Guidance for Directors registered with the Cayman Islands Monetary Authority

Renewal of Director registration

Directors who are registered with CIMA in accordance with The Directors Registration and Licensing Law, 2014 (“DRLL”) in connection with being a Director of an entity that is registered with CIMA (e.g. registered Mutual Fund or an investment management or investment advisory entity that has “Excluded Person” status under the Securities Investment Business Law (2015 Revision)) (a “Covered Entity”) should by this time of the year have received a reminder from CIMA to renew registration via the CIMA portal https://gateway.cimaconnect.com/. A Director should renew his or her registration with CIMA if he or she will continue to be a Director of one or more Covered Entity that either (1) will carry on business for some or all of 2017, or (2) is in the process of winding down such business but the process will not cease prior to 31 December 2016.

Resignation from a Covered Entity

CIMA has stated[i] that if a Director no longer wishes to be registered or licensed as a Director of a Covered Entity, the Director must liaise with the Covered Entity’s registered office and ensure that CIMA receives written resolutions or an updated register of directors, stamped by the Registrar of Companies, to duly notify CIMA of the Director’s resignation from that Covered Entity.

Resignation of a Director from a Covered Entity will not automatically result in a surrender of the Director’s registration or licence under the DRLL.

Surrender of Director registration

CIMA has also stated[ii] that if a Director no longer wishes to be registered or licensed as a Director in accordance with the DRLL, he or she must first resign as a Director of all Covered Entities, then log into the CIMA portal, complete the requisite information under “Surrender”, and pay the relevant surrender fee (US$731.71).

Once the Director has paid the surrender fee, CIMA will check its records to confirm that the Director is no longer listed as a Director on any Covered Entity. If he or she remains as a Director on a Covered Entity, CIMA has stated that it will be unable to process the Director’s surrender application.

In addition to submitting the surrender fee, the Director is required to submit a formal letter which MUST contain the following information:

1. that he or she has resigned as a Director of all Covered Entities;

2. that he or she no longer plans to act as a Director on any Covered Entity; and

3. that if he or she would like to act on any other Covered Entity or wishes to resume directorship services after he or she has surrendered his or her registration or licence, he or she will re-apply under the DRLL.

The Director is responsible for updating his or her records accordingly and must complete the requirements to surrender his or her registration or licence before the 31st December in order to avoid accruing next year’s annual fees, as well as penalties calculated at 1/12th of the annual fee for every month or part of a month after the 15th of January in each year that the fee is not paid.

As stated above, Directors who will continue to provide directorship services and wish to remain current with their registration or licence status under the DRLL MUST, on or before the 15th of January in each calendar year, renew their registration or licence through the CIMA portal.

For specific advice on renewal or surrender under the DRLL or resignation from a Covered Entity, please contact any of:

E gary.smith@loebsmith.com

E yun.sheng@loebsmith.com

[i] CIMA’s Supervisory Issues & Information Circular– Second Edition issued in October 2016

[ii] CIMA’s Supervisory Issues & Information Circular– Second Edition issued in October 2016

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

On October 25, Loeb Smith Attorneys’ Cayman Islands-based corporate lawyer Ramona Tudorancea will chair and moderate the panel titled “Caribbean Offshore Jurisdictions as Stepping Stones for Cross-Border Investments in the Americas“, scheduled as part of the Miami Fall Meeting of the Section of International Law of the American Bar Association and taking place at the JW Marriot Marquis, Met Ballroom 4, starting 4.30 PM.

Panelists include James H. Barrett from Baker & McKenzie LLP (Miami), Fernanda Bastos from Buhatem, Souza, Cescon, Barrieu & Flesch Advogados (Brazil), Pablo Falabella from Bulló Abogados (Argentina), Fabian A. Pal (Miami), and Kevin P. Scanlan from Kramer Levin Naftalis & Frankel LLP (New York).

The panel is sponsored by the Lawyers Abroad Committee (LAC), where Ms. Tudorancea currently serves as a Vice-Chair of Publications, and co-sponsored by the International M&A and Joint Venture Committee, the Latin America and Caribbean Committee, and the International Tax Committee.

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Introduction

The Cayman Islands have been the leading offshore jurisdiction for merger and acquisition (M&A) activity over the last few years, with a steady flow of over USD77bn in combined value of target companies for 2016 and 2017, and a peak of over USD115bn in 2015. By way of comparison, for 2017, the combined value of transactions targeting companies incorporated in the British Virgin Islands (BVI) and Hong Kong was USD37bn and USD40bn respectively1.

A significant portion of this M&A activity was related to merger take-privates involving Cayman-incorporated companies listed on U.S. stock exchanges, which were achieved through the Cayman Islands statutory merger regime (the “Cayman Merger Law”). The related transactions also generated a significant number of litigated cases in the Cayman Islands, as any shareholder who is unhappy with the consideration offered as part of a merger may dissent and is entitled to payment of fair value of its shares under Section 238 of the Cayman Islands Companies Law (2018 Revision) (the “Companies Law”), and such fair value, if not agreed between the parties, is determined by the Grand Court of the Cayman Islands (the “Court”).

2017 Cases Favourable to Dissenting Shareholders

In 2017, several decisions issued by the Court improved upon and clarified the rights of minority shareholders dissenting from a merger, both in respect to procedural matters2, and by allowing the dissenting shareholders to benefit from interim payment relief3. However, the most significant development of the year 2017 had been the judgment issued on 25th April 2017 in the matter of Shanda Games Limited, when the Court reaffirmed its seminal decision in the matter of Integra Group on 28th August 2015, and decided that “fair value” was to be determined on the basis of the Company as a going concern immediately prior to the merger, without any minority discount.

The Court had based its decision on fair value valuation principles in Delaware and Canada because it was the Delaware and Canadian merger law regimes that had inspired the adoption of the Cayman Merger Law. The judgment in the matter of Shanda Games Limited also addressed many technical issues of valuation methodology (including the use of the discounted cashflow (“DCF”) model, how depreciation should factor into the valuation, taking account of trading at any point up until the valuation date, taking account of the actual or anticipated performance against the market, etc.).

Court of Appeal Judgment Regarding Shanda Games Limited

However, following an appeal brought by Shanda Games, the Cayman Islands Court of Appeal held on 6th March 2018 that, contrary to what had been previously decided by the Court, a “minority discount” should be applied in assessing the “fair value” of a dissenter’s shares. In so doing, the Court of Appeal decided to follow Shanda Games’ arguments that the trial judge should have taken into account English case law authorities before looking further to what the Delaware courts had determined.

The English case law authorities cited by the Court of Appeal discussed fairness (or rather unfairness) in the context of disputes with regard to schemes of arrangement and squeeze-outs mechanisms4. In Re Hoare & Co. Ltd (1933) 150 LT 374, cited by the Court of Appeal in paragraph 35 of its decision, the paragraphs cited make it clear that the reasoning for the English court’s conclusion that a minority discount did not make the scheme of arrangement unfair was that the scheme had gathered the approval of the required 90% of the shareholders affected by the offer. This fact, the English court reasoned, constituted prima facie evidence as to fairness and dissentients did not produce appropriate evidence to disprove it. In Re Linton Park plc [2005] EWHC 3545 (Ch); [2008] 17, the English court similarly states that “whether the package on offer is a fair price for the shares is a matter which the shareholders are far better to able to judge than the court, and for that reason the court will be very slow to depart from the majority view”. In Re Grierson, Oldham & Adams Ltd [1968] Ch 17, that the English court issues a substantial view on minority discounts by stating that “it is not unfair to offer a minority shareholder the value of what he possesses, i.e. a minority shareholding”.

