FUND MANAGEMENT REGULATION

Regulatory framework and authorities

1. How is fund management regulated in your jurisdiction? Which authorities have primary responsibility for regulating funds, fund managers and those marketing funds?

The main regulatory body in the Cayman Islands that regulates open- ended investment funds, closed-ended investment funds, fund managers and parties marketing investment funds is the Cayman Islands Monetary Authority (CIMA). The main statutes from which CIMA derives its supervisory powers and duties in respect of investment funds are the Mutual Funds Act and the Private Funds Act, and in respect of fund managers, is the Securities Investment Business Act (the SIB Act).

Fund administration

2. Is fund administration regulated in your jurisdiction?

A Cayman Islands-domiciled entity that carries on business as a mutual fund administrator is required to have a valid license for doing so and is required to be regulated by CIMA. There is more than one type of mutual fund administrator license and CIMA will assess, among other things, whether the applicant has sufficient expertise to administer regulated investment funds (both open-ended and closed-ended) and whether the business as a mutual fund administrator will be administered by persons who are fit and proper to be directors or, as the case may be, managers or officers in their respective positions.

Mutual fund administration is defined in the Mutual Funds Act as the management or administration of a mutual fund to provide the principal office of the mutual fund in the Cayman Islands or the provision of an operator to the mutual fund. An overseas fund administrator that is not established in the Cayman Islands is not regulated by CIMA and may be the administrator of a Cayman Islands investor fund if the administrator is authorised or otherwise permitted to carry out administration activities to investment funds in any non-high-risk jurisdiction.

Authorisation

3. What is the authorisation or licensing process for funds? What are the key requirements that apply to managers and operators of investment funds in your jurisdiction?

The vast majority of open-ended funds will qualify as mutual funds under the Mutual Funds Act (as amended), which requires mutual funds to be licensed or regulated as such. Closed-ended funds (ie, funds that issue investment interests that are not redeemable at the option of the investor of record), which fall within the scope of the Private Funds Act, are required to register with, and consequently become regulated by, CIMA.

The authorisation process for an open-ended fund will depend on the regulatory category it chooses to register under (eg, a licensed fund under section 4(1)(a) of the Mutual Funds Act, an administered fund under section 4(1)(b) of the Mutual Funds Act, a registered fund under section 4(3) of the Mutual Funds Act, or a limited investor fund under section 4(4) of the Mutual Funds Act). For closed-ended funds, the authorisation process requires the private fund to:

- submit an application for registration to CIMA within 21 days after

- its acceptance of capital commitments from investors for the purposes of investments;

- file prescribed details in respect of the private fund with CIMA;

- pay a prescribed annual registration fee to CIMA in respect of the private fund;

- comply with any conditions of its registration imposed by CIMA; and

- comply with the provisions of the Private Funds Act.

A Cayman Islands-domiciled fund manager will have to either apply to CIMA for a license to undertake business as such under the Securities Investment Business Act (as revised) or apply to CIMA to be registered under a less regulatory onerous regime as a Registered Person. An overseas fund manager can provide services to a Cayman Islands investment fund and there is no requirement for the overseas fund manager to be licensed by or registered with CIMA unless that fund manager establishes itself in the Cayman Islands. Operators of mutual funds, and private funds falling within the scope of the Private Funds Act, such as directors, are subject to registration or licensing requirements under the Director Registration and Licensing Act and are required to register with CIMA.

Territorial scope of regulation

4. What is the territorial scope of fund regulation? Can an overseas manager perform management activities or provide services to clients in your jurisdiction without authorisation?

The laws in the Cayman Islands (eg, Mutual Funds Act, Private Funds Act and SIB Act) are not extraterritorial in scope and effect. An overseas fund manager can provide services to a Cayman Islands investment fund and there is no legal requirement for the overseas fund manager to be licensed by or registered with CIMA unless that fund manager establishes operations in the Cayman Islands.

Acquisitions

5. Is the acquisition of a controlling or non-controlling stake in a fund manager in your jurisdiction subject to prior authorisation by the regulator?

There is no requirement for an overseas fund manager to be licensed by or be registered with CIMA unless that fund manager establishes itself in the Cayman Islands. Accordingly, there would be no need for any prior notification to, or authorisation by, CIMA of a change in controlling or non-controlling stake in a fund manager established overseas. A fund manager regulated in the Cayman Islands (ie, whether as a CIMA licensee or a registered person) under the SIB Act is prohibited from issuing, voluntarily transferring or disposing of any shares or partnership interests (as applicable) without the prior approval of CIMA, but CIMA may grant an exemption from this prior approval requirement where the fund manager’s securities are publicly traded on a recognised securities exchange.

