Introduction

The Cayman Islands (Cayman) has been the leading offshore jurisdiction for merger and acquisition (M&A) activity over the last two (2) years. In 2015, Cayman-incorporated companies were the target of 863 transactions worth a combined value of USD116.41bn. The value was more than twice the amount of the British Virgin Islands with USD49.62bn (with 387 M&A transactions) and well in excess of Bermuda with 498 M&A transactions with a combined value of USD67.57bn.

In 2016, Cayman-incorporated companies again led the way in terms of offshore M&A activity and were the target of transactions worth a combined USD68.85bn followed by the British Virgin Islands with USD41.65bn and Bermuda with USD41.25bn. By way of comparison, Hong Kong incorporated companies were the target of transactions worth a combined USD33.19bn in 2016.

With Cayman-incorporated companies becoming the target for such a large proportion of offshore M&A activity, our Year in Review of the Cayman Merger Take-Privates that completed successfully in 2016 aims to showcase some recent trends resulting from M&A activity in the specific area of merger take-privates involving Cayman-incorporated companies listed on U.S. stock exchanges, and to discuss some related lessons which are useful for shareholders, directors and their onshore legal advisors. While our main focus is on those transactions which actually completed in 2016, in providing our analysis on recent trends we also cover some M&A transactions that were either aborted or are still ongoing.

Development of the trend for using Cayman companies for IPOs and merger take-privates

Starting with the 1990’s, many Chinese companies chose to list on the New York Stock Exchange (NYSE) or the Nasdaq Stock Market (NASDAQ) to gain, among other things, access to capital from U.S. investors and stature and credibility in an increasing global world. In or around 2011 and 2012, this trend changed. While U.S. listings remained attractive for Chinese companies, the cost of complying with reporting standards continued to increase. Additionally, a lack of comprehension by U.S. investors of the corporate structures being utilised by these companies and of the underlying business environment in China led to lower market valuations for these Chinese companies.

This opened the door for arbitrage opportunities. A Chinese company which was listed on the NYSE or NASDAQ but which had a stock market value lower than its intrinsic value would be taken private and de-listed with help from private equity (PE) sponsors and either (i) continue to be privately held and later sold to a strategic or a financial buyer or (ii) re-listed on the Shanghai Stock Exchange, the Hong Kong Stock Exchange or the Singapore Stock Exchange for a better

Since 2010, the Cayman Islands statutory merger regime (the “Cayman Merger Law”) has offered a more streamlined and efficient offshore alternative to the onshore merger law regimes (e.g. in New York and Delaware). The popularity of the Cayman Islands for merger take-privates further increased when in 2011 the shareholder voting threshold for approving a merger was reduced to a special shareholder resolution requiring only two-thirds of the votes cast.

Our Year in Review of the Cayman Merger Take-Privates that completed successfully in 2016 which (i) provides legal insights into developing trends and lessons that can be learned from merger take-private acquisitions from U.S. stock exchanges using the Cayman Merger Law, and (ii) deals with the issues that acquirers and minority shareholders should bear in mind. In addition to the above, the publication covers the following areas:

The Nuts and Bolts of the Cayman Merger Law Regime

Data Analysis of Merger Take-Private Transactions which completed successfully, including the following topics:

Financing

Cash, Equity or Debt

Length of the Merger Process

Negotiating with the Special Committee

What Value?

Valuation Methods

Top 5 Lessons for the Buyout Group from the 2016 Take-Privates

Top 5 Lessons for the Minority Shareholders from the 2016 Take-Privates

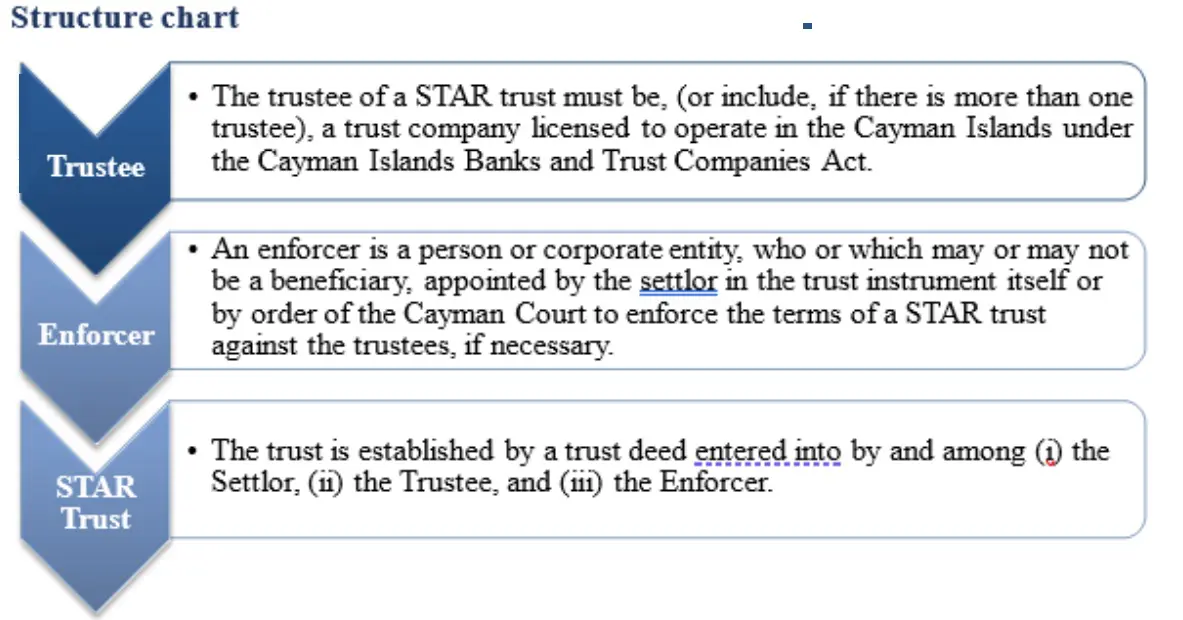

The Special Trusts (Alternative Regime) Law, 1997, now incorporated into Part VIII of the Trusts Law (2011 Revision) (the “Law”) provides the legal basis on which private purpose trusts can be established in the Cayman Islands, without affecting the previously existing laws governing the creation and administration of traditional trusts.

