The Cayman Islands’ Mutual Funds (Amendment) Act, 2026 and the Cayman Islands’ Private Funds (Amendment) Act, 2026 both came into force as of March 24, 2026. The Mutual Funds (Amendment) Act, 2026 established a comprehensive regulatory framework for “tokenised mutual funds”, defining them as funds with equity interests represented by digital equity tokens. It mandates enhanced record-keeping, operator approval for transfers, and specific risk disclosures. The Private Funds (Amendment) Act, 2026 amends the Private Funds Act to define “digital investment tokens”, and mandates strict record-keeping, operator-approved transfers, and risk disclosures for funds where interests are represented by digital tokens.

The key takeaway from the changes introduced is that tokenised funds are to be regulated within the existing Cayman Islands Monetary Authority (CIMA) funds regulatory framework, rather than as separate virtual asset entities.

What are the key changes introduced by both Acts?

- Additional definitions – The definition of “debt” and “equity interests” have been expanded to include LLC interests. New definitions have been included respectively for “digital equity token” in respect of a tokenised mutual fund and “digital investment token” in respect of a tokenised private fund. In each respective case, meaning for “digital equity token” – a digital representation of the whole of an equity interest held by an investor, and meaning for “digital investment token” – a digital representation of the whole of an investment interest held by an investor. A new definition has also been included for “tokenised mutual fund” and “tokenised private fund”, being respectively a fund that has any of its equity interests/ investment interests represented by digital equity tokens/ digital investment tokens.

- No custodian required – There is no requirement for a custodian to be appointed to hold the digital equity tokens or digital investment tokens in secure custody. However, disclosure as to who holds the underlying assets of the fund is material information for the fund’s offering document (particularly where such assets are not held by an independent custodian which is subject to regulatory standards for maintaining custody).

- No requirement for a CIMA licensed Administrator/ principal office – There is no requirement for a tokenised fund to have a CIMA licensed administrator who also acts as the principal office. However, where a tokenised mutual fund does appoint a CIMA licensed administrator, they will need to comply with additional obligations. For example, a CIMA licensed administrator must be satisfied that all records relating to the ownership of tokens are securely maintained by the tokenised fund and readily available and that the tokenised fund has complied with the applicable statute.

- Maintenance of records – If a Cayman Islands licensed mutual fund administrator is appointed, it must ensure secure maintenance of records related to token issuance, creation, sale, transfer, and ownership.

- Transfer Restrictions – Tokens are only transferable with the approval of the operator of the tokenised fund and in accordance with the terms of the offering document.

- Risk Disclosures – Offering documents for tokenized funds must explicitly disclose risks related to digital tokens including cybersecurity risks, custody risks, and transferability risks, together with how such risks are addressed or mitigated for investors.

- Annual confirmation – An annual confirmation will be required by CIMA from the operators of the tokenised fund that all records relating to the issuance, creation, sale, transfer and ownership of an equity interest/. investment interest that is represented by a digital equity token/ digital investment token have been properly kept and maintained in compliance with the requirements set out in the legislation.

- CIMA supervisory powers – CIMA is granted supervisory powers over tokenised funds to ensure compliance with statute and the protection of investors interests, including inspections of the underlying technology and token transactions.

The Virtual Asset (Service Providers) (Amendment) Act, 2026 which is also now in force clarifies that tokenised funds registered with CIMA are not subject to the VASP Act unless they engage in separate virtual asset services.

These changes clearly demonstrate that the Cayman Islands remains committed to fostering innovation, helping the jurisdiction stay at the leading edge, where traditional fund structures meet blockchain technology.

This publication is not intended to be a substitute for specific legal advice or a legal opinion. For specific legal advice on the subject matter of this Briefing, please contact your usual Loeb Smith attorney or Liz Kenny.

Partner: Elizabeth Kenny

E: elizabeth.kenny@loebsmith.com

Liz is a Partner in the Corporate and Funds Group and is also Head of Regulatory and Risk in which capacity she is key thought leader on regulatory licence applications, virtual assets, crypto and fintech regulation, corporate governance reviews, anti-money laundering compliance frameworks, regulatory audits, Corporate Governance, CIMA inspections and remediations, sanction reporting and licencing, data protection laws, regulatory enforcement notices, administrative fines and on mandatory information exchange requirements.

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

1. Overview

The laws relating to trusts and equity in the Cayman Islands and in the British Virgin Islands are derived directly from English law but have been modified in each jurisdiction by legislation to reflect their respective position as a premier offshore financial centre.

A trust is a legally binding arrangement whereby a person (“Settlor”) transfers assets to another person (“Trustee”) who is entrusted by the Settlor with legal title to the trust assets, not for the Trustee’s own benefit, but for the benefit of other persons (known as “Beneficiaries”, who may include the Settlor) or for a specified purpose. In addition to being a Beneficiary, the Settlor may, in certain circumstances, also act as a co-Trustee. The Settlor may, also, retain a degree of control over the trust, such as the power to approve distributions, the power to appoint and remove Trustees and the power to revoke the trust.

The Settlor will set out detailed instructions to the Trustee as to the disposition of trust assets in a document called the Declaration of Trust or the Trust Deed. This document will inform the Settlor, the Trustee and the Beneficiaries as to their respective rights, entitlements and duties.

2. Setting up a Trust – Who will be the Trustee?

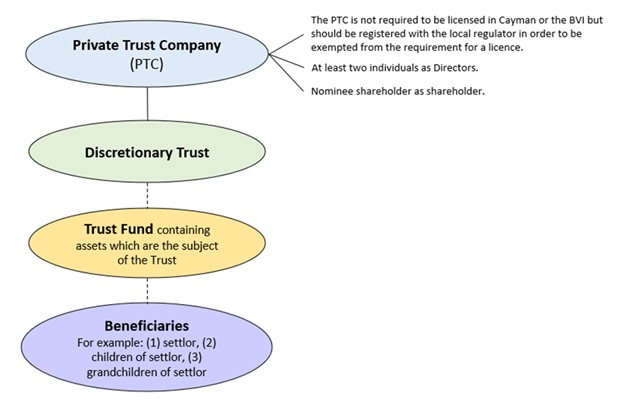

The Trustees or Trustee of a Cayman Islands Trust or a BVI Trust (i) may be individuals, or (ii) may be a company licenced as a trust company in the Cayman Islands for Cayman Trusts or in the BVI for BVI Trusts (except in each case, for a Private Trust Company (“PTC”) which does not have to be licensed). An individual Trustee does not have to be a Cayman resident or a BVI resident to be a trustee of a Cayman Trust or a BVI Trust.

Corporate Trustees

Generally, the Trustee of a Cayman Trust is a trust company based in Cayman or the Trustee of a BVI Trust is a trust company based in the BVI. This can be either (i) a licensed Trust Company which carry on business as a professional trustee, or (ii) a PTC.

Generally, a PTC acts as Trustee of a single trust or a group of related trusts and does not charge fees. For example, instead of using the services of a professional Corporate Trustee in Cayman or in the BVI, the Settlor could establish a PTC in Cayman or in the BVI (as applicable) to act as Trustee of the trust mentioned below. The Settlor or his trusted advisors can serve on the board of directors of the PTC, which allows the Settlor more flexibility, control and continuity in the administration of the trust’s assets. PTCs can also be a more cost-effective solution in certain instances. A PTC in either Cayman or in the BVI is exempt from the regulation and licensing requirements in Cayman or in the BVI (as applicable), subject to certain requirements.