Restrictions on compensation and profit sharing

6. Are there any regulatory restrictions on the structuring of the fund manager’s compensation and profit-sharing arrangements?

There are no regulatory restrictions on the structuring of the fund manager’s compensation and profit-sharing arrangements.

FUND MARKETING

Authorisation

7. Does the marketing of investment funds in your jurisdiction require authorisation?

Investment funds (whether structured as an exempted company or a limited liability company (LLC)) are restricted from making an offer of shares of the company or interests of the LLC to the public in the Cayman Islands to subscribe for such securities unless those securities are listed on the Cayman Islands Stock Exchange. This restriction on the public offer of securities is contained in the Companies Act and the Limited Liability Companies Act, but there are no similar restrictions in the laws governing limited partnerships or unit trusts. The term ‘public in the Islands’ excludes certain entities and residents, including other Cayman Islands exempted companies, LLCs, exempted limited partnerships, any exempted or ordinary non-resident companies, foreign companies registered in the Cayman Islands and foreign limited partnerships. The Private Funds Act separately states that the term ‘public in the Islands’ does not include sophisticated persons and high net worth persons (as defined under the Securities Investment Business Act (the SIB Act)), which means that making an offer of securities to ‘private funds’ (as defined in the Private Funds Act) in the Cayman Islands is not restricted. Private funds would most likely qualify as sophisticated persons or high net worth persons, or both.

An overseas investment fund that wishes to make an offering of its securities to the public in the Cayman Islands will need to either (1) register with the Cayman Islands Monetary Authority (CIMA) as a mutual fund under the Mutual Funds Act or a private fund under the Private Funds Act or (2) market its securities through a person who is appropriately licensed or authorised by CIMA under the terms of the SIB Act (provided that the securities being offered to the public in the Cayman Islands are listed on a stock exchange approved by CIMA or the investment fund is regulated by a recognised overseas regulatory authority approved by CIMA).

8. What marketing activities require authorisation?

Arranging deals in securities with a view to another person dealing in securities or participating in the arrangements for dealing in securities are regulated under the SIB Act and, therefore, would require prior authorisation from CIMA.

Territorial scope and restrictions

9. What is the territorial scope of your regulation? May an overseas entity perform fund marketing activities in your jurisdiction without authorisation?

An entity that is performing marketing activities for an investment fund from within the Cayman Islands is required by the terms of the SIB Act to obtain a licence from, or otherwise register with, CIMA, prior to engaging in such activities.

10. If a local entity must be involved in the fund marketing process, how is this rule satisfied in practice?

There is no legal requirement for a local entity to be involved in the fund marketing process.

Commission payments

11. What restrictions are there on intermediaries earning commission payments in relation to their marketing activities in your jurisdiction?

There are no legal restrictions on intermediaries earning commission payments in relation to their marketing activities in the Cayman Islands.

RETAIL FUNDS

Available vehicles

12. What are the main legal vehicles used to set up a retail fund? How are they formed?

The statutory and regulatory frameworks that apply to investment funds in the Cayman Islands do not distinguish between retail funds and non-retail funds as the Cayman Islands is not primarily known as a retail fund jurisdiction. Its laws and regulations applicable to investment funds are geared mainly towards attracting institutional investors. Accordingly, the legal vehicle used for an investment fund is typically based on whether the fund’s strategy will be open-ended or closed- ended. The exempted company (which includes the segregated portfolio company) is the most commonly used legal vehicle for open-ended funds and the exempted limited partnership is the most commonly used legal vehicle for closed-ended funds. Both types of legal vehicles are formed by filing formation documents with the Companies Registry and paying the requisite government fee. There are no special requirements that apply to managers or operators of retail funds (which for present purposes are taken to mean funds that permit an investor to invest an initial minimum amount of less than US$100,000).

Laws and regulations

13. What are the key laws and other sets of rules that govern retail funds?

The statutory and regulatory frameworks that apply to investment funds in the Cayman Islands do not distinguish between retail funds and non-retail funds. Under section 4(1)(b) of the Mutual Funds Act, a mutual fund can register with the Cayman Islands Monetary Authority (CIMA) and permit its investors to each invest an initial minimum amount of less than US$100,000. This type of fund is often referred to as a ‘retail’ fund. However, the regulatory framework that applies to this category of mutual fund (referred to as an administered fund) is pretty much the same as is applicable to other mutual funds registered with CIMA. Closed-ended funds that fall within the scope of the Private Funds Act and are, therefore, registered with, and regulated by, CIMA do not have a minimum initial investment threshold set by law and, therefore, investors will simply have to comply with the investment limits and restrictions set by the manager or operator of the fund.