Since their introduction in 1997, STAR trusts (as they are commonly referred to) have gained a strong reputation for being flexible estate planning tools where special purpose vehicles are too inflexible or otherwise inappropriate. Unlike traditional English common law trust principles, under which a trust is not valid unless it is for the benefit of an identified person or class of persons or for charitable purposes, the STAR trusts can be (i) for the benefit of an identified person or any number of persons or (ii) solely for the benefit of charitable or non-charitable purposes or objectives provided that the purposes are lawful and not contrary to public policy.

What was the rationale for creating STAR Trusts

Before the Law was enacted, it was not possible to create trusts for a purpose other than a charitable purpose. The Law also permits perpetual trusts; that is, trusts without a perpetuity or expiry period. Cayman Islands trusts which are not subject to the STAR trusts regime are currently limited to a maximum duration of 150 years.

STAR trusts can be (i) for the benefit of an identified person or any number of persons or (ii) solely for the benefit of charitable or non-charitable purposes or objectives provided that the purposes are lawful and not contrary to public policy. This is a unique feature of STAR trusts and highlights the flexibility offered by the STAR trust structure. It is a requirement of the STAR trust regime that at least one trustee of a STAR trust is a trust company licensed in the Cayman Islands or a private trust company registered as such in the Cayman Islands.

What are STAR Trusts used for?

STAR trusts are commonly used for, among other things, the following.

- To create dynasty-style trusts for multiple generations primarily for holding treasured family assets, investments, and preserving shares in family businesses.

- To create trusts for philanthropic purposes which are outside of the scope of what would be considered charitable as a matter of Cayman Islands law.

- To create trusts which restrict the rights of troublesome beneficiaries who may be tempted to challenge the trust, to seek to obtain information in relation to the trust, among other things.

- To create trusts which are unrestricted by a perpetuity period.

- To create trusts which benefit persons while at the same time achieving alternative objectives such as the continuation of family businesses.

- To form “Special Purpose Vehicles” for a wide range of commercial transactions in a safe, flexible, and bankruptcy remote manner.

- To act as a vehicle to hold shares in a private company, thus allowing a family member (or members) to retain a degree of control over the administration of the underlying trusts and influence decisions which may affect the underlying trusts and the assets they hold (most typically, shares in a family business).

- For clubs and associations whereby their members can enforce terms of contracts without actually being a party to the contract. Also, upon the dissolution of the club or association, the contributed assets may be returned to members in portions specified in the trust deed, rather than in an ad-hoc manner.

Regulation and registration

The Trustee of a STAR trust must be or must include a trust company licensed to conduct trust business in the Cayman Islands. This adds a level of oversight and regulation above and beyond other jurisdictions.

The Trustee of a STAR trust is also required to keep, in its Cayman Islands office, a documentary record of:

(i) the terms of the STAR trust,

(ii) the identity of the Trustee and the enforcer(s),

(iii) all settlements of the property upon trust and the identity of the settlor(s),

(iv) the property subject to the STAR trust at the end of each of its accounting years, and

(v) all distributions or applications of the trust property.

These additional obligations clarify any uncertainty in the common law regarding the retention of trust records and other vital information. These requirements therefore

standardize and clarify important administrative expectations specifically imposed on STAR trust Trustees.

Registration

There is no requirement to register a STAR trust with the regulatory authorities in the Cayman Islands, hence confidentiality is preserved. In fact, all trust deeds (except “exempted trusts”) are exempt from registration. Therefore, the details of a STAR trust will remain confidential, subject only to disclosure as may be required by an order of the Cayman Islands Courts.

Conclusion

With sound professional advice, the STAR trust provides a flexible and valuable tool for structured financing arrangements, as well as for the estate and financial planning of private parties seeking a safe and reliable trust mechanism to satisfy their specific needs and purposes.

This publication is not intended to be a substitute for specific legal advice or a legal opinion. It deals in broad terms only and is intended to merely provide a brief overview and general guidance only. For more specific advice on STAR Trusts in the Cayman Islands, please refer to your usual contact or:

Gary Smith

Partner

T +1 (345) 749 7590

M +1 (345) 525 0900

E gary.smith@loebsmith.com

www.loebsmith.com

In the first two issues of our series of legal insights on owning intellectual property (IP) through a Cayman Islands structure, we discussed how the Cayman Islands aim to become an important offshore hub for the development and commercial exploitation of IP, some of the key benefits of being in the Special Economic Zone (SEZ) and certain advantages of incorporating an exempted company in the Cayman Islands (Incorporate Your Idea. How to Develop Your Intellectual Property in the Cayman Islands) and also how the Cayman Islands legal framework has been modernized to cover IP rights in the digital age and how trade secrets are protected in equity, with a special focus on FinTech companies (Financial Technology Intellectual Property (FinTech IP) Welcome in the Cayman Islands). In this third issue, we take a closer look at the “brand new” Cayman Islands Trade Marks Law, published on 19th December 2016 and which is expected to come into force early 2017, pursuant to which a stand-alone comprehensive trademark protection regime is created in the Cayman Islands (the “New Trade Marks Regime”) to replace the current system of extension of UK/EU IP rights.

Basic Concepts of the New Trade Marks Regime:

- A Classic Trade Mark Definition. The concept of “trademark” is defined, in line with the harmonized definition, which is currently applied throughout the European Union countries1, as any sign capable of being represented graphically which is capable of distinguishing goods or services of one undertaking from those of other undertakings. It may consist of words (including personal names) designs, numerals, letters or the shape of goods or their packaging2. However, upon a closer look, the Cayman Islands have not followed the most recent dematerialization trends in Europe, where, starting from September 2017, signs will be registered as trademarks if they are represented in any appropriate form (i.e., not only a graphic form) using generally available technology3.

- Cayman Register. A Register of Trade Marks will be maintained by a Registrar of Trade Marks (the “Registrar”) and will include details of applications for registration (including graphic representations of trade marks), filing dates and dates of priority, names of proprietors of registered trademarks, and any transactions or events affecting registered trademarks (such as an assignment, the grant of a licence, or the grant of any security interest, whether fixed or floating), which are filed with the Registrar in order to protect the rights in the registered trade mark against third parties4.

- Traditional Annual Registration Fees. One of the main features of the current system for trademark protection in the Cayman Islands, the annual registration fee, will remain in place under the New Trade Marks Regime. The proprietor of a registered trademark must, through its registered agent, pay a prescribed annual fee by January 1 of each year. If the annual fee remains unpaid at March 31, the rights shall be deemed to be in abeyance from April 1 until the annual fee and the prescribed penalty have been paid.

