prescribed form).

- Valuation of assets – A private fund must have appropriate and consistent procedures for the purposes of proper valuations of its assets, which ensures that valuations are conducted in accordance with the requirements in the Private Funds Act. Valuations of the assets of a private fund are required to be carried out at a frequency that is appropriate to the assets held by the private fund and, in any case, on at least an annual basis.

- Safekeeping of fund assets – The Private Funds Act requires a custodian: (1) to hold the private fund’s assets that are capable of physical delivery or capable of registration in a custodial account except where that is neither practical nor proportionate given the nature of the private fund and the type of assets held; and (2) to verify title to, and maintain records of, fund assets.

- Cash monitoring – The Private Funds Act requires a private fund to appoint an administrator, custodian or another independent third party (or the manager or operator of the private fund):

- to monitor the cash flows of the private fund;

- to ensure that all cash has been booked in cash accounts opened in the name, or for the account, of the private fund; and

- to ensure that all payments made by investors in respect of investment interests have been received.

- Identification of securities

A private fund that regularly trades securities or holds them on a consistent basis must maintain a record of the identification codes of the securities that it trades and holds and make this available to CIMA upon request.

Directors of mutual funds structured as exempted companies, managers of investment funds structured as LLCs and directors of general partners of investment funds structured as an exempted limited partnership (in each case, wherever in the world these persons are located, not just to Cayman Islands-based directors) regulated by CIMA are required to register with CIMA under the Directors Registration and Licensing Act (DRLA). The DRLA enables CIMA to verify certain information in respect of directors or managers of CIMA-registered funds. There is currently no requirement for registration of directors with CIMA under the DRLA who are directors of closed-ended funds that fall within the scope of the Private Funds Act. However, this may change in the future.

All investment funds are required to comply with Cayman Islands anti-money laundering legislation and regulations, including appointing an anti-money laundering compliance officer, a money laundering reporting officer, and a deputy money laundering reporting officer. The Cayman Islands government and CIMA actively work with the European Union, the Organisation for Economic Co-operation and Development, the Financial Action Task Force and regulators in numerous jurisdictions to observe and maintain international standards on transparency and good corporate governance.

Authorisation

Must non-retail funds be authorised or licensed to be established or marketed in the Cayman Islands?

The statutory and regulatory frameworks that apply to investment funds in the Cayman Islands do not distinguish between retail funds and non-retail funds. All mutual funds (except for those that are single investor funds) are required to be registered with CIMA and fall within its regulatory framework. Closed-ended funds that fall within the scope of the Private Funds Act are required to be registered with, and regulated by, CIMA.

Marketing

Who can market non-retail funds? To whom can they be marketed?

Investment funds (whether structured as an exempted company or a LLC) are restricted from making an offer of shares of the company or interests of the LLC to the public in the Cayman Islands to subscribe for such securities unless those securities are listed on the Cayman Islands Stock Exchange. There are no similar restrictions in the laws governing limited partnerships or unit trusts. The term “public in the Islands” excludes certain entities and residents, including other Cayman Islands exempted companies, LLCs, exempted limited partnerships, any exempted or ordinary non-resident companies, foreign companies registered in the Cayman Islands and foreign limited partnerships. It also excludes sophisticated persons and high net worth persons (as defined under the Securities Investment Business Act (the “SIB Act”)), which means that making an offer of securities to “private funds” (as defined in the Private Funds Act) in the Cayman Islands is not restricted. Private funds would most likely qualify as sophisticated persons or high net worth persons, or both. An overseas investment fund that wishes to make an offering of its securities to the public in the Cayman Islands will need to either (1) register with CIMA as a mutual fund under the Mutual Funds Act or a private fund under the Private Funds Act, or (2) market its securities through a person who is appropriately licensed or authorised by CIMA under the terms of the SIB Act (provided that the securities being offered to the public in the Cayman Islands are listed on a stock exchange approved by CIMA or the investment fund is regulated by a recognised overseas regulatory authority approved by CIMA). However, there is no legal requirement for a local entity to be involved in the fund marketing process.

Ownership restrictions

Do investor-protection rules restrict ownership in non-retail funds to certain classes of investor?

The legal requirement to be an eligible investor in a registered mutual fund with more than 15 investors is a minimum initial investment of US$100,000 (or its equivalent in any other currency); otherwise no other investor – qualification criteria apply to such funds. This minimum initial investment requirement does not apply to registered mutual funds with 15 or fewer investors and also does not apply to closed-ended funds falling within the scope of the Private Funds Act.

Managers and operators

Are there any special requirements that apply to managers or operators of non-retail funds?

There is no requirement for the manager of a Cayman Islands fund to be resident or domiciled in the Cayman Islands.

There are no Cayman Islands laws that seek to regulate overseas managers of Cayman Islands investment funds. Fund managers established in the Cayman Islands need to comply with the provisions of the Securities Investment Business Act and such fund managers must either be licensed or registered with the CIMA. There are also economic substance requirements and AML requirements which must be complied with.