The Retail Mutual Funds (Japan) Regulations are an exception to the above in that they effectively make a distinction between retail funds and non-retail funds by providing a compliance framework for certain licensed funds under section 4(1)(a) of the Mutual Funds Act that will market to retail investors in Japan, enabling these funds to automatically comply with the applicable securities laws and regulations in Japan. However, these funds are merely a sub-set of licensed funds, which themselves only comprise approximately 1 per cent of Cayman Islands’ mutual funds.

Authorisation

14. Must retail funds be authorised or licensed to be established or marketed in your jurisdiction?

All mutual funds and all closed-ended funds that fall within the scope of the Private Funds Act are required to be registered with, and be regulated by, CIMA.

Marketing

15. Who can market retail funds? To whom can they be marketed?

Investment funds (whether structured as an exempted company or a limited liability company (LLC)) are restricted from making an offer of shares of the company or interests of the LLC to the public in the Cayman Islands to subscribe for such securities unless those securities are listed on the Cayman Islands Stock Exchange. There are no similar restrictions in the laws governing limited partnerships or unit trusts. The term ‘public in the Islands’ excludes certain entities and residents, including other Cayman Islands exempted companies, LLCs, exempted limited partnerships, any exempted or ordinary non-resident companies, foreign companies registered in the Cayman Islands and foreign limited partnerships. It also excludes sophisticated persons and high net worth persons (as defined under the Securities Investment Business Act (SIB Act)), which means that making an offer of securities to ‘private funds’ (as defined in the Private Funds Act) in the Cayman Islands is not restricted. Private funds would most likely qualify as sophisticated persons or high net worth persons, or both. An overseas investment fund that wishes to make an offering of its securities to the public in the Cayman Islands will need to either (1) register with CIMA as a mutual fund under the Mutual Funds Act or a private fund under the Private Funds Act or (2) market its securities through a person who is appropriately licensed or authorised by CIMA under the terms of the SIB Act (provided that the securities being offered to the public in the Cayman Islands are listed on a stock exchange approved by CIMA or the investment fund is regulated by a recognised overseas regulatory authority approved by CIMA). However, there is no legal requirement for a local entity to be involved in the fund marketing process.

Managers and operators

16. Are there any special requirements that apply to managers or operators of retail funds?

The statutory and regulatory framework that apply to investment funds in the Cayman Islands do not distinguish between retail funds and non- retail funds. There are no special requirements that apply to managers or operators of retail funds.

Investment and borrowing restrictions

17. What are the investment and borrowing restrictions on retail funds?

There are no specific legal investment and borrowing restrictions on retail funds under Cayman Islands laws.

Tax treatment

18. What is the tax treatment of retail funds? Are exemptions available?

The tax treatments and exemptions available to non-retail funds apply equally to retail funds.

Asset protection

19. Must the portfolio of assets of a retail fund be held by a separate local custodian? What regulations are in place to protect the fund’s assets?

There are no legal requirements in the Cayman Islands for assets of a mutual fund to be held by a separate custodian located in the Cayman Islands. Closed-ended funds that fall within the scope of the Private Funds Act are required to appoint a custodian:

- to hold the private fund’s assets that are capable of physical delivery or capable of registration in a custodial account except where that is neither practical nor proportionate given the nature of the private fund and the type of assets held; and

- to verify title to, and maintain records of, fund assets. However, there is no legal requirement for the custodian to be located in the Cayman Islands.

Governance

20. What are the main governance requirements for a retail fund formed in your jurisdiction?

Mutual funds regulated by CIMA must, as long as there is a continuing offering, update their offering documents and prescribed particulars within 21 days of any material change, and are required to file the updated offering document or the prescribed particulars with CIMA within this 21-day period.

A private fund is required under the Private Funds Act to notify CIMA of any change that materially affects any information submitted to CIMA and of any change of its registered office or the location of its principal office.

The private fund will have 21 days after making the change or becoming aware of the change to file details of the change with CIMA.

All funds regulated by CIMA (mutual funds and private funds) are required to have their accounts audited annually and such audited financial statements must be filed with CIMA within six months of the year end of the fund, along with a financial annual return form including prescribed details, signed by a director. These audited financial statements must be signed off by a CIMA approved Cayman Islands-based audit firm.

Reporting

21. What are the periodic reporting requirements for retail funds?

Mutual funds regulated by CIMA must, as long as there is a continuing offering, update their offering documents and prescribed particulars within 21 days of any material change, and are required to file the updated offering document or the prescribed particulars with CIMA within this 21-day period.

A private fund is required under the Private Funds Act to notify CIMA of any change that materially affects any information submitted to CIMA and of any change of its registered office or the location of its principal office.