Analysis

Admittedly, the adoption of a minority discount in the assessment of “fair value” is by itself a serious setback to dissenting shareholders utilising the Cayman Merger Law to obtain fair value for their shares. However, the consequences of the Court of Appeal’s decision in the matter of Shanda Games Limited may be more far-reaching.

It has been so far generally accepted under Cayman Islands law that under a scheme of arrangement or a statutory squeezeout under section 88 of the Companies Law dissenting shareholders would be “dragged along” if the scheme is approved or the conditions of the statutory squeeze-out are met without a requirement that the Court re-examines the “fair value” of the consideration offered to them. Also, it appears to have been generally accepted that the Court would not in fact intervene unless there is a clear case of unfair or prejudicial treatment of shareholders in these circumstances. It is this exact approach that is illustrated by the English case law authorities cited by the Court of Appeal and referred to above. This minimal level of intervention by the English courts with respect to valuation issues is well justified, as neither schemes of arrangement5 nor squeeze-outs6 are susceptible to the same measure of control (or abuse) by the buyout group in a merger take-private transaction as it is possible under the Cayman Merger Law:

i. a scheme of arrangement not only requires approval by 75% of shareholders in each class and 75% in value of creditors present and voting (a higher majority than required under the Cayman Merger Law), buta. founders or insiders may be treated by the Court as a separate class, which basically translates into a “majority of minority” requirement; and

b. dissenting shareholder are entitled to actually appear before the Court and argue against the scheme; and

ii. a statutory squeeze-out requires that at least 90% in value of shares affected by the offer (i.e. the shares not held by the buyout group) agree to the offer.

The above requirements, if met, translate into strong evidence of fairness with respect to consideration offered given the high thresholds for approval. Accordingly, it could be reasonably argued that there is less need for the Court, and no opportunity under Sections 86 and 88 of the Companies Law, to examine valuation issues.

Not so under Section 238 of the Companies Law, where the approval threshold, two-thirds majority of votes cast, is significantly lower and may be easily controlled by the buyout group itself.

The fact that the Court of Appeal chose to treat mergers, schemes of arrangement and squeeze-outs in a very similar manner with regard to valuation methodology could now open the door (even though this was not necessarily intended) to a dangerous blurring of categories which could lead to further shrinkage of the “fair value” standard under Section 238 of the Companies Law. For now, however, the existing legal principles governing determination of “fair value” for the dissenters’ shares remain unchanged subject to the exception of a minority discount being applied in recognition of the reality that dissenters hold a minority interest. The Honourable John Martin QC, in handing down the judgment of the Cayman Islands Court of Appeal stated:

“The position in the Cayman Islands is accordingly that there are now three mechanisms contained in the Companies Law by which the shares of dissentients may be acquired: by squeeze-out with a 90% majority, by scheme of arrangement with a 75% majority, and under section 238 with a two-thirds majority. Assuming, as I do, that the English approach to squeeze-outs and scheme of arrangement acquisitions would be applied in the Cayman Islands, those two mechanisms allow a minority discount to be applied to the cost of acquisition of dissentients’ shares. It seems to me unlikely in the extreme that the simplified merger and consolidation regime introduced as Part XVI of the Companies Law was intended to depart from that approach; it is to be presumed that the three mechanisms, contained in the same piece of legislation and capable of serving the same purpose in different ways, are to be construed from the same standpoint. Nothing in the wording of section 238 suggests that a different approach was intended; indeed, as Shanda pointed out, there is nothing in the wording of the section that suggests that the focus is to be on the value of the company rather than on the value of the shares. (…) For these reasons, it appears to me that section 238 requires fair value to be attributed to what the dissentient shareholder possesses. If what he possesses is a minority shareholding, it is to be valued as such, if he holds shares to which particular rights or liabilities attach, the shares are to be valued as subject to those rights or liabilities.” (Paragraphs 49-50 of the Court of Appeals decision in the matter of Shanda Games Limited).

This publication is not intended to be a substitute for specific legal advice or a legal opinion. For specific advice, please contact your usual Loeb Smith attorney or either:

E gary.smith@loebsmith.com

E ramona.tudorancea@loebsmith.com

1 Based on figures included in the Global M&A Review 2017 report published by Bureau van Dijk – A Moody’s Analytics Company.

2 In a decision Homeinns Hotel Group v Maso Capital Investments Limited and others dated 7th February 2017, the Court examined the extent of discovery by the parties which is necessary for valuation purposes and supported the dissenters’ position that the Court could order certain classes of documents to be provided by the Company. In the matter of Qihoo 360 Technology Co Ltd., on 24th July 2017, the Court confirmed that it does have the power to order the appointment of an independent expert in forensic information technology to conduct an audit to verify the Company’s compliance with its discovery obligations.

3 In an interim judgement issued on 26th January 2017 in the matter of Blackwell Partners LLC et al v. Qihoo 360 Technology Co Ltd., the Court decided that interim payments pursuant to the Grand Court Rules (G.C.R.) could be requested by dissenting shareholders and granted by the Court during the judicial proceedings initiated to determine the “fair value” of the dissenters’ shares under Section 238 of the Cayman Merger Law. A decision issued on 8th August 2017 in the matter of Qunar Cayman Islands Ltd. provided further guidance on interim relief when the Court reaffirmed that requests for interim payment can be made by dissenting shareholders as part of the Section 238 proceedings, and that the Court has jurisdiction to grant such payments, in an amount determined to be “just”. Finally, in the matter of Trina Solar Limited, in written judgments dated 18th July 2017 and 25th August 2017, the Court held that a consent order for an interim payment entered into between the Company and the minority shareholders dissenting from the merger was binding upon the Company when made.

4 The Court of Appeals specifically acknowledges this in paragraph 45 of the decision: “although the English cases do not concern an appraisal mechanism, or deal with a statutory standard of fair value, they are concerned with fair value of the shares”.

5 Section 86 of the Cayman Islands Companies Law

6 Section 88 of the Cayman Islands Companies Law

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Introduction

In our previous publication Interim Payment Relief: New Developments Regarding Dissenters’ Rights under Cayman Merger Law, we discussed a new and significant development for minority shareholders in their quest to obtain the “fair value” for their shares in the context of a merger take-private carried out under the Cayman Islands statutory merger regime (the “Cayman Merger Law”).

In an interim judgement issued on 26th January 2017 in the matter of Blackwell Partners LLC et al v. Qihoo 360 Technology Co Ltd., the Court decided that interim payments pursuant to the Grand Court Rules (G.C.R.) could be requested by dissenting shareholders and granted by the Court during the judicial proceedings initiated under Section 238 of the Cayman Merger Law. Dissenters’ rights to interim payments now seem entrenched after a second decision was issued on 8th August 2017 in the matter of Qunar Cayman Islands Ltd.