3. Type of Offshore Trusts

There are various types of trusts in each of the Cayman Islands and the BVI. The most appropriate trust structure for the settlement of trust assets will depend on the Settlor’s particular circumstances and the Settlor’s objectives. The most common types of offshore Trusts are (1) Discretionary Trusts, (2) Fixed Interest Trusts, (3) Accumulation and Maintenance Trusts, (4) Revocable Trusts, (5) VISTA trusts for the BVI, (6) STAR Trusts for the Cayman Islands, and (7) Non-Charitable Purpose Trusts.

Discretionary Trust

The discretionary trust provides a flexible and efficient structure under which the Settlor transfers ownership of the assets to the Trustee(s), subject to any reserved powers or Protector provisions. The settlement deed generally gives the Trustee(s) wide discretionary powers over the trust fund and its application for the benefit of the Beneficiaries. The Beneficiaries of a discretionary trust have no definite right to the assets of the trust.

Fixed Interest Trust

A fixed interest trust specifies the rights of Beneficiaries in relation to the capital and/or income of the trust fund. For example, the settlement deed may specify that a Beneficiary is entitled to the income (and not the capital) of the trust fund during his/her lifetime. A trust can also be structured as a combination of a discretionary and a fixed interest trust.

Accumulation and Maintenance Trust

An Accumulation and Maintenance Trust (“A&M Trust”) is a type of discretionary trust where one or more Beneficiaries will become legally entitled to the income, or both capital and income, of the trust on attaining a specified age. A&M Trusts are generally used to benefit children or grandchildren of the Settlor. The Beneficiaries do not have a fixed entitlement to the benefits or interests accruing to the trust for a certain period, during which time income is accumulated and as it grows is added to the capital assets of the trust. The persons who are ultimately entitled to the trust assets may benefit from the accumulation of capital in the trust. The trust deed may give the Trustee a discretionary power to make distributions amongst the Beneficiaries up to a specific age for their education, maintenance and wellbeing and to provide thereafter for a designated share of the trust fund to be distributed to each child on attaining a specified age.

VISTA Trust

The VISTA trust is unique to the BVI. The main features of a VISTA trust are: (a) it may only hold shares of an underlying BVI company, although the company is not restricted in what it may invest in; (b) the Trustee is not under a duty to diversify or monitor the trust fund and investments, which is a basic principle of the more standard trusts; (c) at least one of the Trustees must be a ‘designated Trustee’ as defined in the VISTA Act (for example a PTC or a BVI licensed trust company); and (d) the Trustee cannot act as a director of the underlying company.

STAR Trust

The STAR Trust is unique to the Cayman Islands. The Special Trusts (Alternative Regime) Act, 1997 is now incorporated into Part VIII of the Trusts Act (As Revised) (“Trust Act”. The key features of the STAR Trust are that:

- Beneficiaries and/or objects may be persons, purposes or both. There may be any number of Beneficiaries and any number of purposes, whether charitable or not, provided that such purposes/objects are lawful and not contrary to public policy in Cayman.

- Any uncertainty as to the objects or mode of execution or administration of a STAR trust can be resolved by the Trustee (or any other person the STAR trust document so specifies) or by the Cayman court, if necessary. A STAR trust is therefore very unlikely to be declared void from the outset on grounds of uncertainty, as could be the case with a poorly drafted non-STAR trusts.

- The Trustee of a STAR trust must be or must include a trust company licensed to conduct trust business in the Cayman Islands. This adds a level of oversight and regulation above and beyond other jurisdictions. There are criminal sanctions attached if these requirements are overlooked or bypassed.

- STAR trusts must have an “Enforcer” who is the only individual person or corporate entity with legal standing to enforce the terms of the STAR trust (such enforcement powers having been removed from the Beneficiaries by virtue of the Trust Act). The Trust Act therefore makes a clear distinction between the capacity to benefit from a STAR trust and the actual capacity to enforce such a trust. The effect is to remove rights of Beneficiaries not only to enforce the trust, but also their right to seek disclosure of information regarding the STAR trust and its ongoing administration.

- The rule against perpetuities does not apply to STAR trusts, which may be created for an unlimited duration (or not, depending on the terms of the trust deed), which eliminates the risk of a resulting trust in favour of the Settlor at the end of the perpetuity period and the adverse tax consequences which may flow from such an event.

- A STAR trust cannot hold land in the Cayman Islands but may hold an interest in a company, partnership or other entity which does.

Non-Charitable Purpose Trust

A Cayman Trust or a BVI Trust can be established partly or wholly for non-charitable purposes. The purpose must be specific, reasonable and possible, and may not be immoral, contrary to public policy or unlawful. An enforcer must be appointed who shall have the duty to ensure the Trustee fulfils the non-charitable purposes of the trust. At least one Trustee must be a “designated person” (for example a PTC or a licensed trust company). A purpose trust may exist in perpetuity or be terminated at a specified date.

4. Key Advantages of Offshore trusts

Tax Planning: Offshore trusts are very popular because they are established in jurisdictions such as the Cayman Islands or the British Virgin Islands where the trustees are resident and are subject to zero tax and this brings with it a number of tax planning advantages, even though the tax position of the Settlor and/or the Beneficiaries has to be considered.

Confidentiality: Trustees of offshore trusts have a duty under common law to keep the affairs of the trust confidential. Whilst this duty is not absolute, the courts of the Cayman Islands and the BVI have an inherent supervisory jurisdiction over the administration of trusts and are generally unwilling to sanction the disclosure of information except in cases to avoid potential injustice or harm.

Asset Protection: Global operations may expose the Settlor’s business to different legal and financial challenges. Offshore trusts can protect the Settlor’s finances from lawsuits, bankruptcy actions and political instability in onshore jurisdictions and secure the business’s continuity in these circumstances.

Succession Planning: Changing leadership and ownership within a family business can bring unique complexities. Offshore trusts offer a clear and efficient framework for succession planning where distributions and management roles for future generations can be clearly set out and help prevent potential conflicts among family members and build transparency.

Flexibility and Control: Offshore trusts provide flexibility in that they can be customized to align with the Settlor’s specific goals (e.g. asset protection, philanthropy, or wealth distribution over multiple generations). The Settlor can also retain varying degrees of control over the trust, ensuring his/her vision remains in focus.

Freedom from Onshore rules and regulation: Establishing an offshore trust avoids specific rules relating to trusts onshore which may add additional regulatory and/or compliance burdens.

5. Common uses for Cayman Trusts and BVI Trusts

-

- As an instrument for succession planning in the event of death or incapacity.

- To mitigate against tax liabilities.

- To protect assets (e.g. from exchange controls or other government interference)

- As a confidential way of holding assets.

- To protect beneficiaries who have difficulty in managing their own affairs.

- To circumvent forced heirship rules.

- To hold shares in a family company or in corporate transactions.

- As a vehicle for philanthropic giving.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Briefing, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E. elizabeth.kenny@loebsmith.com

E. vanisha.harjani@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

E: yun.sheng@loebsmith.com

A Private Trust Company (PTC) is an entity that is established with the sole purpose of acting as a corporate trustee to a trust or a number of trusts, provided those trusts are “connected”. The term “Connected trust business” means trust business where the settlors of funds to the trusts are all “connected persons” in relation to each other. PTCs afford high net worth individuals a greater control over their assets and have become extremely attractive for families seeking to manage their wealth effectively.