The Private Fund will have 21 days after making the change or becoming aware of the change to file details of the change with CIMA.

All funds regulated by CIMA (mutual funds and private funds) are required to have their accounts audited annually and such audited financial statements must be filed with CIMA within six months of the year end of the fund, along with a financial annual return form including prescribed details, signed by a director. These audited financial statements must be signed off by a CIMA approved Cayman Islands-based audit firm.

Issue, transfer and redemption of interests

22. Can the manager or operator place any restrictions on the issue, transfer and redemption of interests in retail funds?

Restrictions can be contained in the constitutive documents of a fund or otherwise in the terms of issue of the relevant equity interests or investment interests of the fund.

NON-RETAIL POOLED FUNDS

Available vehicles

23. What are the main legal vehicles used to set up a non-retail fund? How are they formed?

Open-ended funds

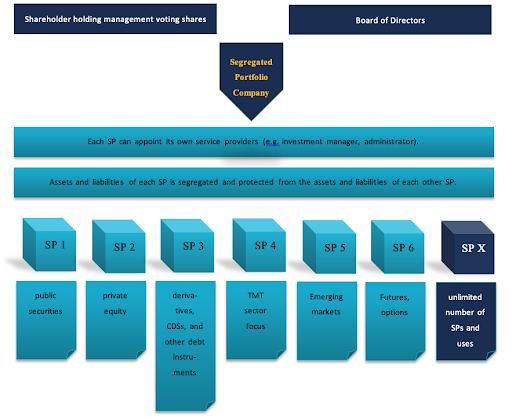

Exempt companies

Exempt companies are the most common legal vehicle for open-ended funds. The exempted company limited by shares and the exempted segregated portfolio companies (SPCs) make up the overwhelming majority of open-ended funds and accounted for over 85 per cent of total open-ended funds registered with the Cayman Islands Monetary Authority (CIMA) as at the end of 2019.

It is possible to incorporate an exempted company limited by shares (including an SPC) on either a standard basis (which takes four to five business days after submission of formation documents to the Registrar of Companies) or on an express (same day) basis subject to paying an additional express fee. Incorporation is effected by filing the company’s memorandum and articles of association and an affidavit sworn by the subscriber to the memorandum of association with the Registrar of Companies. Unless the company proposes to use a restricted word in its name (e.g., ‘bank’ or ‘insurance’) no prior consent or approval is required from CIMA or any other government agency. The memorandum of association is required to contain certain basic information about the company, including its registered office address, its authorised share capital and the objects for which it is incorporated. Shares can be denominated in any currency and denomination. There is no minimum or maximum amount prescribed for authorised, issued or paid-up share capital (although at least one share must be in issue at the time of incorporation).

LLCs

A limited liability company (LLC) is a corporate entity that has separate legal personality to its members. Formation of an LLC requires the filing of a registration statement with the Registrar of Companies and payment of the requisite government fee. The LLC must have at least one member and it can be member managed (by some or all of its members) or the LLC agreement can provide for the appointment of persons (who need not be members) to manage and operate the LLC. The liability of an LLC’s members is limited and members can have capital accounts and can agree among themselves (in the LLC agreement) how the profits and losses of the LLC are to be allocated and how and when distributions are to be made (similar to a Cayman Islands exempted limited partnership). An LLC may be formed for any lawful business, purpose or activity and it has full power to carry on its business or affairs unless its LLC agreement provides otherwise. An LLC may (but is not required to) use one of the following suffixes in its name: Limited Liability Company, LLC or L.L.C.

The LLC structure is an attractive option for certain Cayman closed-ended investment funds (eg, they facilitate aligning the rights of investors in onshore and offshore investment funds in a main fund and sub-fund structures) as well as for general partner entities and other carried interest distribution vehicles.

Limited partnerships

Exempted limited partnerships (ELPs) are most commonly used for closed-ended funds and, to the extent that they fall within the scope of the Private Funds Act, are required to be registered with CIMA.

Unit trusts

Unit trusts are based on English trust law, but are modified by the Trusts Act of the Cayman Islands for suitability as investment fund vehicles. Under a unit trust arrangement, investors contribute funds to a trustee that holds those funds on trust for the investors and each investor is directly entitled to share pro rata in the trust’s assets. An advantage of the unit trust is that it may be structured as an ‘umbrella’ unit trust so that different investments may be allocated to different ‘sub-trusts’ with investors subscribing for units in a particular sub-trust. Unlike SPCs, however, there is no statutory segregation of assets and liabilities of each sub-trust.

A unit trust is formed through a declaration of trust by the trustee alone or by a trust deed executed by both the trustee and the investment manager.