Building Blocks of the Dissenters’ Rights to Interim Relief:

Building upon the reasoning previously adopted by the Court in Qihoo 360 Technology Co Ltd., the recent ruling in Qunar Cayman Islands Ltd. provides further guidance on interim relief available as part of proceedings initiated under Section 238 of the Cayman Merger Law.

1. Availability of Interim Relief Confirmed: As expected, the recent judgment followed Qihoo 360 Technology Co Ltd. and confirmed that requests for interim payment can be made by dissenting shareholders as part of the Section 238 proceedings, and that the Court has jurisdiction to grant such payments, in an amount determined to be “just”. In the matter of Qunar Cayman Islands Ltd., the “just” payment was deemed to be equal to the amount of the merger consideration which had been offered generally to the shareholders by the company.

2. Evidence Needed for Interim Relief to be Granted: At this stage, it seems unlikely that any interim payments ordered as part of Section 238 proceedings will exceed the merger consideration as approved as part of the merger agreement, especially if, as was the case in Qunar Cayman Islands Ltd., the request for interim relief is made before any expert report is submitted on valuation issues. For the purposes of interim relief, however, the Court appears willing and able to rely entirely on the company’s affirmations that the merger price represented the fair value of shares, without requiring dissenters to present any additional “fair value” evidence.

3. Costs of the Interim Relief Application: At this stage and taking account that interim payments in the context of judicial proceedings initiated under Section 238 of the Cayman Merger Law are a new development, the Court decided not to grant the dissenters’ request that the company bear the costs of the application. However, in the future, it cannot be excluded that such request for costs be granted by the Court.

This is not intended to be a substitute for specific legal advice or a legal opinion. For specific advice, please contact:

Gary Smith

Ramona Tudorancea

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

In the previous issue of our series of legal insights on owning intellectual property (IP) through a Cayman Islands corporate structure, we presented a brief overview of the new trademark registration process introduced by the new Cayman Islands Trade Marks Law, 2016 and the Trade Marks Regulations, 2017 (see The New Cayman Islands Trademarks Regime). The new regime has now become effective as at 1st August 2017 (the “Effective Date“), and additional guidance has been released with respect to transitional provisions:

1. Existing Trade Marks: All existing trade marks will be considered as transferred to the new Register of Trade Marks until their scheduled renewal date, when they should be renewed in accordance with the New Trade Marks Regime. However, the Registrar is required to take the necessary steps to ensure that these existing trade marks are not inconsistent with the criteria for accepting registration of trade marks under the new law, i.e. that there are no absolute or relative grounds for refusal of registration. If there are grounds for refusal of registration, the registration of an existing trade mark may be declared invalid under Section 45 of the Trade Marks Law, 2016.

2. Expired or In-Abeyance Trade Marks: The trade marks which have expired prior to the Effective Date, and any trade marks currently held in abeyance for non-payment of annual fees will not be automatically transferred to the Register of Trade Marks, and owners of such trade marks are required to reapply to have their trade marks registered under the New Trade Marks Regime.

3. Transitional Provisions: All matters pending before the Court or the Registrar as at the Effective Date, for a decision on the basis of the previous trade mark registration regime will remain governed by the old law, as well as any infringement of a registered trade mark committed before the Effective Date.

This is not intended to be a substitute for specific legal advice or a legal opinion. For specific advice, please contact:

Ramona Tudorancea

E ramona.tudorancea@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Statutory Remedies

The Foreign Judgments Reciprocal Enforcement Law (1996 Revision) (the “Law”) allows a judgment creditor to apply for the judgment to be registered in the Grand Court and thereafter is deemed to have the same force and effect as Judgment of the Grand Court. However, at present the Law extends only to the enforcement of Australian Judgments.

Common Law Remedies

All other foreign judgments must be enforced at common law. This includes judgments obtained in the United Kingdom and the United States. To do this, it is necessary to issue a writ of summons in the Grand Court to sue upon the foreign judgment and thereafter seek summary judgment. A foreign judgment will only be susceptible to enforcement in this way if it is final and conclusive (although this would appear to include summary and default judgments obtained in foreign jurisdictions). It is no longer necessary for a foreign judgment to be for a specified sum. In Badone v Sol Properties [2008] CILR, the Grand Court was willing to enforce a foreign judgment for specific performance of an agreement to transfer shares. Non-money foreign judgments would now appear to be capable of enforcement where is just to do so and such enforcement would not favour foreign litigants over domestic litigants, or undermine due process in the Cayman Islands. Further, in order for a foreign judgment to be enforced it will be necessary to satisfy the Grand Court that the foreign Court had jurisdiction over the defendant and that enforcement is not against public policy. For example, the Grand Court will not enforce judgments relating to foreign taxation. It is important to bear in mind that the enforcement of a foreign judgment at common law may require an application for leave to serve the defendant outside of the jurisdiction of the Cayman Islands.

This Briefing Note is not intended to be a substitute for specific legal advice or a legal opinion. For more specific advice on the enforcement of foreign judgments in the Cayman Islands, please contact:

Gary Smith

Ramona Tudorancea

E ramona.tudorancea@loebsmith.com

The protection of intellectual property (IP) rights in the Cayman Islands and in the British Virgin Islands (BVI) depends on the type of IP right (e.g. trademarks, patents and designs). The Cayman Islands and the BVI are British Overseas Territories and so the nature of IP protection in each jurisdiction is historically influenced by UK IP protection laws.

Which Agency administers Intellectual Property?

Cayman: Laws relating to IP in the Cayman Islands are administered by the Cayman Islands Intellectual Property Office (CIIPO).

BVI: Laws relating to IP in the BVI are administered by the BVI Office of the Registrar of Trade Marks, Patents & Copyright within the Registry of Corporate Affairs.

Types of Intellectual Property

Trademarks

Cayman Islands: Until 31 July 2017, the Cayman Islands offered trademark protection by way of extension of an existing UK trademark registration and also by the extension of an EU trademark registration; however, direct national filings in the Cayman Islands were not an option. For businesses (both local and foreign) whose interests were principally located in the Americas and the Caribbean, this resulted in increased trademark prosecution costs since they had to first secure protection in a foreign jurisdiction before they could apply in the Cayman Islands. In many cases such businesses would have had no bona fide intention to use the relevant mark in the first filing jurisdictions, thereby falling short of one of the requirements for UK trademark filings and calling into question the validity of the resulting registration of any extensions filed.

BVI: Until 31 August 2015, the BVI offered a dual trademark filing system under which trademark protection could be secured for goods and services on application to extend a UK trade mark registration to the BVI and/or, for goods only, on the filing of a trade mark application directly in the BVI.

Both jurisdictions modernized their trademark laws in 2015 (BVI) and 2017 (Cayman Islands) and as of 1 September 2015 (BVI) and 1 August 2017 (Cayman Islands) it is no longer possible to extend existing foreign trademark registrations to either jurisdiction. All existing trademark registrations were transferred over to the new registers. Since the implementation of the respective changes in law only the direct registration of trademarks in each jurisdiction is permitted.

