What is the state of the Captive Insurance Industry in the Cayman Islands?

Updated: 21 April 2026 . 6 min readA Captive insurance company is a wholly-owned subsidiary insurer that provides risk mitigation services for its parent company or related entities. In its simplest form, the “Captive” wholly-owned subsidiary is incorporated to insure against one or more risks to which its parent company is exposed. It is essentially a form of self-insurance which is put in place within a group corporate structure for a number of reasons. Captives are usually established in the context of a company’s risk management strategy and are typically put in place because those risks which are looking to be insured by the Captive are either non-insurable or priced too high in the current market.

Captives in the Cayman Islands

The Cayman Islands has historically been a jurisdiction for Captive insurance companies and is currently one of the leading Captive hubs in the world, both in terms of number of Captive insurance companies and total assets under management, owing to Cayman’s world-wide reputation as a highly professional, yet business friendly and well-regulated environment with a philosophy of imposing proportionate, risk-based regulations and rules backed by consistency of enforcement. In particular, the Cayman Islands is the absolute leader domicile for healthcare sector Captives, with healthcare-related Captives taking up over a third of Cayman’s Captive industry. According to data released by the Cayman Islands Monetary Authority (“CIMA”) there were 693 captives) in the Cayman Islands as at the close of 2025 which accounted for 96.25% of all international insurer licensees in the Cayman Islands.

Types of Captives

Single parent Captives (more commonly known as “Pure Captives”), Segregated Portfolio Companies (“SPCs”), and Captives with two or more shareholders (“Group Captives”) make up the largest part of Captives in the Cayman Islands.

SPC’s growing popularity in the Captive insurance industry is partly owed to the fact that such structures allow insurers to add additional participants in a reinsurance programme without risk of cross liability. A distinctive feature of all SPCs, in fact, is that the assets and liabilities of each segregated portfolio (also referred to as ‘cells’) are, as the name suggests, segregated from one another. Each SPC cell, however, does not have legal personality and ownership of the underlying assets in the cells is through classes or series of shares in the SPC which are designated to that particular cell.

The SPC structure is often seen in the context of the so-called ‘Rent-A-Captives‘ whereby those wishing to reap the benefits of a Captive insurance company (either for their own insurance or reinsurance) whilst minimizing matters such as time, upfront costs and maintenance, can simply become shareholders in an existing SPC and ‘rent’ a cell. The participants in a rent-a-Captive structure pay premiums and service fees into the cell and in return they get access to the capital base they need to underwrite the risk as well as an entitlement to any distributions made out of that cell.

There are also Portfolio Insurance Companies (“PICs”) which can be seen as a slight variation of the SPCs mentioned above. A PIC is similar to an SPC except that its cells have separate legal personality.

Other forms of Captives include “Association Captives” which are insurance companies owned by an association to meet the insurance needs of its members, and “Agency Captives” which are insurance or reinsurance companies owned by one or more insurance agents and are used to insure against the risks of those agents or any of their clients.

Benefits of a Captive

The potential benefits of having a Captive insurance company include:

-

- lower insurance costs,

- tax advantages,

- underwriting profits,

- ability to tailor coverage for hard to insure or emerging risks,

- ability to apply alternative strategies to deal with insurance market cycles,

- ability to allocate costs to business units,

- provide financial incentives for loss control,

- offer flexibility in managing risk,

- offer creative insurance solutions, and consolidate risk management, and

- greater control over coverage.

Establishing a Captive: regulatory framework

As with any other industry, the Cayman Islands is a dynamic jurisdiction and strive to offer cutting edge solutions to industry problems owing to the strong relationship and continuous dialogue between the regulator and the private sector. This is no different when it comes to the insurance industry. Captives in the Cayman Islands are principally governed by the Insurance Act, 2010 (the “Act”).

To establish a Captive in the Cayman Islands CIMA will require a formal application for a Class “B” Insurer’s Licence. This application is prescribed in the Act, and requires, among other things, the following information:

-

- Name of applicant. This refers to the name that the Class “B” Insurer company will bear, which should be pre-approved for use by CIMA and the Registrar of Companies.

- A detailed business plan. CIMA will expect to see from the business plan that the proposed Captive operation has been thoroughly researched and properly planned with, among other things, feasibility studies and risk management studies supporting the proposal. It is a requirement of the Act that all Captive insurance companies appoint a local insurance manager and the appointed insurance manager is usually integrally involved in the application process.

- Three (3) years’ financial projections.

- Personal details and references for proposed directors and shareholders. A completed Personal Questionnaire should be provided in respect of ALL proposed Directors, Officers and Managers. A “police clearance certificate” is also required, but CIMA will accept a sworn Affidavit as an acceptable “other certificate”.

- Last two (2) years’ audited statements and/or notarised net worth statement of ultimate beneficial owners.

- Confirmation of appointment from a Licensed Insurance Manager and Approved Auditor.