Closed-ended funds

The legal vehicles that can be used for closed-ended funds are the same as for open-ended funds. The most popular vehicle used for closed- ended funds is the ELP. Cayman ELPs are governed by a combination of equitable and common law rules (based on English common law) and also statutory provisions, pursuant to the Exempted Limited Partnership Act (as revised). An ELP may be formed for any lawful purpose to be carried out and undertaken either in or from within the Cayman Islands or elsewhere upon the terms, with the rights and powers, and subject to the conditions, limitations, restrictions and liabilities set forth in the Exempted Limited Partnership Act.

An ELP is a legal arrangement and does not have separate corporate personality. The terms of the ELP are set out in a limited partnership agreement and registered in the Cayman Islands by filing a registration statement with the Registrar of Exempted Limited Partnerships containing the following details:

- the name of the partnership;

- the general nature of the business and term of the partnership;

- the address of the registered office of the partnership;

- the name and address of its general partner; and

- a declaration that the partnership shall not undertake business with the public in the Cayman Islands other than so far as may be necessary to conduct business outside the Cayman Islands.

Laws and regulations

24. What are the key laws and other sets of rules that govern non-retail funds?

Open-ended funds

The Mutual Funds Act (for open-ended funds) and the Private Funds Act (for closed-ended funds) are the two main statutes relevant to the regulation of investment funds in the Cayman Islands. CIMA is the regulatory body responsible for compliance with these laws and related regulations and has broad powers of enforcement.

The Mutual Funds Act defines a mutual fund as ‘a company, unit trust or partnership that issues equity interests, the purpose or effect of which is the pooling of investor funds with the aim of spreading investment risks and enabling investors in the mutual fund to receive profits or gains from the acquisition, holding, management or disposal of investments…’ The reference to ‘equity interests’ means that debt instruments (including warrants, convertibles and sukuk instruments) are excluded and funds issuing such instruments will not be required to register with CIMA as a mutual fund. The scope of regulation extends to Cayman incorporated or established master funds that have one or more CIMA-regulated feeder funds and hold investments and conduct trading activities. Recent changes to the Mutual Funds Act means that certain mutual funds, which were previously exempted from registration with CIMA under section 4(4) of the Mutual Funds Act because they had 15 investors or less, the majority of whom have the power to appoint or remove the operators of the investment fund (the operator being the directors, the general partner or the trustee, as is relevant given the legal vehicle used for the fund), are no longer exempt from registration with CIMA. These limited investor funds are now required to be registered with, and are regulated by, CIMA.

Each CIMA-registered mutual fund is required to have its accounts audited annually by a firm of auditors on the CIMA-approved list of auditors and file such audited accounts with CIMA within six months of the end of each financial year of the mutual fund (along with a financial annual return in CIMA’s prescribed form).

Mutual funds that are established for a sole investor and do not involve the pooling of investor funds fall outside the regulatory framework of the Mutual Funds Act. Nonetheless, a mutual fund with a single investor can apply for voluntary registration to, among other things, benefit from the status of being a regulated fund.

Cayman Islands laws and regulations do not impose restrictions on, or prescribe rules for investment strategies of open-ended funds, or their use of leverage, shorting or other techniques.

Closed-ended funds

The Private Funds Act requires the registration of closed-ended funds (typically, investment funds that do not grant investors with a right or entitlement to withdraw or redeem their shares or interests from the fund upon notice) with CIMA. The Private Funds Act applies to private equity funds, real estate funds, and other types of closed-ended funds set up as Cayman Islands limited partnerships, companies (including SPCs), unit trusts and limited liability companies. The Private Funds Act also applies to non-Cayman Islands private funds carrying on business or attempting to carry on business in or from the Cayman Islands.

In addition to registration with CIMA, the Private Funds Act also imposes the following regulatory requirements to be met by private funds.

Audit

Each private fund is required to have its accounts audited annually by a firm of auditors on the CIMA-approved list of auditors and file such audited accounts with CIMA within six months of the end of each financial year of the private fund (along with a financial annual return in CIMA’s prescribed form).

Valuation of assets

A private fund must have appropriate and consistent procedures for the purposes of proper valuations of its assets, which ensures that valuations are conducted in accordance with the requirements in the Private Funds Act. Valuations of the assets of a private fund are required to be carried out at a frequency that is appropriate to the assets held by the private fund and, in any case, on at least an annual basis.

Safekeeping of fund assets

The Private Funds Act requires a custodian: (1) to hold the private fund’s assets that are capable of physical delivery or capable of registration in a custodial account except where that is neither practical nor proportionate given the nature of the private fund and the type of assets held; and (2) to verify title to, and maintain records of, fund assets.