Each jurisdiction now offers direct registration systems with some key common characteristics, including:

- the Nice Classification system as a mode of classifying goods and services under a trademark;

- multi-class filings;

- similar prosecution processes and formalities: filing, examination, acceptance, publication, registration;

- similar criteria for assessing the registrability of a trademark on both absolute and relative grounds;

- disclaimer and limitation practices as a condition to registration in certain cases;

- similar trademark opposition periods (three (3) months in the BVI and sixty (60) days in the Cayman Islands);

- provisions for the registration of certification and collective trademarks;

- an initial 10-year duration and renewal term.

Key Differences between Trademark Law and Practice in Cayman Islands and the BVI

- Neither the BVI nor the Cayman Islands is party to the Convention for the Protection of Industrial Property signed in Paris on 20 March 1883, as revised or amended from time to time (Paris Convention). But BVI laws allow for the filing of priority-based applications where there is an earlier application in a Paris Convention country and the BVI application is filed within six (6) months of the filing date of the priority application. The BVI also allows for priority-based applications on the basis of an earlier application in a World Trade Organisation member country within the same six-month window.

- The BVI allows for cases of trademark infringement to be brought on the basis of a trademark entitled to protection under the Paris Convention as a well-known trademark; the defensive registration of well-known trademarks is also allowed.

- Whilst both the Cayman Islands and the BVI follow the Nice Classification when examining specifications of goods and services, office actions based on specification queries are more commonly issued in the Cayman Islands where terms from WIPO’s Nice Classification database and the Harmonised List of the EUIPO TMclass database are not used (terms from these lists are automatically accepted). Class headings are also accepted in the Cayman Islands subject to certain general indications as outlined in Practice Note 02/2017 issued by the CIIPO.

- Trademarks which are not put to genuine use in the BVI within three (3) years of the date of registration are subject to revocation where there is no valid reason for non-use. There is no procedure to revoke a trademark registration in the Cayman Islands on grounds of non-use, although revocation actions may be brought on other grounds (for example, where a particular trademark no longer functions as a trade mark on its becoming common in the trade).

- Series marks registered under the repealed trademarks law in the Cayman Islands must be divided into individual trade mark registrations on or before the next renewal date. The current trademarks law does not allow for the filing of series marks. However, the BVI legislation does allow for the registration of series marks.

- Annual fees fall due every 1 January in the Cayman Islands for the life of a trademark registration. Where annual fees are unpaid by 31 March of each year, the rights protected by the registration are in abeyance until annual fees and late penalty fees are paid up to date. This means that registered rights cannot be enforced against third parties until all annual fees and late fees are paid up to date as registered rights are not considered to be in good standing. The BVI does not have an annual fees regime for trademarks.

Designs

Proprietors of UK-registered designs enjoy the same rights and privileges in the BVI as they do in the UK without any need to re-register. Designs registered in the UK automatically extend to the BVI for the life of the UK registration. Local publication of the design in the BVI is nevertheless advisable to put the public on notice of rights in and to the registered design.

Prior to 1 August 2017 there was no protection for designs in the Cayman Islands. On 1 August 2017, the Cayman Islands introduced an indirect registration process. The Design Rights Registration Act, 2016 enables proprietors of UK and EU Registered Design Rights to extend their Registered Design Rights to the Cayman Islands and renew such rights for so long as they are renewed and valid in the UK or EU respectively. There is no substantive examination, and no opposition or invalidation procedure. However, there is a requirement to pay annual fees every 1 January for the life of the registration and, where unpaid for more than 12 months, registrations are liable to cancellation by the Registrar.

Most recently, the Designs Rights Act, 2019 was passed in the Cayman Islands to allow for the direct registration of designs. Designs are defined therein as “the design of the shape or configuration (whether internal or external) of the whole or part of an article”. This legislation is not yet in practical effect.

Patents

Both the BVI and the Cayman Islands allow for the indirect registration of patents. Once a UK or EP(UK) patent is granted, an application can be made in either jurisdiction to extend the scope of protection. In the Cayman Islands, there is no deadline for the filing of the application to extend rights, whereas in the BVI, rights must be extended within three (3) years from the date of issue of the UK patent. The length of protection in each jurisdiction once rights are extended or re-registered is dependent on that of the underlying UK or EP(UK) patent. If the underlying patent expires or becomes invalidated, so does the corresponding patent in each jurisdiction.

In the Cayman Islands, an annual fee must be paid for the life of the patent in order to keep registered rights in good standing. A default in the payment of the annual fee causes registered rights to be held in abeyance until all annual fees and, including any penalties for late payment, are paid up to date. Furthermore, default in the payment of the annual fees and penalties for more than 12 months may result in registered rights being cancelled by the Registrar. In the BVI, each time an annuity or renewal fee is paid in the UK in respect of a patent that has been extended to the BVI, certified proof of same should be provided to the BVI Registry along with payment of the corresponding local renewal fee.

The Cayman Islands legislation also includes some anti-patent trolling provisions to prevent abuse by patent trolls (otherwise called Patent Assertion Entities). A patent troll is a person or entity which holds and enforces patents in an aggressive and opportunistic manner, often with no intention of marketing or promoting the subject of the patent. In other jurisdictions, particularly in the U.S.A., the activities of patent trolls have imposed considerable economic burdens on the creative pursuits of others involved in development and commercial exploitation of IP. The experience in those jurisdictions is that software patents are particularly prone to such abuse. The anti-patent trolling provisions of the Cayman Islands’ patent legislation are designed to limit persons from making assertions of patent infringement in bad faith. In addition to the general prohibition on such bad-faith assertions, the legislation includes a statutory remedy for those aggrieved by the actions of patent trolls. Furthermore, the Cayman courts will not recognise or enforce a foreign judgment to the extent the claim is based on an assertion of patent infringement made in bad faith.

Notably, the BVI also has a Patents Act (Revised 2020) that allows for the direct registration of patents. However, applications for such patents are not currently accepted by the Registry in practice and this is unlikely to change in the near future.

Copyright

An amended version of the UK’s Copyright Act of 1956 was extended to the BVI under The Copyright (Virgin Islands) Order 1962 and continues to be in effect today. Until 30 June 2016, copyright protection in the Cayman Islands was also by way of extension of the UK’s 1956 Act via the Copyright (Cayman Islands) Order 1965 (the 1965 Order). However, on 30 June 2016, Part 1 of the UK’s Copyright, Designs and Patents Act 1988, subject to certain exclusions and modifications, was extended to the Cayman Islands. This was a significant development for the Cayman Islands, and the first step in the Cayman Islands’ Government’s plans to reform and modernize intellectual property laws generally.

In keeping with the approach taken by the UK and many other countries around the world, no copyright registration procedure is in place in either jurisdiction. Instead, protection arises automatically once the work is recorded, in writing or otherwise.