Transitioning to the New Trade Marks Regime and Practical Issues:-

While Regulations detailing the New Trade Marks Regime have not yet been published, the following questions and answers may give companies owning trademarks which are registered or which are planning to be registered shortly in the Cayman Islands, and their IP agents, some useful insight with respect to a few practical issues:

1. What information should be provided with an application for trademark registration and what will be the registration process under the New Trade Marks Regime?

An application to register a trademark in the Cayman Islands will include6, under the New Trade Marks Regime:

(a) a request for registration of a trademark;

(b) the name and address of the applicant;

(c) the name and address of the registered agent;

(d) a statement of the goods or services in relation to which it is sought to register the trademark;

(e) the classification of the goods or services; and

(f) a representation of the trademark.

After the application is complete, the Registrar will review the documentation provided, carry out a search of earlier trademarks in the Register of Trade Marks, and examine if requirements for registration are met7.

⇒ If requirements for registration are not met, the Registrar will inform and give the applicant an opportunity for representations or amendments.

⇒ If requirements for registration are met, applications will be published for opposition by third parties, with the opposition period being 60 (sixty) days following publication8.

The registration process is expected to last an average of three (3) months, and the registration of a trademark must be completed within six (6) months from the date of application, or the Registrar may treat the application as abandoned.

2. When is the trade mark protected?

Under the New Trade Marks Regime, the proprietor has exclusive rights in the registered trademark, preventing any use of the trademark in the Cayman Islands without the proprietor’s consent, starting with the date of filing of the application for registration10, which is the day on which the complete application is filed with the Registrar. (If the initial application is incomplete, the date of filing is the final day on which a relevant document was submitted11.)

Registration of a trademark will not be, however, enforceable against an unregistered earlier trademark which has been in constant use in the Cayman Islands12.

3. When will the registration of a trade mark be refused in the Cayman Islands?

As is customary for any trademark registration systems, the Registrar will refuse the registration of a trade mark13 which is devoid of any distinctive character, or which designates the kind, quality, quantity, purpose, value, geographical origin, time of production, or other characteristics of goods or services, or which is customary in the current language or the established practices of the trade. A trademark will also not be registered if it may deceive the public as to the nature, quality, geographical origin of the goods or services or any other characteristic of the goods or services.

Identical or similar trademarks will not be registered for similar goods or services because of the risk of confusion on the part of the public. Similar trademarks may be registered, however, subject to the consent of the proprietor of the earlier trade mark14 or upon the applicant showing honest concurrent use of the trademark for which registration is sought 15.

In addition to the grounds for refusal referred to above, the New Trade Marks Regime protects existing Cayman Islands’ businesses by restricting registration of trademarks which may take unfair advantage of, or be detrimental to, the distinctive character or the repute of an earlier similar trademark already registered or otherwise protected in the Cayman Islands and which has a reputation in the Cayman Islands16.

Also, the Registrar is prohibited by law17 from registering a trademark which consists exclusively of the word “Cayman”, “Cayman Islands”, “Grand Cayman”, “Cayman Brac”, “Brac” or “Little Cayman”. A trademark will also not be registered if it is contrary to public policy or to accepted principles of morality in the Cayman Islands. Furthermore, the Registrar may publish from time18 to time by notice in the Cayman Islands Gazette, a list of words, letters or devices which are restricted or prohibited to be used in connection with a trademark registration.

4. If the applicant receives a letter of objections, can a trade mark still be registered?

Depending on the objections of the Registrar, to avoid grounds for refusal or to resolve conflicts with existing trademarks, an applicant for registration of a trademark, or the proprietor of a registered trademark, may disclaim any right to the exclusive use of any specified element of the trademark or agree that the rights conferred by the registration shall be subject to a specified territorial or other limitation. This may also be required by the Registrar or the Cayman Court as a condition of the trademark being registered on the Register of Trade Marks19.

- Article 2 of the Directive 2008/95/EC of the European Parliament and of the Council

- Article 2(1) of the Trade Marks Law, 2016.

- The Amending Regulation (EU) No 2015/2424 removes the graphical representation requirement.

- Unless such transactions are registered in the Register of Trade Marks, assignees are not entitled to damages or an account of profits in respect of any infringement of the registered trade mark occurring after the date of the transaction. See Article 39 of the Trade Marks Law, 2016.

- Article 21 of the Trade Marks Law, 2016

- Article 13(2) of the Trade Marks Law, 2016

- Article 15 of the Trade Marks Law, 2016

- Article 16(2) of the Trade Marks Law, 2016

- Article 15(6) of the Trade Marks Law, 2016

- However, under Article 29(3) of the Trade Marks Law, 2016, no infringement proceedings may be begun before the date on which the trade mark is in fact registered.

- Article 14(2) of the Trade Marks Law, 2016

- Article 31(3) of the Trade Marks Law, 2016

- Article 23(1) of the Trade Marks Law, 2016

- Article 25(6) of the Trade Marks Law, 2016

- Article 26 of the Trade Marks Law, 2016; “honest concurrent use” means such use in the Islands by the applicant or use with the applicant’s consent, at the same time that use is made by the proprietor of the earlier trade mark.

- Article 25(3) of the Trade Marks Law, 2016

- Article 23(2) of the Trade Marks Law, 2016

- Article 23(5)(c) of the Trade Marks Law, 2016

- Article 33(4) of the Trade Marks Law, 2016

This is not intended to be a substitute for specific legal advice or a legal opinion.

Ramona Tudorancea

Corporate / M&A Specialist

Suite 329 | 10 Market Street | Camana Bay |

Grand Cayman KY1-9006 | Cayman Islands

E ramona.tudorancea@loebsmith.com

www.loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Introduction

What changes have been introduced recently in Cayman Islands law that you believe will enhance the jurisdiction’s offering in the investment funds industry?

In June 2016 the Cayman Islands brought into effect The Limited Liability Companies Law, 2016 (the “LLC Law”) which introduces a new Cayman Islands limited liability company (an “LLC”). Since July 2016 there has been an increasing number of LLCs formed and also a large number that have transferred to the Cayman Islands by way of continuation from other jurisdictions. The Cayman Islands LLC structure will be attractive for general partner entities and other carried interest distribution vehicles because while the LLC has the benefit of being (like a Cayman Islands exempted company) a separate corporate entity with limited liability, it does not have the maintenance of capital restrictions applicable to exempted companies and therefore has more flexibility to make distributions of income and capital through the terms of the LLC Agreement. For the same reason, LLCs are also proving attractive for management company entities. We expect that over the next few years LLCs might also prove attractive as a structure for offshore funds in order to align the rights of investors between onshore and offshore investment funds in master/feeder structures.