The regulatory basis for the operation of trust companies in the Cayman Islands is found in the Banks and Trust Companies Act (2021 Revision) as amended (BTCA) and the Private Trust Companies Regulations (2020 Revision) as amended (PTCR). These regulations provide for the establishment of the two types of PTCs recognized in the Cayman Islands which are (i) the Licenced PTCs and (ii) the Registered PTCs.

Licenced PTC – requirements

A Licenced PTC has to obtain a valid licence from the Cayman Islands Monetary Authority (CIMA) before conducting any trust business within or outside the Cayman Islands. This requirement is subject to exemptions guaranteed under the PTCR which provide an avenue for PTCs to operate without a licence as long as they are registered with CIMA and fulfill the following conditions:

-

- They are incorporated in the Cayman Islands; and

- They conduct no trust business other than connected trust business.

The licence granted by CIMA for a Licenced PTC is known as a Restricted Trust Licence and it authorizes the holder to undertake trust business only for persons listed in any undertaking which accompanies the application for the licence. CIMA will only grant a license to a PTC if it has:

-

- a place of business in the Cayman Islands approved by CIMA which will be its principal office in the Cayman Islands; and

- two individuals or a body corporate, approved by CIMA, resident or incorporated in the Cayman Islands to be its agent in the Cayman Islands.

Licenced PTC – key features

Some of the key features of a Licenced PTC include:

-

- The minimum net worth of the PTC should be twenty thousand dollars (CI$20,000) which is approximately US$24,400.

- If incorporated under the Cayman Islands’ Companies Act (Companies Act) the PTC is under an obligation to have its accounts audited annually by an auditor approved by CIMA. The audited accounts are required to be forwarded to CIMA within three (3) months of the end of the financial year of the PTC unless an extension has been sought.

- The PTC must have a minimum of two individual directors at any given time, one of whom must have extensive knowledge and experience in trust business. CIMA usually does not approve corporate directors to sit on boards of Licenced entities.

- The disclosure of beneficial ownership and control is required on application of a licence.

Registered PTC – requirements

The Registered PTC is founded under the provisions of the PTCR. The main requirements for this type of PTC include:

-

- It must maintain a registered office at the office of a company that holds an unrestricted Trust licence provided for under the BTCA;

- It must allow CIMA, at any given time, to inspect all its documents and records or that should be held at the registered office;

- It must keep at its registered office and make available for inspection at its registered office, in relation to each relevant trust, adequate, accurate and up to date copies of the trust deed or other documents containing or recording the terms of the trust, names and addresses of the settlor, protector, enforcer, contributor to the trust, any beneficiary to whom a distribution is made from the trust, any deed or other document varying the terms of the trust and all financial transactional records of the PTC and its connected trust business;

- It must file an annual declaration with CIMA every year declaring the name of the PTC, the name and addresses of the directors, shareholders (if any), the name of the holder of the Trust licence providing the registered office of the PTC, that the Company is a PTC which does not require a licence to carry on connected trust business and that the PTC is in compliance with the requirements of the PTCR;

- It must file with CIMA, the identification of the directors and shareholders of the PTC;

- The PTCR prescribes that a natural person must be appointed as a director for the PTC;

- The PTC must include the word “Private Trust Company” or the letters “PTC” in the name by which the company is registered under the Companies Act;

- It must not solicit or receive contributions in respect of trusts of which it is trustee from the public or persons other than those who are, in relation to each other, connected persons.

Registered PTC vs. Licenced PTC

-

- Fees

The initial registration fee for a Registered PTC is US$4,268.29 (CI$3500) and thereafter an annual registration fee of the same amount is applied to be paid before the 31st day of January every year. The application fee for a Licenced PTC is US$2,439.02 (CI$2000) and the fee paid on the grant of a licence and subsequently every year is US$8,536.59 (CI$7,000). - Net worth Requirements

The regulations do not prescribe a minimum net worth requirement for the Registered PTC. The Licenced PTC, on the other hand, is required to have a minimum net worth of US$25,000 (CI$20,000). - Audit

There is no requirement for the Registered PTC to file audited accounts with CIMA. The Licenced PTC is under an obligation to file its audited accounts annually with CIMA by an auditor approved by the Authority. - Directors

A Registered PTC is required to have a natural person appointed as director, but the PTCR is silent on the minimum number of directors. CIMA however recommends a minimum of two individual directors. It is a mandatory requirement for a Licenced PTC to have at least two natural persons appointed as directors on the Board of the PTC. There is no requirement for the directors to be approved by CIMA - Timing

A Registered PTC can be up and running within three to four business days from the day the application for registration has been submitted to CIMA. The turnaround for processing an application for a Licenced PTC is six to eight weeks from the date the application was submitted to CIMA.The Registered PTCs have gained more popularity in the Cayman Islands as CIMA has noted a steady increase in the number of PTCs seeking to be registered over the past eight (8) years based on the table below which has been published on the CIMA website.

- Fees

Trust (Fiduciary) Licensees & Registration Statistics

Shareholders of a PTC

The shares of a PTC are commonly held by one or more individuals, or by a company limited by guarantee or in a STAR Trust. It is advisable to use a corporate entity as opposed to an individual because in the event of death, the devolution of shares may take a long time owing to the probate process.

Benefits of using PTCS

Registered PTCs are regularly used by high net worth families in their wealth structuring for a number of reasons:

-

- they protect confidentiality and are lightly regulated when compared to using a large and highly regulated international financial institutions as trustee;

- they provide a comprehensive framework under which family members and advisors can be involved in decision making (by being on the board of Directors of the PTC) which gives room for flexibility as families can tailor the PTC based on their personal needs and objectives;

- they can avoid the complications of succession when used in conjunction with a STAR Trust (i.e. a STAR Trust can be used to hold all the shares of the PTC).

- the speed at which a PTC can be established (i.e. 3-4 days), and the relatively low cost of operation have made PTCs extremely attractive to HNW families and their advisors.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the formation of a Cayman Islands Private Trust Companies, establishing family offices or protecting private wealth generally, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E. elizabeth.kenny@loebsmith.com

E: vanisha.harjani@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

E: yun.sheng@loebsmith.com

Cayman Islands exempted companies (“Cayman Companies” and each a “Cayman Company”) are widely utilized in structuring cross-border finance transactions. One of the key reasons for this is that the Cayman Islands provides a flexible and well-tested regime for secured financing transactions that is attractive to borrowers and lenders alike. The process for creating security in the Cayman Islands is also straightforward and will not typically impact the timeframe of a proposed transaction.

In this Briefing, we address certain of the key Cayman Islands law points pertaining to the creation and protection of security by a Cayman Company over its assets. For details with respect to the creation of security over Cayman Islands shares, please refer to our separate guide entitled “Granting and protecting security over shares in a Cayman Islands exempted company”.

This Briefing does not consider the additional steps that may be necessary for the purposes of creating and protecting security over specific asset classes, such as Cayman Islands registered aircraft and ships, or land located in the Cayman Islands.

1. Creation of security

The Companies Act (as Revised) of the Cayman Islands (the “Companies Act”) does not contain any provisions with respect to the creation of security over the assets of a Cayman Company. Therefore, the security should adhere to the following common law principles:

i. it must be in writing;

ii. the security document must signed by, or with the authority of, the Cayman Company; and

iii. the security document must clearly indicate the intention to create security over the relevant assets and the amount secured or how that amount is to be calculated.

Cayman Islands law recognizes various forms of security over assets, including legal mortgages, equitable mortgages, charges and assignments by way of security. The type of security interest that is created will depend on the type of asset to be secured.