Conclusion

The recent development of IP laws in the Cayman Islands and the BVI has significantly increased the ability of businesses, entrepreneurs and developers of new technology (for example, with respect to Blockchain technology) to protect, exploit and enforce their IP rights.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Legal Insight, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: ivy.wong@loebsmith.com

E: edmond.fung@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: cesare.bandini@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

E: yun.sheng@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Introduction

In certain circumstances the official liquidator of a Cayman company may be able to take action to recover assets which have been transferred in the run up to the company’s insolvency. It is important for those concerned with the affairs of a Cayman company in the twilight of insolvency to be aware of the statutory powers available to the official liquidator and the Grand Court in the Cayman Islands.

Voidable preferences

Section 145(1) of the Companies Law (2016 Revision) (the “Law”) provides that every conveyance or transfer of property, or charge thereon, and every payment obligation and judicial proceeding, made, incurred, taken or suffered by any company in favour of any creditor at a time when the company is unable to pay its debts within the meaning of section 93 with a view to giving such creditor a preference over other creditors shall be invalid if made, incurred, taken or suffered within six (6) months immediately preceding the commencement of a liquidation.

Section 93 provides that a company shall be deemed to be unable to pay its debts if:

(a) it fails to comply with a statutory demand;

(b) the company fails to satisfy a judgment debt; or

(c) it is proven to the satisfaction of the Court that the company is unable to pay its debts.

Pursuant to section 100 of the Law, the compulsory winding up of a company is deemed to commence at the time of the presentation of the petition for the winding up or, in the case of a voluntary liquidation, at the time of the resolution or expiry of the relevant period or occurrence of an event provided by the company’s Articles of Association upon which the company is to be wound up.

It is important to note that a payment to a related party of a company shall be deemed to have been made with a view to giving a creditor a preference if made within the preceding period of six (6) months. Section 145(3) provides that a creditor shall be treated as a “related party” if it has the ability to control the company or exercises significant influence over the company in making financial and operating decisions.

Dispositions at an undervalue

Section 146(2) of the Law provides that every disposition of property made at an undervalue by or on behalf of a company with intent to defraud its creditors shall be voidable at the instance of its official liquidator. The official liquidator bears the burden of establishing an intent to defraud and no action may be brought under this section after six years following the date of the relevant disposition. A number of important definitions are set out in section 146(1):

(a) “disposition” has the meaning ascribed in Part VI of the Trusts Law (As Revised);

(b) “intent to defraud” means an intention to willfully defeat an obligation owed to a creditor;

(c) “obligation” means an obligation or liability (which includes a contingent liability) which existed on or prior to the date of the relevant disposition;

(d) “transferee” means the person to whom a relevant disposition is made and shall include any successor in title; and

(e) “undervalue” in relation to a disposition of a company’s property means:

(i) the provision of no consideration for the disposition; or

(ii) a consideration for the disposition the value of which in money or monies worth is significantly less than the value of the property which is the subject of the disposition.

However, the rights of the transferee are subject to some protection. Pursuant to section 145(5) of the Law in the event that any disposition is set aside under this section and the Court is subsequently satisfied that the transferee has not acted in bad faith:

(a) the transferee shall have a first and paramount charge over the property which is the subject of the disposition, of an amount equal to the entire costs properly incurred by the transferee in the defence of the action or proceedings; and

(b) the relevant disposition shall be set aside subject to the proper fees, costs, pre-existing rights, claims and interests of the transferee (and of any predecessor transferee who has not acted in bad faith).

Fraudulent Trading

Pursuant to section 147, if in the course of a winding up of a Cayman company it appears that any business of the company has been carried on with intent to defraud creditors of the company or creditors of any other person or for any fraudulent purpose the liquidator may apply to the Court for a declaration that any persons who were knowingly parties to the carrying on of the business in such a manner are liable to make such contributions, if any, to the company’s assets as the Court thinks proper.

This Briefing Note is not intended to be a substitute for specific legal advice or a legal opinion. For more specific advice on setting aside of antecedent transactions in the Cayman Islands, please contact:

Gary Smith

Ramona Tudorancea

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Introduction

In line with the transparency and compliance efforts that made the Cayman Islands one of the early adopters of the Common Reporting Standard (CRS) and FATCA, the Cayman Islands introduced, with effect from 1st July 2017, a beneficial ownership regime (the “BO Regime”) which requires each company and limited liability company (LLC) to maintain a register of beneficial owners holding more than 25% of the interests in the company or LLC. The rules are set out in Part XVIIA (Beneficial Ownership Registers) of the Companies Law (2018 Revision) (the “Companies Law”). All companies and LLCs incorporated or registered by way of continuation in the Cayman Islands are collectively referred to herein as “Companies”.

In summary, a register is required to be created for Companies covered by the BO Regime, to be maintained at each company’s registered office in the Cayman Islands, in which beneficial ownership information is required to be kept current (the “BO Register”). Entries from the BO Register have to be periodically uploaded onto a centralized search platform (the “Beneficial Ownership Platform”) which is maintained by the Cayman Islands government authorities and accessible under certain conditions.

Determining which person(s) constitutes a “beneficial owner”

An individual is a “beneficial owner”[i] of a company or LLC if he/she holds, directly or indirectly:

(a) more than 25% of the shares in the company or interests in the LLC; or

(b) more than 25% of the voting rights in the company or LLC; or

(c) the right to appoint or remove a majority of the board of directors of the company or managers of the LLC.

If no person meets the conditions of (a), (b) or (c) above, then a person who has the absolute and unconditional legal right to exercise, or actually exercises, significant influence or control over the company or LLC (through the ownership structure or otherwise), other than solely in the capacity of a director, professional advisor or professional manager[ii], will be deemed a beneficial owner.

Which Companies are impacted by the BO regime?

Companies required to maintain a BO Register are mainly those that are not already subject to some form of direct regulatory oversight (e.g. subject to regulatory oversight in the Cayman Islands, U.S.A., China, U.K., E.U.) or indirect regulatory oversight (e.g. subject to regulatory oversight by a competent authority in an equivalent jurisdiction). In any case, limited partnerships and foreign companies will not be subject to the BO Regime.

Investment Funds and Investment Fund Managers

Effectively Companies which are structured as Cayman Islands investment funds, whether hedge funds or private equity funds, and general partners of private equity funds, real estate funds, or other investment funds, will not have to maintain a BO Register provided they fall within one of several exemptions contained in the Companies Law (e.g. the investment fund (i) is listed on a recognized stock exchange or (ii) has appointed a fund administrator that is licensed and regulated either in the Cayman Islands or in an equivalent legislation jurisdiction, or (iii) appointed an in-vestment manager that is licensed, registered and regulated either in the Cayman Islands or in an equivalent legislation jurisdiction, or (iv) appointed a sponsor that is licensed and regulated either in the Cayman Islands or in an equivalent legislation jurisdiction.

However Companies which are exempted are nonetheless required to file details outlining the ba-sis for their exemption from the requirement to file details of beneficial owners.

Obligation on each Cayman company:

-

- keep its beneficial ownership register at the company’s registered office;

- take reasonable steps to identify any individual who is a beneficial owner of the company;

- take reasonable steps to identify all relevant legal entities that exist in relation to the company.

A “relevant legal entity” is a legal entity that (a) is incorporated, formed or registered (including by way of continuation or as a foreign company) in the Cayman Islands; and (b) would be a beneficial owner of the company if it were an individual[iii].