Cash monitoring

The Private Funds Act requires a private fund to appoint an administrator, custodian or another independent third party (or the manager or operator of the private fund):

- to monitor the cash flows of the private fund;

- to ensure that all cash has been booked in cash accounts opened in the name, or for the account, of the private fund; and

- to ensure that all payments made by investors in respect of investment interests have been received.

Identification of securities

A private fund that regularly trades securities or holds them on a consistent basis must maintain a record of the identification codes of the securities that it trades and holds and make this available to CIMA upon request.

Directors of mutual funds structured as exempted companies, managers of investment funds structured as LLCs and directors of general partners of investment funds structured as an exempted limited partnership (in each case, wherever in the world these persons are located, not just to Cayman Islands-based directors) regulated by CIMA are required to register with CIMA under the Directors Registration and Licensing Act (DRLA). The DRLA enables CIMA to verify certain information in respect of directors or managers of CIMA-registered funds. There is currently no requirement for registration of directors with CIMA under the DRLA who are directors of closed-ended funds that fall within the scope of the Private Funds Act. However, this may change in the future.

All investment funds are required to comply with Cayman Islands anti-money laundering legislation and regulations, including appointing an anti-money laundering compliance officer, a money laundering reporting officer, and a deputy money laundering reporting officer. The Cayman Islands government and CIMA actively work with the European Union, the Organisation for Economic Co-operation and Development, the Financial Action Task Force and regulators in numerous jurisdictions to observe and maintain international standards on transparency and good corporate governance.

Authorisation

25. Must non-retail funds be authorised or licensed to be established or marketed in your jurisdiction?

The statutory and regulatory frameworks that apply to investment funds in the Cayman Islands do not distinguish between retail funds and non-retail funds. All mutual funds (except for those that are single investor funds) are required to be registered with CIMA and fall within its regulatory framework. Closed-ended funds that fall within the scope of the Private Funds Act are required to be registered with, and regulated by, CIMA.

Marketing

26. Who can market non-retail funds? To whom can they be marketed?

Investment funds (whether structured as an exempted company or a LLC) are restricted from making an offer of shares of the company or interests of the LLC to the public in the Cayman Islands to subscribe for such securities unless those securities are listed on the Cayman Islands Stock Exchange. There are no similar restrictions in the laws governing limited partnerships or unit trusts. The term ‘public in the Islands’ excludes certain entities and residents, including other Cayman Islands exempted companies, LLCs, exempted limited partnerships, any exempted or ordinary non-resident companies, foreign companies registered in the Cayman Islands and foreign limited partnerships. It also excludes sophisticated persons and high net worth persons (as defined under the Securities Investment Business Act (the SIB Act)), which means that making an offer of securities to ‘private funds’ (as defined in the Private Funds Act) in the Cayman Islands is not restricted. Private funds would most likely qualify as sophisticated persons or high net worth persons, or both. An overseas investment fund that wishes to make an offering of its securities to the public in the Cayman Islands will need to either (1) register with CIMA as a mutual fund under the Mutual Funds Act or a private fund under the Private Funds Act or (2) market its securities through a person who is appropriately licensed or authorised by CIMA under the terms of the SIB Act (provided that the securities being offered to the public in the Cayman Islands are listed on a stock exchange approved by CIMA or the investment fund is regulated by a recognised overseas regulatory authority approved by CIMA). However, there is no legal requirement for a local entity to be involved in the fund marketing process.

Ownership restrictions

27. Do investor-protection rules restrict ownership in non-retail funds to certain classes of investor?

The legal requirement to be an eligible investor in a registered mutual fund with more than 15 investors is a minimum initial investment of US$100,000 (or its equivalent in any other currency); otherwise, no other investor-qualification criteria apply to such funds. This minimum initial investment requirement does not apply to registered mutual funds with 15 or fewer investors and also does not apply to closed-ended funds falling within the scope of the Private Funds Act.

Managers and operators

28. Are there any special requirements that apply to managers or operators of non-retail funds?

There is no requirement for the manager of a Cayman Islands fund to be resident or domiciled in the Cayman Islands. There are no Cayman Islands laws that seeks to regulate overseas managers of Cayman investment funds. Fund managers established in the Cayman Islands need to comply with the provisions of the Securities Investment Business Act and such fund managers must either be licensed or registered with the CIMA. There are also economic substance requirements which must be complied with.

Directors of mutual funds structured as exempted companies, managers of investment funds structured as LLCs and directors of general partners of investment funds structured as exempted limited partnerships (in each case, wherever in the world these persons are located, not just to Cayman Islands-based directors) regulated by CIMA are required to register with CIMA under the DRLL. The DRLL enables CIMA to verify certain information in respect of directors or managers of CIMA-registered funds. There is currently no requirement for registration of directors with CIMA under the DRLL who are directors of closed-ended funds that fall within the scope of the Private Funds Act. However, this may change in the future.