2. Execution formalities and regulatory approvals

Cayman Islands law does not prescribe a particular mode of execution with respect to security over the assets of a Cayman Company and it is not necessary for such security to be certified, notarized or apostilled to make the security valid or enforceable from a Cayman Islands law perspective.

It is important to review the Memorandum and Articles of the relevant Cayman Company to ensure compliance with any applicable signing formalities. No regulatory approvals are necessary to create valid and enforceable security as a matter of Cayman Islands law in respect of security that is created over a Cayman Company’s assets.

3. Stamp duty and taxes

No stamp duty or taxes are payable with respect to the creation of security over the assets of a Cayman Company or upon any transfer thereof in an enforcement as a matter of Cayman Islands law so long as:

i. the security document and any ancillary documents thereunder are not executed or delivered in, brought into, or produced before a court of, the Cayman Islands; and/or

ii. the assets do not comprise land in the Cayman Islands, or shares in a subsidiary that has an interest in land in the Cayman Islands.

4. Governing law

Cayman Islands law permits security over the assets of a Cayman Company to be governed by Cayman Islands law or foreign law.

In cross-border finance transactions, it is relatively common for the governing law of a security document over the assets of a Cayman Company to be aligned with the governing law of the principal finance documents or the lex situs of the secured asset. One advantage of adopting a foreign governing law clause in a security document is that it may make available certain additional remedies (such as appropriation) which are not available under Cayman Islands law. Care should however be taken to ensure that there are no conflicts of law issues where a security document is governed by foreign law. English law, New York law, Hong Kong law, and Singapore law are frequently adopted to govern security over the assets of a Cayman Company and no major conflicts of law issues are likely to arise.

Where the security document is governed by foreign law, the:

i. security document should comply with the requirements of its governing law to be valid and binding on the Cayman Company; and

ii. remedies available to a secured party are governed by the governing law and the terms of the security document.

5. Security deliverables

The Cayman Company will typically be required to deliver the following documents to the secured party under the terms of the relevant security document and/or the other finance documents:

i. a certified copy of its register of mortgages and charges showing the security created over the secured assets (see further below); and

ii. a copy of the board resolutions of its board of directors authorizing:

a. its entry into and execution of the security document; and

b. the updates to be made to its register of mortgages and charges.

6. Register of Mortgages and Charges

Pursuant to the Companies Act, a Cayman Company must record particulars of the security created over any of its assets in its register of mortgages and charges. The register of mortgages and charges must include:

i. a short description of the property mortgaged or charged;

ii. the amount of charge created; and

iii. the names of the mortgagees or persons entitled to such charge.

There is no statutory timeframe within which the register needs to be updated. However, a well-advised secured party will request that the register is updated promptly so that third parties that inspect it are on notice of the security. Any variations and releases of charge should also be reflected in the register of mortgages and charges.

A copy of the register of mortgages and charges (including a blank register if no prior security has been granted) must be kept at the registered office of the Cayman Company and is a private record that is not open to inspection by the public. However, any creditor or member of the Cayman Company may inspect the register at all reasonable times.

If a Cayman Company does not comply with the aforementioned provisions, every director or officer who authorizes or knowingly and willfully permits such non-compliance is liable to a penalty. This does not invalidate the validity, enforceability or the admissibility in evidence of the charge, however.

As there is no statutory regime for registering security interests under Cayman Islands law, the common law rules of priority continue to apply. In general terms, these rules specify that priority between competing security interests is determined by the dates on which the relevant security interests were created. It is important to note that inserting details of mortgages and charges in the register of mortgages and charges of a Cayman Company does not confer priority on a charge in respect of the relevant secured asset.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Briefing, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

E: yun.sheng@loebsmith.com

Irrevocable trusts are a crucial instrument in estate planning, particularly in jurisdictions like the Cayman Islands, known for its robust legal framework and favourable tax environment. An irrevocable trust in the Cayman Islands is a legal arrangement where assets are transferred by a grantor or settlor to a trustee, who manages them for the benefit of designated beneficiaries, and the trust cannot be revoked or terminated by the grantor or settlor. This structure is often chosen for its asset protection features and privacy benefits, particularly for individuals seeking to safeguard their wealth from future creditors or legal claim.

In the Cayman Islands, the legal system supports the establishment of irrevocable trusts, specifically designed to cater to international clientele seeking to secure their assets against potential creditors, divorce proceedings, or other financial claims. Once assets are transferred into an irrevocable trust, the grantor or settlor relinquishes control, thereby ensuring that the trust’s assets are legally separated from the grantor’s estate. This permanent separation between the trust assets and the grantor’s estate has specific legal and tax implications.

Cayman Islands irrevocable trusts also enjoy confidentiality, as trust documents are not publicly recorded. This privacy is particularly appealing to high-net-worth individuals and families. Additionally, the jurisdiction’s lack of capital gains tax, estate tax, and inheritance tax further enhances the appeal of irrevocable trusts for wealth preservation and succession planning.

Key Features of Irrevocable Trusts

In the Cayman Islands, irrevocable trusts have several distinct legal characteristics that differentiate them from other types of trusts, particularly revocable trusts. These key features including the following.

- Irrevocability: As the name suggests, irrevocable trusts cannot be revoked, or terminated by the grantor or settlor once they are established.

- Asset Protection: Since the grantor or settlor retains no control over the assets once placed in an irrevocable trust, those assets are generally protected from creditors and legal claims against the settlor. This feature is particularly valuable for estate planning and asset protection strategies.

- Beneficiary Rights: In an irrevocable trust, the rights of the beneficiaries are generally defined clearly from the outset. Beneficiaries may have enforceable rights to the income or capital of the trust, which cannot be altered by the grantor/settlor. This contrasts with revocable trusts, where beneficiaries’ rights can change if the grantor/settlor modifies the trust.

- Settlor’s Control: The grantor/settlor of an irrevocable trust typically relinquishes control over the trust assets and the trust’s management. This differs from a revocable trust, where the grantor/settlor can retain control and amend terms as needed throughout their lifetime.

- Tax Implications: Whilst there are no taxes on income, capital, profits or gains in the Cayman Islands, irrevocable trusts may have benefits regarding estate taxes in the jurisdiction where the grantor/settlor is domiciled since the assets are no longer considered part of the grantor/settlor’s estate.

- Trustee Powers: The powers of the trustee in an irrevocable trust are often more clearly defined, as the settlor cannot subsequently direct or change these powers. The trustee has a fiduciary duty to act in the best interests of the beneficiaries, managing and distributing trust assets according to the terms set out in the trust deed at the establishment of the trust.

- Duration and Administration: Irrevocable trusts may be subject to specific rules regarding their duration and administration. Depending on the terms set by the settlor/grantor and applicable laws, these trusts may continue for a long period or until specific conditions are met.

Conclusion

Understanding these characteristics is crucial for individuals considering establishing a trust in the Cayman Islands, as they can significantly impact estate planning, asset management, and the protection of assets.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Briefing, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: faye.huang@loebsmith.com

E: vivian.huang@loebsmith.com

E: yun.sheng@loebsmith.com

The rapid advancement of artificial intelligence (AI) continues to raise complex questions about the applicability of intellectual property (IP) laws to AI and AI-generated works.