What are the key features of a Cayman LLC?

The key features are:

An LLC formed under the LLC Law is similar in structure to the Delaware LLC as the LLC Law is broadly based on the Limited Liability Company Act in the State of Delaware. However the LLC Law has also preserved the broad legal principles applicable to Cayman Islands companies and the rules of equity and common law.

An LLC is a corporate entity which has separate legal personality to its members.

Formation of an LLC is straightforward. It requires the filing of a registration statement with the Companies Registry and payment of the requisite Government fee.

An LLC must have at least one member. It can be member managed (by some or all of its members) or the LLC agreement can provide for the appointment of persons (who need not be members) to manage and operate the LLC.

The liability of an LLC’s members is limited. Members can have capital accounts and can agree amongst themselves (in the LLC agreement) how the profits and losses of the LLC are to be allocated and how and when distributions are to be made (similar to a Cayman Islands exempted limited partnership)

An LLC may be formed for any lawful business, purpose or activity and it has full power to carry on its business or affairs unless its LLC agreement provides otherwise.

The following statutory registers are required to be maintained for an LLC but, similarly to the requirement for a Cayman Islands exempted company, only an LLC’s register of managers is required to be filed with the Companies Registry:

a register of members;

a register of managers; and

a register of mortgages and charges.

The register of managers and register of mortgages and charges are required to be maintained in a manner similar to the register of directors and register of mortgages and charges for a Cayman Islands exempted company.

Subject to any express provisions of an LLC agreement to the contrary, a manager of the LLC will not owe any duty (fiduciary or otherwise) to the LLC or any member or other person in respect of the LLC other than a duty to act in good faith in respect of the rights, authorities or obligations which are exercised or performed or to which such manager is subject in connection with the management of the LLC provided that such duty of good faith may be expanded or restricted by the express provisions of the LLC agreement.

The Segregated Portfolio Company (“SPC”) is increasingly being used as a structure for investment funds, what do think explains this increasing popularity?

Under the Cayman Islands Companies Law (the “Companies Law”), an SPC is an exempted company which has been registered as a segregated portfolio company. It has full capacity to undertake any object or purpose subject to any restrictions imposed on the SPC in its Memorandum of Association. The Memorandum of Association of an SPC usually gives the SPC full capacity to pursue very broad objects. Once registered under the Companies Law, an SPC can operate segregated portfolios (“SPs”) with the benefit of statutory segregation of assets and liabilities between portfolios.

The appeal of SPCs extends beyond investment funds and the structure is often used in capital markets and securitisation transactions. In the investment funds context, SPCs greatly enhance the versatility and efficiency of Cayman Islands fund structures. It allows investors to access different trading strategies or investments, different markets or different managers through a single corporate vehicle whilst simultaneously providing the segregation of assets and liabilities through each SP (unlike, for example, a ‘multi class’ fund where there is typically a single legal entity offering various classes of shares designated according to the designated portfolio investment) and avoiding cross class liability issues which could arise with ‘multi class’ funds.

The Companies Law permits an SPC to create one or more SPs in order to segregate the assets and liabilities of the SPC held within one SP from the assets and liabilities of the SPC held within another SP of the SPC. The general assets and general liabilities of the SPC (i.e. assets and liabilities which cannot be properly attributed to a particular SP) are held within a separate general account rather than in any of the SP accounts. Each SP should have, as appropriate, its own bank account, brokerage account, and other accounts to hold its assets to avoid co-mingling with the assets of other SPs.

Figure 1. An unlimited number of SPs can be created by the SPC to hold various assets, employ different investment strategies or have varying sector focus.

The Companies Law requires that segregated portfolio assets must only be available and used to meet liabilities to the creditors of the SPC who are creditors in respect of that SP and who are thereby entitled to have recourse to the segregated portfolio assets attributable to that SP for such purposes. Segregated portfolio assets should not be available or used to meet liabilities to, and must be absolutely protected from, the creditors of the SPC who are not creditors in respect of that SP, and who accordingly are not entitled to have recourse to the segregated portfolio assets attributable to that SP.

Accordingly, a creditor will only have recourse to assets from SPs with which it has contracted and creditors will have no recourse to the assets of other SPs of the SPC which are protected under the Companies Law. This statutory protection afforded under the Companies Law to the assets of each SP is one of the key feature and benefit of the SPC structure.

Why is the SPC being used increasingly as a fund structure?

The Cayman Islands continue to be one of the leading offshore jurisdictions for the establishment of hedge funds, private equity funds, real estate funds, and other asset classes. The versatility and efficiency of the SPC structure in terms of the ability to effectively ‘ring fence’ certain assets and liabilities under the same investment portfolio and benefit from statutory recognition of that ring-fencing have made the SPC increasingly attractive in this environment. Like other exempted companies, there are no residency restrictions on Directors or Shareholders of an SPC and there are no Cayman Islands taxes on the SPC or its shareholders.

The SPC corporate structure allows a fund manager to employ different trading strategies, and/or establish different investment platforms, and/or provide access to different markets, and/or different trading advisers through a single corporate vehicle whilst simultaneously providing the segregation of assets and liabilities through each SP. Fund managers are able to market an SPC fund as being able to provide the ability to set up a statutory “ring-fence” to protect against cross liability issues relating to the assets and liabilities of the various SPs within the SPC. The SPC structure is being used as an investment platform on which investors can form different SPs to hold varying asset classes (e.g. real estate, intellectual property, stocks and shares, and distressed assets) and have their investments managed separately from other investments held by other SPs on the same SPC platform.

The SPC will have a Board of Directors. In addition, each SP can have its own segregated portfolio directorate or investment or management committee which effectively controls and manages the operations of the relevant SP. The segregated portfolio directorate, investment or management committee obtains its powers through powers delegated to it by the Board of Directors of the SPC.