Directors of mutual funds structured as exempted companies, managers of investment funds structured as LLCs and directors of general partners of investment funds structured as exempted limited partnerships (in each case, wherever in the world these persons are located, not just Cayman Islands-based directors) regulated by CIMA are required to register with CIMA under the DRLA. The DRLA enables CIMA to verify certain information in respect of directors or managers of CIMA-registered funds. There is currently no requirement for registration of directors with CIMA under the DRLA who are directors of closed-ended funds that fall within the scope of the Private Funds Act. However, this may change in the future.

Tax treatment

What is the tax treatment of non-retail funds? Are any exemptions available?

Cayman Islands tax treatment is the same for both “retail” funds and non-retail funds. The Cayman Islands has no direct taxaon of any kind. There are no income, corporaon, capital gains or withholding taxes or death duties. It is possible for all types of Cayman Islands legal structures (exempted company, LLC, unit trust and ELP) to apply to the Cayman Islands government or a tax undertaking that the legal structure will not be subject to direct taxation, for a minimum period, which in the case of a company is 20 years, and in the case of an LLC, unit trust and an ELP is 50 years.

Asset protection

Must the portfolio of assets of a non-retail fund be held by a separate local custodian? What regulations are in place to protect the fund’s assets?

Under CIMA’s Rule on the Segregation of Assets – Regulated Mutual Funds, a Cayman Islands mutual fund is required to do the following.

- Appoint a Service Provider (which includes an administrator, custodian, prime broker, or any of their delegates) with regard to ensuring safekeeping of the fund’s portfolio (i.e. all financial assets and liabilities of an investment fund and any part thereof, including “investor funds” and “investments” as those terms are used in the

definition of “mutual fund” in section 2 of the Mutual Funds Act). - The Portfolio must be segregated and accounted for separately from any assets of any Service Provider.

- The fund must ensure that any Service Provider that holds or manages the Portfolio complies with the requirement to ensure that the Portfolio is segregated and accounted for separately from any assets of any Service Provider.

- The overriding requirement of the Rule is that a fund must ensure that none of its Service Providers use the Portfolio to finance their own or any other operations in any way.

Closed-ended funds that fall within the scope of the Private Funds Act are required to appoint a custodian (1) to hold the private fund’s assets that are capable of physical delivery or capable of registration in a custodial account except where that is neither practical nor proportionate given the nature of the private fund and the type of assets held; and (2) to verify title to, and maintain records of, fund assets. However, there is no legal requirement for the custodian to be located in the Cayman Islands.

Governance

What are the main governance requirements for a non-retail fund formed in the Cayman Islands?

The Mutual Funds Act (for open-ended funds) and the Private Funds Act (for closed-ended funds) are the two main statutes relevant to the regulation of investment funds in the Cayman Islands. CIMA is the regulatory body responsible for compliance with these laws and related regulations and has broad powers of enforcement. Depending on the legal structure of the investment fund, there are also various continuing filing obligations and annual registration fees to be paid.

Reporting

What are the periodic reporting requirements for non-retail funds?

CIMA’s Rule on Corporate Governance for Regulated Entities requires a Cayman Islands regulated investment fund to:

- establish, implement, and maintain a corporate governance framework which provides for sound and prudent management oversight of the regulated entity’s business and protects the legitimate interests of relevant stakeholders.

- establish a Governing Body (i.e. the Board of Directors where the entity is a corporation, the General Partner where the entity is a partnership, the manager (or equivalent) where the entity is a Limited Liability Company, and the Board of Trustees where the entity is a trust business) that is responsible for implementing a corporate governance framework that addresses, at a minimum:

-

- Objectives and strategies of the regulated entity;

- Structure of the governance of the Governing Body;

- Appropriate allocation of oversight and management responsibilities;

- Independence and objectivity;

- Collective duties of the Governing Body;

- Duties of individual directors of the Governing Body;

- Appointments and delegation of functions and responsibilities;

- Risk management and internal control systems;

- Conflicts of interest and code of conduct;

- Remuneration policy and practices;

- Reliable and transparent financial reporting;

- Transparency and communications;

- Duties of Senior Management;

- Relations with CIMA.

CIMA’s Rule on Corporate Governance for Regulated Enes also sets out CIMA’s expectations with respect to certain baseline standards that a regulated investment fund should have in place with respect to the matters listed above.

This publication is not intended to be a substitute for specific legal advice or legal opinion. For more information or specific legal advice, please contact:-

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: vanisha.harjani@loebsmith.com

E: faye.huang@loebsmith.com

E: vivian.huang@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

CIMA advises that the application of penalties for the settlement of any outstanding balances relating to the revised annual fees for regulated mutual funds and private funds has been extended from 15 February 2026 to 15 March 2026.

This extension is intended to provide industry stakeholders with additional time to complete internal reconciliations, administrative processes, and payment arrangements under the revised fee framework.

All outstanding amounts should be remitted in full on or before 15 March 2026. Any entity that fails to remit all applicable fees in full after the revised date will be regarded as non-compliant and will be subject to the assessment of penalties in accordance with the relevant legislation.

For entities seeking clarification, please email: Contactlnvestments@cima.ky.

This was published by Cayman Islands Monetary Authority with the link: https://www.cima.ky/extension-of-application-of-penalties-revised-fees-for-funds or read full notice on: https://lnkd.in/ezasREgb

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Legal Briefing, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: vanisha.harjani@loebsmith.com

E: faye.huang@loebsmith.com

E: vivian.huang@loebsmith.com