Duty of beneficial owners and relevant legal entities to supply information

Where a “registrable person” (i.e. any beneficial owner and any relevant legal entity) knows that he or she is a beneficial owner of a Cayman company or a relevant legal entity and (i) has no reason to believe that the person’s required particulars are stated in the company’s beneficial ownership register, and (ii) the registrable person has not received a notice from the company in respect of its beneficial ownership obligations, the person shall:

(i) notify the company of the person’s status as a registrable person in relation to the company;

(ii) state the date, to the best of the person’s knowledge, on which the person acquired that status; and

(iii) give the company the required particulars.

Penalties and fines for failing to Comply

A company or LLC that knowingly and wilfully contravenes its obligations with respect to the BO Register will be liable:

(i) in the case of a first offence, to a fine of CI $25,000 (circa US $30,500); or

(ii) in the case of a second or subsequent offence, to a fine of CI $100,000 (circa US $122,000); and

(iii) Where a company is convicted of a third offence, the Cayman court may order that the company be struck off the register by the Registrar of Companies.

Directors and officers may be guilty of the same offence and liable to the same penalty if non-compliance happens with their consent or connivance, or is attributable to their wilful default.

Sanctions also apply to “registrable persons” that knowingly and wilfully fail to comply with the notice received from the company or LLC, or that knowingly and wilfully make a statement that they know to be false in a material particular, or recklessly make a statement that is false in a material particular. In this case, the sanctions are:

(i) on conviction on indictment:

(a) in the case of a first offence, to a fine of CI $25,000 (circa US $30,500); or

(b) in the case of a second or subsequent offence, to a fine of CI $50,000 (circa US $74,500) or to imprisonment for a term of two years, or to both;

(ii) on summary conviction, imprisonment for twelve months or a fine of CI$5,000 (circa US $6,100), or both.

Dealing with Non-Cooperative Shareholders

If the company or LLC does not receive the information from the registrable persons within a month of requesting them, a restrictions notice1 may be issued to the registrable persons whose particulars are missing, with a copy to the competent authority2. If the company or LLC has sent a restrictions notice3, then until it is withdrawn:

(i) any transfer or agreement to transfer the interest held by the person having received the restrictions notice, or to transfer a right to be issued with any shares, or a right to receive payment of any sums due from the company, is void (other than in a liquidation);

(ii) no rights are exercisable in respect of the interest (including the right to vote or appoint a proxy), no shares may be issued and, except in a liquidation, no payments may be made of sums due from the company, whether in respect of capital or otherwise; and

(iii) the BO Register will state ““restrictions notice issued” and the date of issue of the notice4.

Restrictions may be withdrawn by the company or LLC, if the company or LLC is satisfied with information and/or explanations received, or if the rights of a third party are being unfairly affected by the restrictions notice5. The restrictions may also be removed by the Court upon application by an interested party. Finally, a company or LLC may apply to the Court that interests subject to restrictions be sold, with the proceeds to be paid into the Court for the benefit of the beneficial owners6.

Confidentiality and Access to Information

Information regarding beneficial owners is protected under the Confidential Information Disclosure Law, 20167. The Beneficial Ownership Platform is accessible, however, by the Cayman Islands Government Minister with responsibility for Financial Services8 upon formal request by the Financial Intelligence Unit, the Financial Reporting Authority, the Cayman Islands Monetary Authority, the Tax Information Authority, or another body monitoring compliance with money laundering regulations9, or by the Financial Crime Unit of the Royal Cayman Islands Police Service in response to a request from a jurisdiction that has entered into an agreement with the Cayman Islands respecting the sharing of beneficial ownership information.

If you would like to discuss the application of the Beneficial Ownership regime to your particular Cayman Islands entity, please contact your usual Loeb Smith attorney or any of:

E: gary.smith@loebsmith.com

E: ramona.tudorancea@loebsmith.com

E: vivian.huang@loebsmith.com

E: yun.sheng@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: santiago.carvajal@loebsmith.com

[i] Section 247 of the Companies Law

[ii] Section 247(4) of the Companies Law

[iii] Section 248 of the Companies Law

1 Section 256(3) of the Companies Law

2 According to Section 246(1) of the Companies law, the competent authority is the Minister charged with responsibility for Financial Services.

3 Section 266(1) of the Companies Law

4 Section 7(2) of the Beneficial Ownership (Companies) Regulations, 2017

5 Section 273 of the Companies Law; in this case, the BO Register will state “restrictions notice withdrawn”.

6 Sections 271(1) and 272(1) of the Companies Law

7 Section 264 of the Companies Law

8 Section 260(1) of the Companies Law

9 Section 262(1) of the Companies Law

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Introduction

In line with the transparency and compliance efforts that made the Cayman Islands one of the early adopters of the Common Reporting Standard (CRS) and FATCA, and which contributed to the continued success of the Cayman Islands as one of the premier offshore financial centres, an enhanced beneficial ownership regime will be implemented starting with 1st July 20171. The new rules are set out in a new Part XVIIA (Beneficial Ownership Registers) of the Companies Law (2016 Revision) (the “Companies Law”). The same rules also apply for limited liability companies (LLCs)2. All companies and LLCs incorporated or registered by way of continuation in the Cayman Islands are collectively referred to herein as “Companies”.

In summary, an additional corporate registry will be created for Companies covered by the new regime, to be maintained at each company’s registered office in the Cayman Islands3, in which beneficial ownership information will be required to be kept current (the “BO Register”). Entries from the BO Register will have to be periodically uploaded onto a centralized search platform (the “Beneficial Ownership Platform”) which will be maintained by the Cayman Islands government authorities and accessible under certain conditions. The following is a summary of the new regime, including some useful insights for our clients and partners.

1. Which Companies will be impacted by the new regime?

Companies required to maintain a BO Register will mainly be those that are not already subject to some form of direct regulatory oversight (e.g. subject to regulatory oversight in the Cayman Islands) or indirect regulatory oversight (e.g. subject to regulatory oversight by a competent authority in a Schedule 3 country). In any case, limited partnerships and foreign companies will not be subject to the new regime.

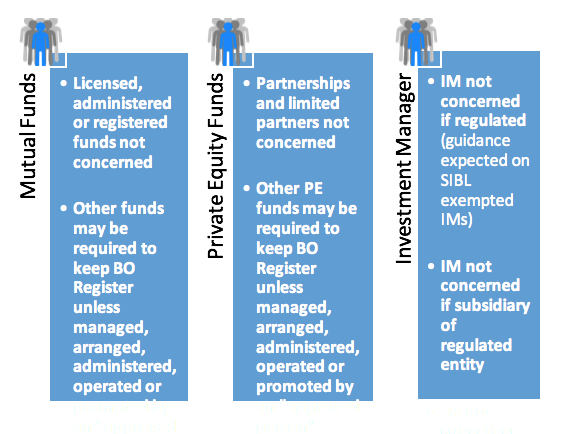

Investment Funds – Effectively Companies which are structured as Cayman Islands investment funds, whether hedge funds or private equity funds, and general partners of private equity funds, real estate funds, or other investment funds, will not have to maintain a BO Register provided they fall within one of several exemptions contained in the Companies Law.