IP remains one of the leading and most contentious issues in respect of AI governance. AI adoption continues to grow, and this year is already showcasing a wider range of commercial applications across all sectors. In light of the IP related challenges, businesses leveraging AI technologies must strategize to navigate the evolving intellectual property landscape. As the legal framework around AI continues to develop, businesses need to ensure that they avoid copyright infringement while also effectively safeguarding their own IP assets. Developing a clear understanding of how existing laws apply to AI technology and staying updated on legal developments will be crucial for companies seeking to innovate responsibly and protect their intellectual property in an AI-driven economy.

How is Intellectual Property protected in the Cayman Islands and the BVI?

Copyright protection in the BVI (for “qualified persons”) and in the Cayman Islands (for “qualifying persons”) is automatic when such person creates an original work (once the work is recorded, in writing or otherwise) such as sound and music recordings; films; when you write a book or poem; or when you develop new software. By virtue of the Copyright (Cayman Islands) Order 2015 and Order 2016 (as amended), Part 1 of the U.K.’s Copyright, Designs and Patents Act 1988, subject to certain exclusions and modifications, was extended to the Cayman Islands. The BVI has implemented its own legislation in the form of the Copyright Act (Revised 2020) which is very similar.

Patent protection in the two jurisdictions is quite similar. As it is in other jurisdictions, in order to get patent protection, the invention must be: (i) new – i.e. the first in the world, (ii) useful – i.e. the invention must serve a purpose or provide a solution, and (iii) inventive – i.e. the invention must not be obvious to persons in the industry in which the invention is intended to be used.

Both the BVI and the Cayman Islands allow for the indirect registration of patents. Once a U.K. patent is granted, an application can be made in either of the Cayman Islands or the BVI to extend the scope of protection. In the Cayman Islands, there is no deadline for the filing of the application to extend rights, whereas in the BVI, rights must be extended within three years from the date of issue of the UK patent.

AI-generated works, AI-inventions and other AI-outputs and infringement

IP laws are designed to protect human creations. Generative AI (AI which generates text, images, speech, video or technical inventions based on user-inputted instructions) continues to increase in capability and grow in adoption. However, most copyright and patent laws, for example, do not yet explicitly address AI’s role in authorship or inventorship, leaving a legal void requiring attention. Traditionally, the author or inventor is the person or organisation that creates the works. If now AI is responsible for content creation autonomously without any human input, the question is who owns the copyright protecting such content.

- For countries, such as the UK, this may be answered by the fact that computer-generated works will be owned by the person who made the necessary arrangements for the creation of the work.

- An overwhelming view in the E.U. is that AI cannot be a legitimate author. However, specific ways of using AI may result in a work that is protected for the user.

How does Artificial Intelligence affect Intellectual Property Protection?

We expect to see governments across the world grappling with balancing strategies aimed at encouraging the development of AI and innovation while, at the same time, attempting to modernize IP and AI legal frameworks to account for AI.

Training generative AI involves using large bodies of IP-protected works/ data in ways that may be infringing under current laws. Governments seeking to “unlock” the potential of generative AI are now more often looking to legislate to permit text and data mining (TDM) of IP-protected data in order to train AI. The intellectual property in the data used to train AI models is growing as a subject of legislative discourse and is now a key issue in matters that have flooded courts across the world, whether use of copyright-protected materials to train AI models infringes copyright.

Training AI using personal data or protected IP also provides challenges to legislators worldwide. Over the next 2-3 years we expect to see increased regulatory scrutiny of companies that create or use AI technologies which have been trained using (i) personal data and/or (ii) information/data protected by IP rights. Regulators worldwide are now paying greater attention to balancing the benefits of AI against concerns about personal data and the protection of IP, and we expect that this will continue in the next few years.

Copyright

AI programs usually qualify as IP with software or computer programs being literary works. In some countries however, copyright protection will not apply for functional aspects of AI such as algorithms or system designs. AI systems function however by processing human-provided instructions to generate problem-solving outcomes. This capability makes AI-based programs highly valuable from an IP perspective, as their innovative nature and diverse utility underline their significance of IP protection.

Who owns the copyright?

Copyright laws often require that there must be a natural person to whom copyright can be attributed and many jurisdictions including the Cayman Islands and the BVI, do not provide for “computer generated” works where no human author is involved. This creates a gap in the protection of AI-generated works, which are typically produced autonomously with little or no human intervention. Many copyright laws also require that “sufficient effort” must be expended to make any literary, musical, or artistic work original in character – which involves time, human labour, and skill. What constitutes sufficient effort for AI-generated content remains largely untested, raising debates about whether crafting prompts or editing AI output meets the thresholds. Additionally, if non-human entities are recognized as “authors” then copyright duration may become complex. Generally, copyright protection is granted for an author’s lifetime plus a period of time following, potentially leading to indefinite protection for AI-generated works.

The duration of copyright protection in the Cayman Islands varies depending on the nature of the work at issue. For example:

- For Literary, Dramatic, Musical or Artistic Works: copyright expires at the end of 70 years from the end of the calendar year in which the author dies. However, if the author is unknown, copyright expires at the end of 70 years from the end of the calendar year in which the work was made or first made public

- For Computer Generated Literary, Dramatic, Musical or Artistic Works: copyright expires at the end of 50 years from the end of the calendar year in which the work was made.

- For Sound Recordings: copyright expires at the end of 50 years from the end of the calendar year in which the sound recording was made or first made public.

- For Films: copyright expires at the end of 70 years from the end of the calendar year in which the film/movie was made or first made public.

- For Broadcasts: copyright expires at the end of 50 years from the end of the calendar year in which the broadcast was made.

Copyright Protection and Deepfakes

Most IP laws are ill-equipped to address the challenges posed by digital replicas or deepfake technology. Copyright law generally is not fit for purpose in respect of deepfakes as the source material for many deepfakes either falls outside the scope of copyright protection or the copyright owner is not the individual who is harmed by the infringement. Possible causes of action presented by deepfakes include (1) copyright infringement (if a deepfake involves unauthorized use of copyrighted material), (2) trademark infringement (if it uses a registered trademark without permission), (3) the tort of passing off (if it misrepresents a product or service as endorsed by a well-known individual), (4) personal data privacy violations or (5) defamation (if the content defames an individual). The issue of whether the outputs of AI models – particularly where they substantially reproduce source materials – may infringe copyright and who may be responsible for such infringement, is also unresolved.

Is the person who infringed: the user of the AI generated work without the rights holder’s consent or the AI developer or AI system owner? This ambiguity poses risks for businesses. If there is no clear proprietary right in AI-generated works, businesses may be exposed to unnecessary risk.

AI programs usually qualify as IP with software or computer programs being literary works. In some countries however, copyright protection will not apply for functional aspects of AI such as algorithms or system designs. AI systems function however by processing human-provided instructions to generate problem-solving outcomes. This capability makes AI-based programs highly valuable from an IP perspective, as their innovative nature and diverse utility underline their significance of IP protection.

Fair dealing exceptions

With respect copyright infringement, some jurisdictions such as the Cayman Islands, BVI, U.S., U.K., Australia, Hong Kong and Singapore provide fair dealing exceptions for particular activities, despite the fact that many other jurisdictions do not.

Under Cayman Islands law and BVI law, some of the fair dealing exceptions permitted are:

- Personal copying for private use

- Non-commercial research and private study

- Text and data mining for non-commercial research

- Criticising, reviewing and reporting current events

- Use for parody, caricature and pastiche

- Making backup copies, de-compilation, observing, testing and studying, and correcting computer programme errors.

Patents

Who is the inventor? Will the requirement for “novelty” remain?