This Article first appeared in Asian Legal Business December 2016 Issue – Guide to BVI and Cayman

Gary Smith

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

The Nuts and Bolts of the Cayman Islands Merger Regime

The Cayman Islands (Cayman) has been the leading offshore jurisdiction for merger and acquisition (M&A) activity over the last three (3) years. In 2015, Cayman-incorporated companies were the target of 863 transactions worth a combined value of USD116.41bn. The value was more than twice the amount of the British Virgin Islands with USD49.62bn (with 387 M&A transactions) and well in excess of Bermuda with 498 M&A transactions with a combined value of USD67.57bni. In 2016, Cayman-incorporated companies again led the way in terms of offshore M&A activity and were the target of transactions worth a combined USD68.85bn followed by the British Virgin Islands with USD41.65bn and Bermuda with USD41.25bnii. By way of comparison, Hong Kong incorporated companies were the target of transactions worth a combined USD33.19bn in 2016iii. Cayman-incorporated companies were the target of transactions worth a total USD80bn in 2017 and USD60bn in the first half of 2018.

The Cayman Merger Law regime is attractive for both companies and investors, due to the process being relatively straightforward and simpler than either a takeover offer (tender offer) under section 88 of the Cayman Islands Companies Law or a court-approved scheme of arrangement under section 86 or 87 of the Cayman Islands Companies Law. Set out below are the basic steps in the process of effecting a merger under Part XVI of the Cayman Islands Companies Law (As Revised).

1. s of the take-private transaction) (the “Buyout Group”) to take on finance and to be ultimately merged with the company which is the target of the take-private (“Target”). Forming MergerCo. The most straightforward structure used for a merger take-private is that a new company (“MergerCo”) is formed in the Cayman Islands by the investors adhering to the takeover group (often involving the founders/managers of the listed company, its parent and/or several private equity (PE) investors acting as sponsors for the purpose

2. Take-Private Offer. After obtaining legal and financial advice, the Buyout Group agrees on the terms of the proposed merger take-private and the consideration which would be offered to the shareholders of the Target and makes an offer to the Board of the Target (the “Initial Take-Private Offer”). Since most of the take-private transactions are initiated by or with involvement of the management or certain shareholders represented at Board level, the merger process requires that a special committee formed of independent directors (the “Special Committee”) be designated to review the take-private offer and negotiate on behalf of the Target with the Buyout Group. This is both to ensure that the Board is in compliance with the fiduciary duties it owes the Target, and to avoid any accusation of self-dealing.

3. Negotiations. The Special Committee reviews and negotiates the offer with the help of its own independent legal and financial advice, which may lengthen the process. Overall, the typical mission of the Special Committee is to: (i) investigate and evaluate the Initial Take-Private Offer, (ii) discuss and negotiate any terms of the merger agreement (the “Merger Agreement”), (iii) explore and pursue any alternatives to the Initial Take-Private Offer as the Special Committee deems appropriate, including maintaining the public listing of Target or finding an alternative buyer, (iv) negotiate definitive agreements with respect to the take-private or any other transaction, and (v) report to the Board the recommendations and conclusions of the Special Committee with respect to the Initial Take-Private Offer.

4. Board Approval. The directors of each company participating in a merger (MergerCo and Target) are required to approve the terms and conditions of the proposed merger (the “Plan of Merger”), including, among other things:

i. how shares in each participating company will convert into shares in the surviving company or other property (e.g. cash payable to shareholders);

ii. what rights and restrictions will attach to the shares in the surviving company;

iv. how the Memorandum and Articles of Association of the surviving company are amended; and

v. what are the amounts or benefits paid or payable to any director consequent upon the merger.

5. Shareholder Approval. For each constituent company (MergerCo and Target), the Plan of Merger is required to be authorized by a special resolution of the shareholders who have the right to receive notice of, attend and vote at the general shareholders’ meeting (“EGM”), voting as one class with at least two-thirds majority.

6. Consents. Each participating company must also obtain the consent of (i) each creditor holding a fixed or floating security interests, and (ii) any other relevant consents or filings with relevant regulatory authorities, such as the Cayman Islands Monetary Authority or authorities in the overseas jurisdiction where the Target is registered and/or operates.

7. Filing and Registration. After obtaining all necessary authorizations and consents, the Plan of Merger is required to be signed by a director on behalf of each participating company and filed with the Cayman Islands Registrar of Companies, who will register the Plan of Merger and issue a certificate of merger.

8. Effective Date. The merger will be effective on the date that the Plan of Merger is registered by the Registrar of Companies unless the Plan of Merger provides for a later specified date or event. Upon the effective date, all rights and assets of each of the participating companies shall immediately vest in the surviving company and, subject to any specific arrangements, the surviving company shall inherit all assets and liabilities of each of the participating companies (MergerCo and Target).

9. Shareholder Dissent. Any shareholder of a company participating in the merger is entitled to payment of fair value of its shares upon dissenting from the merger under Section 238 of the Cayman Islands Companies Law. Fair value can either be agreed between the parties or determined by the Cayman Court.

i Figures from the M&A Latin America and Global Review published by Bureau van Dijk (Zephyr) for the year 2016.

ii Ibid.

iii Figures from the M&A Greater China Review published by Bureau van Dijk (Zephyr) for the year 2016.

iv Or such higher threshold as may be specified in the Memorandum and Articles of Association.

v Or, if the secured creditor fails to grant such consent, the company may apply to the court for a waiver.

vi If date or event is not more than 90 days after the Plan of Merger is registered by the Registrar of Companies.

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

In the prevailing economic conditions, investors in offshore companies registered in the Cayman Islands or the British Virgin Islands (“BVI”) are increasingly being forced to consider their rights against directors who may have been responsible for mismanagement of the company’s affairs. Minority shareholders, in particular, are keen to understand the availability of remedies which allow them to overcome “wrongdoer control”. That is to say, the common situation where the composition and direction of the board is controlled by majority shareholders. We have set out below a brief summary of the duties owed by directors and the remedies available to shareholders in each of these jurisdictions.

What is scope of director’s duties?

Cayman Islands

The duties of a director of a Cayman Company are found in the common law and include the duty to act bona fide in the best interests of the company, a duty not to exercise his or her powers for purposes for which they were not conferred and not to make secret profits.