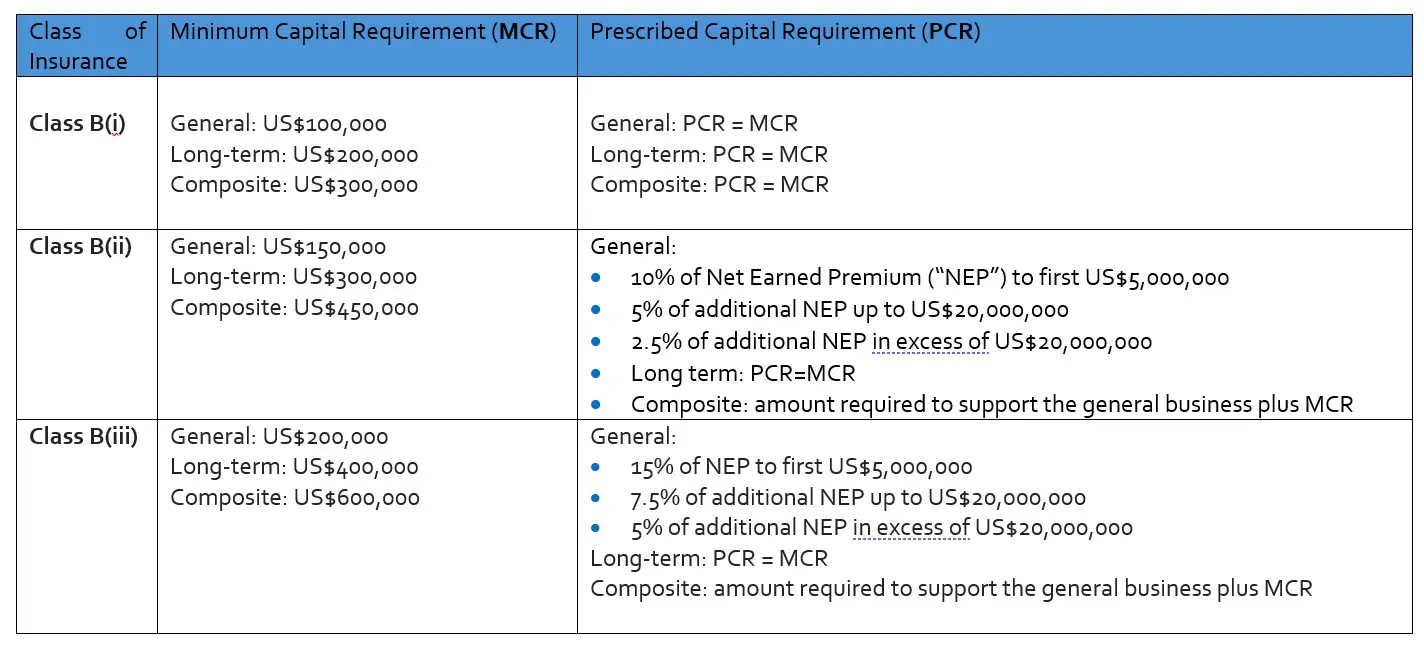

Under the Act, the Class B insurer license is reserved to Captives and is sub-divided into three sub-groups, each relating to a different percentage of the insurer’s related business underwritten by it by reference to net premiums (i.e. Class B(i) 95% or more, Class B(ii) over 50%, and Class B(iii) equal or less than 50%, respectively).

These subdivisions allow CIMA to provide for different thresholds as to (a) Minimum Capital Requirement (“MCR”), (b) Prescribed Capital Requirement (“PCR”) and, consequently, (c) margin of solvency, under The Insurance (Capital and Solvency) (Classes B, C And D Insurers) Regulations, 2012 (the “Regulations”).

a. Minimum Capital Requirement

Under the Regulations, the MCR, which is described as the minimum capital that an insurer must maintain in order to operate in accordance with the Act, for each Class B licensee is as follows:

b. Prescribed Capital Requirement

Under the Regulations, the PCR, which is described as the total risk-based capital that an insurer must maintain in order to operate in a safe and sound manner, is the same as the MCR when it comes to Class B(i) licensees, however, for Class B(ii) and Class B(iii) licensees, it is determined as a percentage by reference to the net-earned premium, which is the net written premium applicable to the expired part of the policy period or reinsurance agreement period.

c. Margin of solvency

Under the Act, margin of solvency is defined as the excess of the value of prescribed assets over prescribed liabilities. In terms of what the margin of solvency should be for each Class B licensee, the Regulations provide that it must be the same as the PCR for all three Class B sub-groups.

CIMA may impose an additional regulatory capital requirement depending upon the business plan submitted. Given the popularity of SPC structures, it is worth noting that the SPC regulatory regime which, owing to its particular stratified structure, differs slightly from the above. Under the Act, in fact, there is no MCR or PCR for cells within an SPC Captive. However, the Regulations provide that the margin of solvency requirement for cells is met so long as each cell passes both cashflow and balance sheet solvency tests.

Once the application with all requisite documentation has been submitted, the Insurance Supervision Division of CIMA will review the application and raise questions if necessary, which can be directed to the appointed insurance manager or Cayman legal counsel. Once CIMA is satisfied that the proposal is sound, a letter can be provided, addressed to the Cayman Registrar of Companies, in order for the company to be incorporated. Simultaneously, a submission for licensing will be made to CIMA’s Management Committee (MC). If approved by the MC, the licence will be issued subject to confirmation that CIMA has received the final copy of the Memorandum and Articles of Association of the company, the Certificate of Incorporation issued by the Registrar of Companies, evidence that the agreed capital has been received by the insurance manager and any other documentation previously identified by CIMA as being required.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to Captive insurance in the Cayman Islands or setting up a Captive, please contact us. We would be delighted to assist.