Many patent laws require the inventor to be a natural person. This requirement could exclude AI from being independently recognized as an inventor. AI-driven innovations, such as those involving algorithms and machine learning processes, face challenges in meeting the criteria for protection as an invention. Under US patent law, for example, absent at least one human inventor, an invention is not patentable. Also, the criteria for patentability in many jurisdictions (including the Cayman Islands and the BVI) usually involves requirements for novelty, an inventive step and industrial applicability. These criteria raise questions about whether AI-generated inventions can ever meet the inventive step requirement, traditionally linked to human ingenuity. AI relies on algorithms and datasets to mimic human cognitive functions, enabling it to generate patentable inventions.

We expect to see a continuing updating of guidance as to the level and type of human contributions that are necessary to support patentability as new cases make their way through courts in various jurisdictions. A vital question that arises is whether AI can be regarded as a legitimate author of content that it generates or an inventor in case of patents, given the want of legal personality of the AI itself.

AI-Driven Entity – Cayman Islands Foundation Company

A particularly effective legal structure for an AI-driven entity is the Cayman Islands foundation company. Such foundation companies do not require shareholders, allowing them to function with a governance model that can be tailored to an AI’s decision-making models. Key advantages of using such foundation companies include the following.

- Legal recognition: foundation companies can provide a defined legal entity that can interact with traditional financial institutions, sign contracts and meet compliance obligations.

- Decentralised governance: the ability to structure the foundation company without shareholders allows for governance mechanisms that can adopt smart contract-based decision-making or AI-driven decision-making.

- Asset protection and Tax mitigation: foundation company can be tax resident in the Cayman Islands, hold and manage assets and ensure legal clarity in asset ownership.

- Regulatory compliance: foundation companies can be designed to comply with regulations, including AML and CFT requirements, making them suitable for global transactions.

- Economic substance rules: foundation companies limited by guarantee are specifically exempted from the economic substance rules and can therefore hold and even make profits from intellectual property without coming under the relevant economic substance compliance regime.

This publication is not intended to be a substitute for specific legal advice or a legal opinion. For specific advice on the matters covered above, please contact your usual Loeb Smith attorney or any of the following:

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: vanisha.harjani@loebsmith.com

E: edmond.fung@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

E: yun.sheng@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

What Are Captives?

A captive insurance company is a wholly owned subsidiary insurer that provides risk mitigation services for its parent company or related entities. In its simplest form, the ‘captive’, wholly owned subsidiary is incorporated to insure against one or more risks to which its parent company is exposed. It is essentially a form of self-insurance, which is put in place within a group corporate structure for a number of reasons. Captives are usually established in the context of a company’s risk management strategy and are typically put in place because those risks that are looking to be insured by the captive are either non-insurable or priced too high in the current market.

Cayman Captives By Numbers

The captive insurance industry in the Cayman Islands recorded 42 new international insurer licenses in 2025, which was the second year in a row at that number, according to fourth-quarter data released by the Cayman Islands Monetary Authority (CIMA).

The data released by CIMA showed that at the end of 2025, the jurisdiction reported 693 Class B licences, 16 Class C licences, and 11 Class D licences, with an aggregate total of 720 licensed insurance companies in operation. These entities collectively wrote $51.2 billion in premiums and held $176.2 billion in total assets. The data showed that the premium volume reflected a 24 per cent increase compared to 2024, while total assets rose by 15 per cent over the same period.

The 693 Class B licences (mostly captives) in 2025, represented an increase from 670 in 2024 and 658 in 2023. Accordingly, captives licensed in 2025 by CIMA accounted for 96.25 per cent of all international insurer licensees in the Cayman Islands.

The Cayman Islands has historically been a jurisdiction for captive insurance companies and is currently one of the leading captive hubs in the world, both in terms of number of companies and total assets under management. This is a result of Cayman’s world-wide reputation as a highly professional, yet business friendly and well-regulated environment, with a philosophy of imposing proportionate, risk-based regulations and rules backed by consistency of enforcement.

The growing popularity of the segregated portfolio (SPC) structure in the captive insurance industry is partly due to the fact that such structures allow insurers to add additional participants in a reinsurance programme without risk of cross liability. In fact, a distinctive feature of all SPCs is that the assets and liabilities of each segregated portfolio (also referred to as ‘cells’) are, as the name suggests, segregated from one another. Each SPC cell, however, does not have legal personality. Ownership of the underlying assets in the cells is through classes or series of shares in the SPC which are designated to that particular cell.

The SPC structure is often seen in the context of the so-called ‘rent-a-captives’, whereby those wishing to reap the benefits of a captive insurance company (either for their own insurance or reinsurance) while minimising matters such as time, upfront costs, and maintenance, can simply become shareholders in an existing SPC and ‘rent’ a cell. The participants in a rent-a-captive structure pay premiums and service fees into the cell and in return they get access to the capital base they need to underwrite the risk, as well as an entitlement to any distributions made out of that cell. The SPC structure provides smaller businesses with a lower-cost entry point into the captive market, thanks to reduced premium thresholds and significantly lower formation costs.

There are also Portfolio Insurance Companies (PICs) which can be seen as a slight variation of the SPCs mentioned above. A PIC is similar to an SPC except that its cells have separate legal personality.

Other forms of captives include ‘Association Captives’, which are insurance companies owned by an association to meet the insurance needs of its members, and ‘Agency Captives’, which are insurance or reinsurance companies owned by one or more insurance agents, used to insure against the risks of those agents or any of their clients.

Key Benefits Of Cayman Captives

Cayman Islands domiciled captivesoperate primarily as Single Parent Captives (‘Pure Captives’), Group Captives, or Segregated Portfolio Companies (SPCs), allowing for bespoke insurance solutions. Businesses utilise them to manage complex risks, reduce reliance on commercial insurance, retain underwriting profits, lower insurance costs, enhance the ability to tailor coverage for hard to insure or emerging risks, enhance greater control over coverage and flexibility in managing risks, and increase the ability to allocate costs to different business units.

The continued growth of Single Parent Captives indicates that captives are increasingly being used by organisations to cover cyber risks that are difficult to place, expensive, or excluded in the traditional insurance market. By creating a wholly owned insurance entity, companies can customise policies to fit their specific risk profile, retain underwriting profits, and bridge gaps in standard cyber coverage. Group Captives act as a collaborative, accessible entry point for mid-market businesses seeking control over insurance costs and risk management, acting as an alternative to traditional insurance and costly single-parent captives. By pooling resources, members gain direct access to reinsurance markets, transparency in underwriting, and the ability to earn dividends on unused premium, particularly in casualty lines. Going forward, it is anticipated that economic uncertainty, rising premiums, and emerging risks, will drive more businesses to seek collaborative solutions that offer stability and cost efficiency.

A Class B(iii) Captive in the Cayman Islands is a specialised insurance company that writes 50 per cent or less of its net premiums from related business, requiring a minimum capital of US$200,000. These Captives are ideal for group risks, joint ventures, or scenarios with significant third-party business. They have the versatility of being suitable for complex risks that do not fit the 95 per cent single parent threshold of Class B(i) captives and can be structured as a standalone company or as an SPC.

This article was first posted in the IFC Review.