British Virgin Islands

The law governing the “duties of directors and conflicts” is set out in Division 3 of Part VI of the BVI Business Companies Act, 2004 (as amended) (the “Act”). These largely mirror the position at common law and include, for example, (a) the duty to “act honestly and in good faith and in what the director believes to be in the best interests of the company”(s.120); (b) the duty to exercise powers “for a proper purpose” and a requirement that a director “shall not act, or agree to the company acting, in a manner which contravenes this Act or the memorandum or articles of the company (s.121)”; and a requirement that “a director of a company shall forthwith after becoming aware of the fact that he is interested in a transaction entered into or to be entered into by the company, disclose the interest to the board of the company (s.124). It is interesting to note that subsections 120 (2)-(4) of the Act provide that a director of a company that is a wholly-owned subsidiary, subsidiary or joint venture company may, subject to certain requirements, act in the best interests of the relevant parent, or in the case of the joint venture company, the relevant shareholders even though such act may not be in the best interests of the company of which he is a director.

What are the standard director’s duties?

Cayman Islands

The common law applies to the Cayman Islands such that a director is under a duty to act with reasonable care, skill and diligence in the performance of his or her duties. In the English authority of Re City Equitable Fire Insurance Co [1925] Ch. 407 it was held that “a director need not exhibit in the performance of his duties a greater degree of skill than may reasonably be expected from a person of his knowledge and experience. This highly subjective test, however, has been met with increasing criticism in more recent years and there is further English authority to suggest that directors are nevertheless subject to an objective duty to “take such care as an ordinary man might be expected to take on his own behalf” (Dorchester Finance Co v Stebbing [1989] BCLC 498 (decided in 1977)). As such, a distinction appears to be drawn between the duty of skill on the one hand and the duty to take care on the other. However, in Re City Equitable Fire Insurance Co it was further held that “in respect of all duties that, having regard to the exigencies of business, and the articles of association, may be properly left to some other official, a director is, in the absence of grounds for suspicion, justified in trusting to that official to perform such duties honestly.”

British Virgin Islands

Section 122 of the Act provides that “A director of a company, when exercising powers or performing duties as a director shall exercise the care, diligence and skill that a reasonable director would exercise in the same circumstances taking into account, but without limitation:

(a) the nature of the company;

(b) the nature of the decision; and

(c) the position of the director and the nature of the responsibilities undertaken by him.”

This duty is qualified by s. 123 to the extent that the director of a company is entitled to rely upon the books of the company in question and/or employees and professional advisers provided that in doing so he or she acts in good faith, undertakes a proper inquiry where this is warranted and has no knowledge of a reason for not placing reliance on the said books and records.

What are the key remedies available to a member or shareholder?

Cayman Islands

The following remedies are available to a member of a Cayman Company:

(a) A personal action against the company (where the company has breached a duty which is owed to the member personally);

(b) A representative action (similar to a personal action such a claim would lie for breach of a duty owed to a group of shareholders)

(c) A derivative, or multiple derivative claim (this is the most common type of action. See below); or

A petition to wind up the company on just and equitable grounds. (This is seen as a last resort because it risks placing the company into liquidation although s.95(3) of the Companies Law (2013 Revision) (the “Law”) provides the Court with the option of making an alternative order. See below).

British Virgin Islands

The members of a BVI company may pursue the following remedies:

(a) A personal action pursuant to section 184G of the Act (on the same grounds as at common law in the Cayman Islands)

(b) A representative action pursuant to section 184H which provides that the Court may appoint a member “to represent all or some of the members having the same interest and may, for that purpose, make such order as it thinks fit, including an order (a) as to the control and conduct of the proceedings; (b) as to the costs of the proceedings; and (c) directing the distribution of any amount ordered to be paid by a defendant in the proceedings among the members represented.

(c) A derivative claim pursuant to section 184C; or

(d) An unfair prejudice claim pursuant to section 184I.

(c) and (d) above are the most common type of remedies sought by minority shareholders (see below).

What are derivative claims and what is their legal basis?

Cayman Islands

A derivative action is a claim commenced by one or more minority shareholders on behalf of a company of which they are a member in respect of loss or damage which that company has suffered. Such a claim can only be brought in certain circumstances and amounts to an exception to the rule that a company, as a separate legal person, should sue and be sued in its own name (often referred to as the rule in the English authority of Foss v Harbottle (1843) 2 Hare 461; 67 E.R 189). In the Cayman Islands the law governing derivative actions is drawn from the common law rather than statute.

British Virgin Islands

While the English common law applies in the British Virgin Islands “members remedies” have been given a statutory footing in Part XA of the Act (see below).

What is the procedure for commencing a derivative action?

Cayman Islands

As with the majority of actions commenced in the Cayman Islands, derivative claims are normally begun by serving a writ and statement of claim on the relevant defendant or defendants. Grand Court Rules O.15, r. 12A provides that where the defendant gives notice of an intention to defend the claim then the plaintiff must apply to the Court for leave to continue the action. Such an application should be supported by affidavit evidence verifying the facts on which the claim and entitlement to sue on behalf of the company are based. Pursuant to Grand Court Rules O.15 r.12A(8) on the hearing of the application, the Court may grant leave to continue the action for such period and upon such terms as it thinks fit, dismiss the action, or adjourn the application and give such direction as to joinder of parties, the filing of further evidence, discovery, cross-examination of deponents and otherwise as it considers expedient. In Renova Resources Private Equity Limited v Gilbertson and Others [2009] CILR 268, Foster., J affirmed the application in the Cayman Islands of the test to be applied in determining whether to grant leave to continue the action put forward by the English Court of Appeal in Prudential Assurance Co Ltd v Newman Industries Ltd (No.2) [1981] Ch 257. Foster, J., held that: “(…) there are two elements to this: first the plaintiff [is] required to show prima facie that there [is] a viable cause of action vested in the company and, secondly, that the alleged wrongdoers [have] control of the company (or could block any resolution of the company or the board) and thereby prevent the company bringing an action against themselves.”

British Virgin Islands

Section 184C (1) of the Act provides that subject to certain exceptions “the Court may, on the application of a member of a company, grant leave to that member to (a) bring proceedings in the name and on behalf of that company; or (b) intervene in the proceedings to which the company is a party for the purpose of continuing, defending or discontinuing the proceedings on behalf of the company.” Section 184C(2) provides that “without limiting subsection (1), in determining whether to grant leave under that subsection, the Court must take the following matters into account: (a) whether the member is acting in good faith; (b) whether the derivative action is in the interests of the company taking account of the views of the company’s director’s on commercial matters; (c) whether the proceedings are likely to succeed; (d) the costs of the proceedings in relation to the relief likely to be obtained; and (e) whether an alternative remedy to the derivative claim is available.” Pursuant to subsection (3) leave to bring or intervene in proceedings may be granted “only if the Court is satisfied that: (a) the company does not intend to bring, diligently continue or defend or discontinue the proceedings as the case may be; or it is in the interests of the company that the conduct of the proceedings should not be left to the directors or to the determination of the shareholders or members as a whole. Such an application for leave should be made to the Court supported by affidavit evidence.