Exemptions from the new BO Register regime – All Companies will be concerned4, except for those Companies which:

(a) are listed on the Cayman Islands Stock Exchange (CSX) or an “approved stock exchange”5;

(b) are registered or holding a licence under a “regulatory law”6 (regulatory law includes the Mutual Funds Law);

(c) are managed, arranged, administered, operated or promoted by an approved person as a special purpose vehicle, private equity fund, collective investment scheme or investment fund;

(d) are a general partner of a vehicle, fund or scheme referred to in paragraph (c) that is managed, arranged, administered, operated or promoted by an approved person; or

(e) are exempted by the Beneficial Ownership (Companies) Regulations, 2017.

In this context, “approved person” means a person or a subsidiary of a person that is regulated, registered or holding a licence in the Cayman Islands under a “regulatory law” or regulated in a jurisdiction listed in Schedule 3 of the Money Laundering Regulations (2015 Revision), or listed on the CSX or an “approved stock exchange”.

All exempted companies, ordinary non-resident companies and companies registered as special economic zone companies (SEZC) under the Special Economic Zones Law, 2011, are required to engage a corporate services provider (CSP) to assist them to establish and maintain their BO Registers7. Ordinary resident companies may either engage a CSP or the Registrar of Companies of the Cayman Islands may assist them8.

In practice, Cayman registered agents and other corporate services providers (CSPs) will be contacting and informing the Companies concerned of the new reporting obligations prior to 1st July 2017. For the investment funds industry, the Cayman Islands counsel may need to be involved in order to determine whether a fund, a general partner of a fund or an investment manager are subject to the requirement to keep a BO Register.

2. Requirement to take “Reasonable Steps” to identify Registrable Persons.

Companies required to maintain a BO Register will need to take reasonable steps to identify the individuals and the legal entities which fall under the definitions of beneficial owners and relevant legal entities.

In connection with the BO Register, Companies concerned are required to take “reasonable steps” to identify (i) any individual who is a beneficial owner of the company or LLC, and (ii) all relevant legal entities that exist in relation to the company or LLC. Together, (i) and (ii) are defined as “registrable persons”.

3. Determining which person(s) constitutes a “beneficial owner”

A person is a “beneficial owner”9 of a company or LLC if he/she holds, directly or indirectly:

(a) more than 25% of the shares in the company or interests in the LLC; or

(b) more than 25% of the voting rights in the company or LLC; or

(c) the right to appoint or remove a majority of the board of directors of the company or managers of the LLC.

If no person meets the conditions (a), (b) or (c) above, then a person who has the absolute and unconditional legal right to exercise, or actually exercises, significant influence or control over the company or LLC (through the ownership structure or otherwise), other than solely in the capacity of a director, professional advisor or professional manager10, will be deemed a beneficial owner.

A “relevant legal entity” is a legal entity that (a) is incorporated, formed or registered (including by way of continuation or as a foreign company) in the Cayman Islands; and (b) would be a beneficial owner of the company if it were an individual11. Foreign legal entities are therefore not registrable persons.

Further guidance is provided to help a company to identify its beneficial owners as follows:

Direct interest: To directly own shares, voting rights, or the right to appoint or remove any member of the board of directors, the right to exercise significant influence or control directly over the company, or to actually exercise significant influence, or the right to exercise, or to actually exercise, significant influence or control directly over the activities of a trust, partnership or other entity the trustees or members of which hold an interest in a company directly12.

Indirect interest: To have a majority stake in a legal entity which holds the shares or right directly or as part of a chain of other legal entities, with a “majority stake” defined as: (i) holding a simple majority of voting rights; or (ii) as a member, having the right to appoint or remove a simple majority of the board of directors; or (iii) as a member, controlling alone a simple majority of voting rights pursuant to a joint agreement with other shareholders or members; or (iv) having the right to exercise or exercising dominant direct influence or control13.

Joint Interest: If two or more persons each hold a share or right jointly, each of them is treated as holding that share or right. If shares or rights held by a person and shares or rights held by another person are the subject of a joint arrangement between those persons, each of them is treated as holding the combined shares or rights of both of them14.

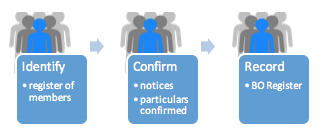

4. A Step-by-Step Process.

Concerned Companies will need, starting with 1st July 2017, to maintain a BO Register. A specific step-by-step process of how companies should (i) identify (starting with the register of members but often looking beyond it), (ii) confirm, and (iii) record beneficial owners is detailed in the Companies Law and related Regulations. Specific instructions as to what the BO Register should include are also provided.

a. At first, it is expected that concerned Companies will be working on identifying any registrable persons. During this period of time, the BO Register should state “enquiries pending”.

b. If from the outset or following investigation, the company or LLC knows or has reasonable cause to believe that there is no registrable person, then the BO Register should state “no registrable person identified”.

c. Once the potential registrable persons are identified, the concerned company or LLC is required to give them notice15 in writing, asking them, within one month of the date of receipt of the notice:

(a) to confirm whether or not they are registrable persons; and

(b) if they are registrable persons, to confirm or correct any required particulars that are included in the notice and supply any required particulars that are missing.

During this period of time, the BO Register should state “confirmations pending”.

What “particulars” are required?

The following information, once confirmed, will be required to be provided by each company and LLC to the CSP (or the Registrar, as the case may be), to be entered into the BO Register:

– for an individual16, the full legal name, residential address and, if different, an address for service of notices, date of birth, information identifying the individual from their passport, driver’s licence or other government-issued document, including identifying number, country of issue and date of issue and of expiry;

– for a corporation sole, a government or government department of a country or territory or a part of a country or territory, an international organization whose members include two or more countries or territories (or their governments), or a local authority or local government body17, name, principal office, and the legal form of the person and the law by which the person is governed; and

– for a relevant legal entity18, the corporate or firm name, the registered or principal office, the legal form of the entity and the law by which it is governed, the register of companies in which it is entered and its registration number (if applicable),

In each case, the date on which the individual or entity became or ceased to be a registrable person is also required.

If the company or LLC has not identified all potential registrable persons but knows or has reasonable cause to believe that a shareholder or another legal entity knows the identity of a registrable person19, the company or LLC may also give notice to these persons, asking them:

(a) to state whether or not they know the identity of a registrable person or any person likely to have that knowledge; and

(b) if so, within one month of receipt of the notice, to supply, at the expense of the company, any required particulars respecting such registrable persons that are within the addressee’s knowledge, and to state whether the particulars are being supplied with or without the knowledge of the person concerned.

Finally, a company is not required to give a notice if:

(a) the company knows that the individual or entity is not a registrable person; or

(b) the company has already been informed of the individual’s or entity’s status as a registrable person in relation to it, and has received all the required particulars.

d. Particulars are deemed confirmed and the notices process stops20 when the company has reasonable grounds to believe that:

(i) the particulars were supplied or confirmed by the individual or entity to whom the particulars relate; or

(ii) if another person supplied or confirmed the particulars, this was done with the knowledge of the individual or entity to whom the particulars relate; or

(iii) if the particulars were included in a statement of initial significant control delivered to the Registrar by subscribers wishing to form a company.