This publication is not intended to be a substitute for specific legal advice or a legal opinion. For specific legal advice on the subject matter of this Legal Insight, please contact:

Partner: Gary Smith

E: gary.smith@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

The Cayman Islands (Cayman) continues to be the leading offshore jurisdiction for the establishment of hedge funds, private equity funds, and investment funds focused on other asset classes. A large number of Cayman funds (typically private equity, venture capital or real estate focused funds) are structured as exempted limited partnerships (ELPs) where the affairs of the ELP are managed and operated by a general partner and the investors join the ELP as limited partners. The general partner is typically a Cayman exempted company (General Partner) but may also be (i) an individual resident in the Cayman Islands, (ii) a company domiciled in another jurisdiction but registered in Cayman as a foreign company, (iii) an ELP or a foreign limited partnership registered in Cayman in order to qualify as the general of the ELP.

Limited partners are prohibited from taking part in the management of an ELP and face liability risks if they do.

- Cayman’s Exempted Limited Partnership Act (As Revised) (ELP Act);

- Cayman’s Partnership Act (As Revised);

- The terms of the applicable Limited Partnership Agreement (Partnership Agreement) between the general partner(s) of the ELP and the limited partners of the ELP.

- The rules of equity and of common law applicable to partnerships so far as they have not been amended by Cayman statutory provisions listed above.

This article focuses on the main fiduciary duties of a General Partner of an ELP rather than on the General Partner’s duty of skill and care or other applicable duties arising under the ELP Act (for example, the duty to maintain a register of partners of the ELP and a register of capital contributions) that may apply to a General Partner.

FIDUCIARY DUTIES AND THEIR SCOPE

1. Duty to act in good faith in the interest of the ELP

The main fiduciary duty that a General Partner owes to the ELP and the ELP’s limited partners as a whole is the duty of loyalty and good faith. Under Cayman law this is expressed as requiring the General Partner to act in good faith in the interest of the ELP. There is no specific guidance in the ELP Act as to the full extent of this duty. There are no decisions of the Cayman Islands’ courts that have determined the full scope of the duty. However, as in other areas of Cayman law, it is reasonable to assume that the Cayman courts would refer to the decisions in English and Commonwealth cases, which are of persuasive authority if not binding authority, for guidance.

Prior to July 2014, a General Partner was under an absolute duty to act in good faith in the interest of the ELP. This duty could not be restricted, limited or varied by the terms of the Partnership Agreement between the General Partner and the limited partners. The requirement to act in the interest of the ELP often raises the issue of conflicts of interest for the General Partner, particularly when it acts as General Partner to more than one ELP.

Examples of where conflicts of interests can arise for the General Partner include:

- The General Partner causes the ELP to:

- co-invest with other ELPs (in which it is also the general partner) in only certain transactions that benefit the General Partner; or

- co-invest in disproportionate amounts, which causes its interests to be no longer directly aligned with those of the limited partners of the ELP.

- The General Partner causes the ELP to invest in a portfolio company in which the person(s) who control and/or own the General Partner, for example, the director(s) and/or shareholder(s) of the General Partner, have a personal interest.

- The General Partner causes the ELP to purchase securities from person(s) who control and/or own the General Partner, for example, the director(s) and/or shareholder(s) of the General Partner.

- The General Partner is responsible for valuing assets of the ELP where carried interest payable to the General Partner are based on such valuations.

- Treatment of limited partners: the General Partner owes a fiduciary duty to the limited partners of the ELP as a whole. Therefore the General Partner should treat each limited partner of the ELP in a similar manner. It should not benefit one at the expense of the others. Different treatment of limited partners sometimes arises in the context of default by a limited partner in performing its obligations under the Partnership Agreement. For example, where the limited partner fails to pay its contributions to the ELP when a call on its capital commitments has been made.

Often the Partnership Agreement provides that where a limited partner fails to perform any of its obligations under, or otherwise breaches the Partnership Agreement (for example, where a limited partner fails to commit additional capital when called on to do so), that limited partner may be subject to or suffer remedies for, or consequences of, the failure or breach specified in the Partnership Agreement. Such remedies or consequences can include, for example, reducing, eliminating or forfeiting the defaulting limited partner’s partnership interest in the ELP. The ELP Act confirms that those remedies or consequences in the Partnership Agreement will not be unenforceable solely on the basis that they are penal in nature. This confirmation by the ELP Act reduces significantly the risk of those remedies or consequences in the Partnership Agreement being subject to legal challenge in the Cayman courts on the basis that they are penalties (that is, remedies that go well beyond a reasonable assessment and measure of the loss suffered as a consequence of the default) and may be unenforceable as a matter of Cayman law generally.

However, there is a risk of legal challenge by a limited partner where a General Partner fails to apply a clear and consistent approach to implementing such remedies in the Partnership Agreement against defaulting limited partners. The challenge could be based on the ground that the inconsistent implementation of such default procedures benefits one limited partner at the expense of the others or vice versa.

2. Modification of duty to act in good faith in the interest of the ELP

The ELP Act modified the scope of the fiduciary duty of a General Partner to act in good faith in the interest of the ELP. There is still an absolute duty on the General Partner of an ELP to act in good faith on matters concerning the ELP. However, the duty to act in the interest of the ELP is now subject to any express provision in the Partnership Agreement to the contrary.

The Partnership Agreement can therefore stipulate the circumstances in which the General Partner may act in the interest of a party other than the ELP (for example, see above, Duty to act in good faith in the interest of the ELP). Including these circumstances in the Partnership Agreement should make it easier for the General Partner to manage interests that compete against the interests of the ELP.

However, where the Partnership Agreement has no express provision to state in whose interest the General Partner must act in given circumstances, then the default position is that the General Partner must act in good faith in the interest of the ELP (that is, in the collective interest of all limited partners of the ELP).

3. Duty to exercise its powers for the purposes for which they are conferred

A General Partner’s powers derive from the ELP Act and the Partnership Agreement governing its relationship with the limited partners. The General Partner is under a fiduciary duty to exercise its powers for the purpose(s) for which they are conferred in the Partnership Agreement. The purposes in the Partnership Agreement can be stated in general terms, for example, to undertake any lawful activity under the ELP Act, or to act as an investment fund. They can also be expressed in specific terms, for example, to invest in a portfolio consisting primarily of securities of companies in the renewable energy, renewables, clean technology, environment regeneration sectors and to engage in all activities and transactions as may be necessary, advisable, or desirable to carry out these activities. Where the Partnership Agreement of an ELP is, for example, negotiated with a large institutional investor or seed capital investor, the investor will more than likely seek to have the purpose(s) of the ELP stated in more specific terms.

4. A duty of trusteeship of the ELP’s assets

The ELP Act states that all “rights or property of every description of the [ELP], including all choses in action and any right to make capital calls and receive the proceeds thereof that is conveyed to or vested in or held on behalf of any one or more of the general partners or which is conveyed into or vested in the name of the [ELP] shall be held or deemed to be held by the general partner and if more than one then by the general partners jointly, upon trust as an asset of the [ELP] in accordance with the terms of the partnership agreement” (section 16(1), ELP Act).

As the General Partner holds the ELP’s assets on trust, it follows that it should:

- Not make any secret profits from such assets or, without express authorisation, appropriate any benefits or opportunities that derive from such assets for itself.

- Disclose personal interest in contracts involving the ELP.

- Apply the ELP’s assets for the purpose of the ELP.