Is it possible to bring multiple derivative claims (“MDCs”)?

Cayman Islands

In Renova the Grand Court held that in appropriate circumstances MDCs would be permitted. In that case, the plaintiff had brought an action in respect of loss incurred by a wholly-owned subsidiary of the company in which it was a shareholder and therefore loss to the subsidiary caused indirect loss to its parent company and shareholders. However, the rule against the recovery of reflexive loss applied such that a shareholder or parent company would not be permitted to claim for indirect losses which mirrored those losses suffered directly by the relevant subsidiary or indeed sub-subsidiary on who behalf action was being brought.

British Virgin Islands

In Microsoft Corporation v Vandem Ltd BVIHCVAP2013/0007 the Eastern Caribbean Court of Appeal held that BVI law which has been codified in this area “does not permit double derivative actions.” That said, recent English authority such as Universal Project Management Services Ltd v Fort Gilkicker Ltd [2013] 3 WLR concerning the interpretation of s.260 the English Companies Act, 2006 may open up arguments that such actions are nevertheless available in the jurisdiction at common law.

What remedies are available for unfair prejudice and what is their legal basis?

Cayman Islands

Pursuant to section 92 of the Companies Law (2013 Revision) the Court may wind up a company if it is of the opinion that it would be just and equitable for it to do so. Section 95(3) provides that where such a petition “is presented by members of the company as contributories on the ground that it is just and equitable that the company should be wound up, the Court shall have jurisdiction to make the following orders, as an alternative to a winding-up order, namely –

(a) an order regulating the conduct of the company’s affairs in the future;

(b) an order requiring the company to refrain from doing or continuing an act complained of by the petitioner or to do an act which the petitioner has complained it has omitted to do;

(c) an order authorising civil proceedings to be brought in the name of and on behalf of the company by the petitioner on such terms as the Court may direct; or

an order providing for the purchase of the shares of any members of the company by other members or by the company itself and, in the case of a purchase by the company itself, a reduction of the company’s capital accordingly.

British Virgin Islands

Section 184I of the Act provides that “a member of a company who considers that the affairs of the company have been, are being or are likely to be, conducted in a manner that is, or any act or acts of the company have been, or are, likely to be oppressive, unfairly discriminatory, or unfairly prejudicial to him in that capacity, may apply to the Court for an order under this section.” Section 184I(2) provides that “if on an application under this section, the Court considers it just and equitable to do so, it may make such order as it thinks fit, including, without limiting the generality of this subsection, one or more of the following orders:

(a) in the case of a shareholder, requiring the company or any other person to acquire the shareholder’s shares;

(b) requiring the company or any other person to pay compensation to the member;

(c) regulating the future conduct of the company’s affairs;

(d) amending the memorandum and articles of the company;

(e) appointing a receiver of the company;

(f) appointing a liquidator of the company under section 159(1) of the Insolvency Act on the grounds specified in section 162(1)(b) of that Act;

(g) directing the rectification of the records of the company;

setting aside any decision made or action taken by the company or its directors in breach of this Act or the memorandum or articles of the company.

This Briefing Note is not intended to be a substitute for specific legal advice or a legal opinion. It deals in broad terms only and is intended to merely provide a brief overview and general guidance only. For more specific advice on the laws in the Cayman Islands, please contact:

In the previous issues of our series of legal insights on owning intellectual property (IP) through a Cayman Islands corporate structure, we presented a brief overview of the new trademark registration process which became effective in the Cayman Islands as at 1st August 2017 (see The New Cayman Islands Trademarks Regime).

In the meantime, blockchain technologies and ICOs have gained increasing popularity all over the world and in the Cayman Islands as well (see our FinTech series including Top Ten Risks for the Crypto-Currency Investor: A View from the Cayman Islands and Cayman Islands Legal Perspective on the Regulation of Initial Coin Offerings (ICOs)).

Confident in the security and their uniqueness or blinded by the open source aspects of their technology, blockchain start-ups may tend to forget one of the basic tenets of entrepreneurship: making certain that any newly generated intellectual property is well-protected. Beyond block-chain technology, commercial names and trademarks may become extremely valuable. If a block-chain start-up incorporates in the Cayman Islands, it now has the option of registering its name and logo in the Cayman Islands as well, providing additional protection after the launch or the projected Initial Coin Offering (ICO) or Initial Token Offering (ITO).

Three Simple Steps to Register Name & Logo:

Be Original & Distinctive: A trade mark1 which lacks distinctive character, which is customary in the current language or the established practices of the trade, or which designates characteristics of goods or services will be refused from registration.

Check Availability: Identical or similar trade marks cannot be registered for similar services, while similar trade marks may only be registered subject to the consent of the holder of the earlier mark2 . In addition, trade marks which take unfair advantage of, or are detrimental to, the character or the repute of an earlier similar mark registered or otherwise protected in the Cayman Islands3 will not be accepted.

File Early: Once accepted, the trade mark will be published in the Intellectual Property Edition of the Cayman Islands Gazette, which triggers a sixty (60) day period for oppositions4 . From a strategic point of view, it is best to launch after the opposition period had lapsed and the trade mark registration is secured.

See also, for more information regarding the trademark registration and intellectual property pro-tection for FinTech companies, our alerts on The New Cayman Islands Trademarks Regime and Financial Technology Intellectual Property (FinTech IP) Welcome in the Cayman Islands.

1. Article 23(1) of the Trade Marks Law, 2016

2. Article 25(6) of the Trade Marks Law, 2016

3. Article 25(3) of the Trade Marks Law, 2016

4. Article 16(2) of the Trade Marks Law, 2016

This is not intended to be a substitute for specific legal advice or a legal opinion. For specific advice, please contact:

Ramona Tudorancea

Corporate / M&A Specialist

E: ramona.tudorancea@loebsmith.com

W: www.loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

The Cayman Islands have now brought into effect the long-awaited Limited Liability Companies Law, 2016 (the “LLC Law”) which introduces a new Cayman Islands limited liability company (an “LLC”). The LLC Law was published on 8th June 2016 but had not been brought into effect until 8th July 2016 in order to provide the Companies Registry with sufficient time to implement internal systems for dealing with registration of new LLCs. The Companies Registry is currently undertaking pilot testing of its internal systems and has advised that it expects to be able to accept registration applications for new LLCs before 15th July 2016.