In general, it is accepted that a company will be entitled to rely, without further enquiry, on the response of a person to a notice in writing sent in good faith by the company, unless the company has reason to believe that the response is misleading or false21.

e. If a company or LLC becomes aware of a relevant change, with respect to a registrable person or its particulars, which would cause the company’s BO Register to be materially incorrect or incomplete, then the company is required to give notice to the registrable person requesting confirmation of the change22. If the change is confirmed, the BO Registrar will need to be updated accordingly.

It should be noted that details of a previous registrable person can only be deleted from the BO Register after the expiration of five years from the date on which the person ceases to be a registrable person23.

f. If a mistake is made, any person listed as a registrable person in relation to the company may apply to the Grand Court24 for rectification of the company’s BO Register.

5. Compliance Issues.

Concerned Companies will have a one year “grace period” commencing on 1st July 2017 during which they are required to work with the relevant Cayman registered agent in order to identify registrable persons and create the BO Register before sanctions are applicable.

Reminder: If the Companies fail to comply with its obligations without reasonable excuse or makes a statement that is false, deceptive or misleading in respect of a material particular in the BO Register, the CSP helping the company or LLC to maintain the BO Register is required to give notice to the company or LLC25, and the company or LLC is then required to provide the missing particulars, as well as a justification or correction of any statements identified as false, deceptive or misleading.

Sanctions: After 1st July 201826, a company or LLC that knowingly and wilfully contravenes its obligations with respect to the BO Register will be liable to a fine of CI$25,000 (US$30,487.80), plus CI$500 (US$609.76) for each day during which the offence continues, up to a maximum of CI$25,000 (US$30,487.80)27. Directors and officers may be guilty of the same offence and liable to the same penalty if non-compliance happens with their consent or connivance, or is attributable to their wilful default28. Sanctions also apply to registrable persons that knowingly and wilfully fail to comply with the notice received from the company or LLC, or that knowingly and wilfully make a statement that they know to be false in a material particular, or recklessly make a statement that is false in a material particular. In this case, the sanctions are imprisonment for two years or a fine of CI$10,000 (US$12,195.12), or both (or, on summary conviction, imprisonment for twelve months or a fine of CI$5,000 (US$6,097.56), or both)29.

Dealing with Non-Cooperative Shareholders: If the company or LLC does not receive the information from the registrable persons within a month of requesting them, a restrictions notice30 may be issued to the registrable persons whose particulars are missing, with a copy to the competent authority31. If the company or LLC has sent a restrictions notice32, then until it is withdrawn:

(i) any transfer or agreement to transfer the interest held by the person having received the restrictions notice, or to transfer a right to be issued with any shares, or a right to receive payment of any sums due from the company, is void (other than in a liquidation);

(ii) no rights are exercisable in respect of the interest (including the right to vote or appoint a proxy), no shares may be issued and, except in a liquidation, no payments may be made of sums due from the company, whether in respect of capital or otherwise; and

(iii) the BO Register will state “restrictions notice issued” and the date of issue of the notice33.

Restrictions may be withdrawn by the company or LLC, if the company or LLC is satisfied with information and/or explanations received, or if the rights of a third party are being unfairly affected by the restrictions notice34. The restrictions may also be removed by the Court upon application by an interested party. Finally, a company or LLC may apply to the Court that interests subject to restrictions be sold, with the proceeds to be paid into the Court for the benefit of the beneficial owners35.

6. Confidentiality and Access to Information.

Information regarding beneficial owners is protected under the Confidential Information Disclosure Law, 201636. The Beneficial Ownership Platform will be accessible, however, by the Cayman Islands Government Minister with responsibility for Financial Services37 upon formal request by the Financial Intelligence Unit, the Financial Reporting Authority, the Cayman Islands Monetary Authority, the Tax Information Authority, or another body monitoring compliance with money laundering regulations38, or by the Financial Crime Unit of the Royal Cayman Islands Police Service in response to a request from a jurisdiction that has entered into an agreement with the Cayman Islands respecting the sharing of beneficial ownership information. Currently, only the UK is deemed to be such a jurisdiction.

This is not intended to be a substitute for specific legal advice or a legal opinion.

1. The Beneficial Ownership (Companies) Regulations, 2017, the Companies (Amendment) Law, 2017, the Companies Management (Amendment) Law, 2017, Limited Liability Companies (Amendment) Law, 2017, Beneficial Ownership (Limited Liability Companies) Regulations, 2017, are scheduled to become effective on 1st July 2017.

2. Limited Liability Companies (Amendment) Law, 2017, Beneficial Ownership (Limited Liability Companies) Regulations, 2017, the provisions of which are fairly similar.

3. Section 252(1) of the Companies Law

4. Section 245 of the Companies Law

5. As listed in Schedule 4 of the Companies Law

6.Section 2 of the Monetary Authority Law (2016 Revision), which refers to (i) Banks and Trust Companies Law (2013 Revision); (ii) Building Societies Law (2014 Revision); (iii) Companies Management Law (2003 Revision); (iv) Cooperative Societies Law (2001 Revision); (v) Insurance Law, 2010; (vi) Money Services Law (2010 Revision); (vii) Mutual Funds Law (2015 Revision); and (viii) Securities Investment Business Law (2015 Revision).

7. Section 252(2) of the Companies Law

8. Section 252(3) of the Companies Law

9. Section 247 of the Companies Law

10. Section 247(4) of the Companies Law

11. Section 248 of the Companies Law

12. Section 11 of the Beneficial Ownership (Companies) Regulations, 2017

13. Sections 12-13 of the Beneficial Ownership (Companies) Regulations, 2017

14. Section 15 of the Beneficial Ownership (Companies) Regulations, 2017

15. Section 249(1) of the Companies Law

16. Section 254(1) of the Companies Law

17. According to Section 244(2) of the Companies Law, such entities should be treated as an individual for the purposes of determining if they are a beneficial owner.

18. Section 254(3) of the Companies Law

19. Section 249(3) of the Companies Law

20. Section 254(4) of the Companies Law

21. Sections 247(2) and 248(2) of the Companies Law

22. Section 255(1) of the Companies Law

23. Section 258 of the Companies Law

24. Section 259 of the Companies Law

25. Section 256(1) of the Companies Law

26. Section 5 of the Companies (Amendment) Law, 2017

27. Section 274 of the Companies Law

28. Section 278 of the Companies Law

29. Sections 275 and 276 of the Companies Law

30. Section 256(3) of the Companies Law

31. According to Section 246(1) of the Companies law, the competent authority is the Minister charged with responsibility for Financial Services.

32. Section 266(1) of the Companies Law

33. Section 7(2) of the Beneficial Ownership (Companies) Regulations, 2017

34. Section 273 of the Companies Law; in this case, the BO Register will state “restrictions notice withdrawn”.

35. Sections 271(1) and 272(1) of the Companies Law

36. Section 264 of the Companies Law

37. Section 260(1) of the Companies Law

38. Section 262(1) of the Companies Law

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.