ACTIONS TO REDUCE THE RISK OF BREACHING FIDUCIARY DUTIES

A General Partner can minimise the risk of breaching its fiduciary duties to the ELP and thereby the risk of being sued by one or more limited partners by adopting some or all of the following:

- Avoid conflict transactions or establish advisory committees (LPACs) or votes of limited partners to approve conflict transactions or waive conflicts. An ELP’s Partnership Agreement often provides for the establishment of an advisory committee of persons nominated by certain limited partners (LPAC) to adjudicate on, among other things, conflict situations involving the General Partner. The use of advisory committees is a good way of mitigating the risk of the General Partner being found to be in breach of its fiduciary duties for failing to deal with conflicts or dealing with them inadequately. The ELP Act confirms that, subject to any terms of the Partnership Agreement to the contrary, a member of the LPAC does not owe any fiduciary duty to the ELP or to the General Partner or to any of the ELP’s limited partners, in exercising any of its rights or otherwise in performing any of its obligations as a member of the advisory committee (section 24(2), ELP Act).

- Clear and consistent policies. The General Partner should ensure that the ELP, where possible, adopts clear and consistent valuation policies approved by the ELP’s advisory committee. The General Partner should also ensure that the ELP, where possible, adopts clear and consistent policies for dealing with circumstances where limited partners default on their obligations in the Partnership Agreement (for example, failing to make contributions when a capital call has been made). An ELP which operates as a regulated investment fund registered with the Cayman Islands Monetary Authority is required to have policies and procedures for implementing and effecting good corporate governance. This can also help to mitigate risks of liability.

- Internal compliance. The General Partner should establish clear internal procedures for identifying potential conflicts and dealing with them (for example, referral to the LPAC for consideration).

- Restrict the scope of fiduciary duties by agreement. The Partnership Agreement can be drafted in such a way as to minimise or restrict the scope of certain fiduciary duties. For example, the ELP Act now permits the Partnership Agreement to set out circumstances in which the General Partner may act in the interests of parties other than the ELP (see above, Modification of duty to act in good faith in the interest of the ELP). The Partnership Agreement can also be used to clearly exclude fiduciary duty obligations of the General Partner in other areas but this will depend on the relative bargaining power between the General Partner and incoming limited partners and the degree of negotiation of the Partnership Agreement. However, the absolute duty on the General Partner to act in good faith in respect of the ELP cannot be excluded or eliminated.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Briefing, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: elizabeth.kenny@loebsmith.com

E: vanisha.harjani@loebsmith.com

E: kate.sun@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

E: yun.sheng@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

The Cayman Islands is a leading offshore jurisdiction for investment funds known for its investor friendly regulations, tax neutrality, robust legal framework, regulatory environment, professional services infrastructure and global reach. It offers significant benefits, including no corporate income tax, capital gains tax or inheritance tax, making it attractive for fund managers as well as investors.

According to the latest data from the Cayman Islands Monetary Authority, at the end of Q4 of 2025, there were 12,876 mutual funds and 17,722 private funds registered in the Cayman Islands.

Parallel fund structures have gained popularity in recent years and are increasingly prevalent as they provide flexibility in meeting the needs of diverse investors while addressing regulatory, tax and legal considerations.

What are parallel funds?

Parallel funds are investment vehicles structured to co-invest and divest alongside a main fund, with each structure being similar in many ways to the main fund in terms of strategy, investment policy, investment target, asset classes, risk management, etc. The major distinction between the different funds in the structure are typically the tax framework (capital gains, dividend, interest, etc.) or the intention of the investment manager to differentiate each fund vehicle based on their investor group.

For example, parallel funds may include an onshore fund or mid-shore (established in any jurisdiction, e.g. Singapore or Hong Kong) and a standalone Cayman fund, both being managed by the same investment manager, with similar investment objectives and strategies, making identical investments but having different structures and a different pool of investors (e.g. US investors in one Cayman structure or Delaware structure, Japanese investors in a Singapore domiciled fund structure, and other non-US investors based in Asia in another Cayman-domiciled fund structure), in order to cater for a tax efficient framework or regulatory requirements based on investors’ jurisdiction of domicile.

Who uses parallel funds?

Parallel funds are often established by private equity (PE) fund managers to complement the main fund and address legal, tax, regulatory, accounting or other considerations from specific investors who are interested in the investment objective and strategy.

Parallel funds versus master-feeder funds. Parallel funds are distinguishable from master-feeder structures in that the feeder funds invest directly into the master fund, thereby pooling all investments in the master fund. With parallel funds, separate investment funds invest directly in the same investment deals or asset classes, but they are kept as distinct entities with no pooling of capital into a master fund.

What are the key benefits and advantages offered by parallel fund structures?

Using parallel funds provides a number of benefits to investment managers, including:

- Flexibility, allowing investment managers to tailor investment strategies and structures based on investor profiles, offering different fee structures or liquidity terms;

- Tax efficiency, providing a tax efficient way to invest without triggering adverse tax consequences in jurisdictions with stringent regulations; and

- Regulatory compliance, allowing investment managers to adapt to varying regulatory environments, ensuring compliance.

However, it would be wise to note that parallel fund structures do not come without risks, including:

- Operational issues – the investment manager may need to manage multiple funds across jurisdictions;

- Different regulatory requirements – creating more administrative responsibility and complexities in terms of operations and compliance, increasing cost; and

- Investor relations and fees – managing communications and reporting between different investor classes, and dealing with different structures and fees can cause confusion and increase the administrative burden.

When structuring parallel funds, consideration needs to be given to:

- Investment strategy alignment to ensure that funds can invest in the same underlying assets without conflicts of interest;

- Fund documentation, drafted to address the specific needs of each fund while ensuring consistency;

- Management and fees, ensuring transparency; and

- Legal and tax advice to ensure compliance with all relevant laws and regulations, and optimise the tax impact for investors.

When considering the Cayman Islands for a parallel fund structure, its robust legal framework, absence of taxes on investment funds and their investors, and flexible regulatory environment make it attractive for investment managers and investors alike.

This article was first published with Asia Business Law Journal. https://law.asia/cayman-islands-parallel-funds-growth-benefits/

***

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Article, please contact us. We would be delighted to assist.

Vanisha Harjani

E: vanisha.harjani@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Exempted limited partnerships (“ELPs”) are a form of Cayman Islands partnership which are commonly used in investment fund structures, particularly closed-ended private investment funds. This can be contrasted with open-ended mutual funds which are typically structured using a Cayman Islands exempted company.

There are a broad number of funding arrangements available to Cayman Islands investment funds and also to investors in them. For example, a fund which holds investments through an ELP as a holding vehicle may obtain debt finance from either a bank or private credit institution which is linked to the net asset value (NAV) of the fund and in exchange, the lender takes collateral over interests in the ELP that holds the fund’s investments.

Funding is also available to investors in Cayman Islands funds which will borrow to fund their capital contributions, and the lender will take collateral over the investor’s interest in the fund.

Taking collateral is straightforward where the interests being charged are shares in a typical limited liability company (such as a Cayman Islands exempted company) as that takes the form of a conventional charge over shares with supporting ancillary documents. This article explores the less well-known method of taking security over a limited partner’s interest in an ELP.

This is the first in a series of two articles. In the next article, we will consider other types of finance that are available to ELPs as well as the method of taking security over the assets of an ELP.

Limited Partner Interests

An investor in a fund that is structured as an ELP is issued with limited partnership interests (“LP Interests”) in exchange for their capital contributions. The general partner of an ELP (“General Partner”) is required to maintain a register of partnership interests containing certain prescribed information in respect of each limited partner (“Register”).

Creating security over LP Interests

Before a lender takes security over LP Interests, it must first undertake detailed due diligence in order to ensure that the security that is available matches its expectations.