Key Features of Cayman LLCs

- An LLC formed under the LLC Law will be similar in structure to that of the Delaware LLC as the LLC Law is broadly based on the Limited Liability Company Act in the State of Delaware. However, the LLC Law has also preserved the broad legal principles applicable to Cayman Islands companies and the rules of equity and common law. Section 3 of the LLC Law expressly states that: “The rules of equity and of common law applicable to companies registered in the Islands, as modified by the Companies Law and any other Laws in force in the Islands applicable to such companies, shall apply to a limited liability company, except in so far as such rules and law or modifications thereto are inconsistent with the express provisions of this Law or the nature of a limited liability company”.

- An LLC is a corporate entity which has separate legal personality to its members.

- Formation of an LLC is straightforward. It requires the filing of a registration statement with the Companies Registry and payment of the requisite Government fee.

- An LLC must have at least one member. It can be member managed (by some or all of its members) or the LLC agreement can provide for the appointment of persons (who need not be members) to manage and operate the LLC.

- The liability of an LLC’s members is limited. Members can have capital accounts and can agree amongst themselves (in the LLC agreement) how the profits and losses of the LLC are to be allocated and how and when distributions are to be made (similar to a Cayman Islands exempted limited partnership).

- An LLC may be formed for any lawful business, purpose or activity and it has full power to carry on its business or affairs unless its LLC agreement provides otherwise.

- An LLC may (but is not required to) use one of the following suffixes in its name: “Limited Liability Company”, “LLC” or “L.L.C.”.

- The following statutory registers are required to be maintained for an LLC but, similarly to the requirement for a Cayman Islands exempted company, only an LLC’s register of managers is required to be filed with the Companies Registry:

-

- a register of members;

- a register of managers; and

- a register of mortgages and charges.

The register of managers and register of mortgages and charges are required to be maintained in a manner similar to the register of directors and register of mortgages and charges for a Cayman Islands exempted company.

- Subject to any express provisions of an LLC agreement to the contrary, a manager of the LLC will not owe any duty (fiduciary or otherwise) to the LLC or any member or other person in respect of the LLC other than a duty to act in good faith in respect of the rights, authorities or obligations which are exercised or performed or to which such manager is subject in connection with the management of the LLC provided that such duty of good faith may be expanded or restricted by the express provisions of the LLC agreement.

Expected Benefits of the New LLC Vehicle

Under the LLC Law, it is now possible to:

- Form and register a new LLC;

- Convert an existing Cayman Islands exempted company into an LLC;

- Merge an existing Cayman Islands exempted company into an LLC; and

- Migrate an entity formed in another jurisdiction (e.g. Delaware) into the Cayman Islands as an LLC.

It is expected that the new Cayman Islands LLC structure will be attractive for general partner entities and other carried interest distribution vehicles. It may also prove attractive for management company entities and possibly for offshore funds in order to align the rights of investors between onshore and offshore investment funds in a master/feeder structures.

For Specific advice on Cayman Islands limited liability companies, please contact either of:

E: gary.smith@loebsmith.com

E yun.sheng@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

The Cayman Islands Government has issued The Confidential Information Disclosure Bill, 2016 (“Confidentiality Bill”) which, once it comes into force will bring into effect a fundamental overhaul of confidentiality laws in the Cayman Islands.

The introduction of the Confidentiality Bill is part of a series of actions being taken by the Cayman Islands Government to the assist global efforts to increase transparency.

Existing Law

Under the existing law, which is found in The Confidential Relationships (Preservation) Law (2015 Revision), it is a criminal offence to divulge or attempt, offer or threaten to divulge “confidential information” (which is defined as including information concerning any property which the recipient thereof is not, otherwise than (in the narrowly construed exception of) “in the normal course of business”, authorised by the principal to divulge) except in a limited number of specified circumstances.

Notwithstanding the criminal penalties that follow a breach of the existing law, there has not been a criminal conviction under the existing law since its original enactment over 40 years ago.

The prohibition applies with respect to business of a professional nature (e.g. the relationship between a bank, trust company, an attorney-at-law, an accountant, an estate agent, an insurer, or a broker and its client) which arises in or is brought to the Cayman Islands and to all persons coming into possession of such information at any time thereafter whether they be within the jurisdiction or not.

As mentioned above, disclosure is permitted in a number of specified circumstances (e.g. (i) in respect of any professional person acting in the normal course of business, or with the consent, express or implied, of the relevant principal; or (ii) in response to statutory requests from certain criminal or regulatory authorities (e.g. the Cayman Islands Monetary Authority), or (iii) a court order).

Proposed new Law

The Confidentiality Bill proposes the following key amendments:

It will no longer be a criminal offence to breach a duty of confidentiality.

In future it will be necessary to assess whether the information imparted was subject to a duty of confidence in the first place. This will effectively shift the burden of proof from showing that the disclosure falls within an exception to the current prohibition, to showing that the information imparted was in fact subject to a duty of confidence.

Where a person owes a duty of confidence, that person’s disclosure of such information within a widened list of specified circumstances will not constitute a breach of the duty of confidence and a person will not be able to sue the discloser.

A person who discloses confidential information in relation to a serious threat to the life, health, safety of a person or in relation to a serious threat to the environment will have a defence to legal action for breach of a duty of confidence, as long as the person acted in good faith and in the reasonable belief that the information was substantially true and disclosed evidence of a serious threat to life, health, safety of a person or of a serious threat to the environment.

This publication is not intended to be a substitute for specific legal advice or a legal opinion. It deals in broad terms only and is intended to merely provide a brief overview and general guidance only. For more specific advice on the confidentiality laws in the Cayman Islands, please contact:

Gary Smith

Partner

E: gary.smith@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

As the deadline for the filing of notifications to the Cayman Islands Tax Information Authority via the Cayman AEOI Portal in respect of (i) entities formed in 2015 for U.S. FATCA purposes and (ii) entities for UK CDOT purposes, approaches on 10 June 2016, we revisit some of the key issues on the Common Reporting Standard (CRS) and its application to Cayman Islands formed Investment Entities.

For specific advice on U.S. FATCA, UK CDOT, and the CRS as they relate to Cayman Islands entities, please contact any of:

E lorna.williams@loebsmith.com

Gary Smith

Partner