Tax treatment

29. What is the tax treatment of non-retail funds? Are any exemptions available?

Cayman Islands tax treatment is the same for both retail funds and non-retail funds.

The Cayman Islands has no direct taxation of any kind. There is no income, corporation, capital gains or withholding taxes or death duties. It is possible for all types of Cayman legal structures (exempted company, LLC, unit trust and ELP) to apply to the Cayman Islands government for a tax undertaking that the legal structure will not be subject to direct taxation, for a minimum period, which in the case of a company is 20 years, and in the case of an LLC, unit trust and an ELP is 50 years.

Asset protection

30 Must the portfolio of assets of a non-retail fund be held by a separate local custodian? What regulations are in place to protect the fund’s assets?

There are no legal requirements in the Cayman Islands for assets of a mutual fund to be held by a separate custodian located in the Cayman Islands. Closed-ended funds that fall within the scope of the Private Funds Act are required to appoint a custodian (1) to hold the private fund’s assets that are capable of physical delivery or capable of registration in a custodial account except where that is neither practical nor proportionate given the nature of the private fund and the type of assets held; and (2) to verify title to, and maintain records of, fund assets. However, there is no legal requirement for the custodian to be located in the Cayman Islands.

Governance

31. What are the main governance requirements for a non-retail fund formed in your jurisdiction?

The Mutual Funds Act (for open-ended funds) and the Private Funds Act (for closed-ended funds) are the two main statutes relevant to the regulation of investment funds in the Cayman Islands. CIMA is the regulatory body responsible for compliance with these laws and related regulations and has broad powers of enforcement. Depending on the legal structure of the investment fund, there are also various continuing filing obligations and annual registration fees to be paid.

Reporting

32. What are the periodic reporting requirements for non-retail funds?

Mutual funds regulated by CIMA must, as long as there is a continuing offering, update their offering documents and prescribed particulars within 21 days of any material change, and are required to file the updated offering document or the prescribed particulars with CIMA within this 21-day period.

A private fund is required under the Private Funds Act to notify CIMA of any change that materially affects any information submitted to CIMA and any change of its registered office or the location of its principal office.

The Private Fund will have 21 days after making the change or becoming aware of the change to file details of the change with CIMA.

All funds regulated by CIMA (mutual funds and private funds) are required to have their accounts audited annually, and these audited financial statements must be filed with CIMA within six months of the year end of the fund, along with a financial annual return form including prescribed details, signed by a director. These audited financial statements must be signed off by a CIMA-approved Cayman Islands-based audit firm.

SEPARATELY MANAGED ACCOUNTS

Structure

33. How are separately managed accounts typically structured in your jurisdiction?

Separately managed accounts are not typically structured using Cayman entities. The investment manager entity that provides managed account services may itself be a Cayman-domiciled entity and be regulated by the Cayman Islands Monetary Authority.

Key legal issues

34. What are the key legal issues to be determined when structuring a separately managed account?

There are no specific Cayman Islands legal requirements to be determined when structuring a separately managed account unless the managed account is structured using a Cayman legal vehicle, in which case the same issues applicable to a mutual fund or a private fund may apply.

Regulation

35. Is the management or marketing of separately managed accounts regulated in your jurisdiction?

The manager or entity marketing the separately managed account is regulated in the same manner as fund management.

GENERAL

Proposed reforms

36. Are there proposals for further regulation of funds, fund managers or marketers of funds in your jurisdiction?

The introduction of (1) the requirement to register with the Cayman Islands Monetary Authority (CIMA), mutual funds that were previously exempted from registration, and (2) the registration of private funds with CIMA under the terms of the Private Funds Act has expanded the regulatory landscape for Cayman investment funds considerably. It is anticipated that there will be accompanying regulations that will set out in more detail how this expanded regulatory landscape will apply.

Public listing

37. Outline any specific requirements for stock-exchange listing of retail and non-retail funds.

The listing of investment funds on the Cayman Islands stock exchange covers all types of legal vehicles (eg, exempted company (including segregated portfolio companies), limited liability company, unit trust or limited partnership) and every type of strategy (closed-ended funds, open-ended funds, stand-alone and master-feeder funds, real estate funds or umbrella funds) can apply to be listed. Funds based in both the Cayman Islands and in other jurisdictions are permitted under the listing rules to apply.

Overseas vehicles

38. Is it possible to redomicile an overseas vehicle in your jurisdiction?

Yes.

Foreign investment

39. Are there any special rules relating to the ability of foreign investors to invest in funds established or managed in your jurisdiction or domestic investors to invest in funds established or managed abroad?

There are no special rules.

Funds investing in derivatives

40. Are there any special requirements in your jurisdiction relating to funds investing in derivatives?

Answer in progress.

UPDATE AND TRENDS

Recent developments

41. Are there any other current developments or emerging trends in your jurisdiction that should be noted? Please include reference to world-wide regulatory concerns, such as restrictions on foreign ownership in strategic industries, high-frequency trading, commodity position limits, capital adequacy for investment firms and ‘shadow banking’.

There are no updates at this time.

Coronavirus

42. What emergency legislation, relief programmes and other initiatives specific to your practice area has your state implemented to address the pandemic? Have any existing government programmes, laws or regulations been amended to address these concerns? What best practices are advisable for clients?

The information in this chapter was verified between May and June 2020.

Gary Smith

E: gary.smith@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Attached is the May 2021 publication of the Technical Brief for Investment Funds, a newsletter developed by the Loeb Smith Cayman Islands Investment Funds Technical Team. As regulatory compliance becomes increasingly a key focus for both Cayman investment funds and CIMA as regulator, this Technical Brief covers, among other things:

FATCA/CRS Summary and Update

Considerations for Directors of Cayman Regulated Open-ended Funds

Cayman Islands’ Rule on Cybersecurity for Regulated Entities

New Administrative Fines for breach of Regulatory Laws.

If you have any questions, please reach out to your usual Loeb Smith contacts or any member of our Investment Funds Technical Team shown in the Bulletin

The Cayman Islands Monetary Authority (“CIMA”) released a Notice on 19 April 2021 to confirm that the deadline for the first filing of audited accounts for Private Funds and the Fund Annual Return (FAR) form which is also required to be filed annually has been extended to 30 September 2021.

The extension relates only to the audited accounts and FAR forms for Private Funds and does not apply to open-ended mutual funds registered under the Mutual Funds Act (2021 Revision). The audited accounts and FAR forms for mutual funds are still required to be filed within six (6) months of each relevant Fund’s financial year end.

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Cayman Islands exempted companies are widely utilized in structuring cross-border finance transactions. One of the key reasons for this is that the Cayman Islands provides a flexible and well-tested regime for secured financing transactions that is attractive to borrowers and lenders alike.

In this brief guide, we address certain of the key Cayman Islands law points pertaining to the enforcement of an equitable mortgage over shares (the “Secured Shares”) in a Cayman Islands exempted company (the “Secured Company”). An equitable mortgage is the most popular form of security over Secured Shares in a Secured Company.

For details regarding the creation and protection of security over Secured Shares in a Secured Company, please refer to our guide entitled “Granting and protecting security over shares in a Cayman Islands exempted company”.

1. Security deliverables and power of attorney

The terms of a well-drafted Cayman Islands law governed security document with respect to Secured Shares in a Secured Company and the principal finance document will usually require the security provider to deliver the following documents to the secured party to assist with an enforcement:

i. any original share certificate(s) with respect to the Secured Shares in the Secured Company;

ii. an undated share transfer form with respect to the Secured Shares in the Secured Company – the secured party may date this and insert details of the transferee in an enforcement for the purposes of transferring the Secured Shares to itself or a nominee;

iii. an undated resignation letter from each director of the Secured Company – the secured party may date these in an enforcement for the purposes of removing the existing directors of the Secured Company;

iv. a letter of authorization from each director of the Secured Company authorizing the secured party to date each undated letter of resignation upon the occurrence of a default under the security document;

v. an irrevocable proxy with respect to the Secured Shares in the Secured Company in favor of the secured party – this can assist the secured party in taking control of the Secured Company before a transfer of Secured Shares in the Secured Company has been completed;

vi. a letter of instruction to the Secured Company’s registered office service provider containing, among other things, directions to register a transfer of Secured Shares in the Secured Company upon the occurrence of a default under the security document;

vii. a letter of acknowledgement from the registered office service provider with respect to the instructions contained in the letter of instruction;

viii. if the security provider is a Cayman Islands exempted company, a certified copy of its register of mortgages and charges showing the security created over the Secured Shares in the Secured Company – refer to our guide entitled “Granting and protecting security over shares in a Cayman Islands exempted company” for further details;

ix. a certified copy of the Secured Company’s register of members annotated to show the security created over the Secured Shares in the Secured Company (if commercially agreed) – refer to our guide entitled “Granting and protecting security over shares in a Cayman Islands exempted company” for further details;

x. if the security provider is a Cayman Islands exempted company, a copy of the board resolutions of its board of directors authorizing:

a. its entry into and execution of the security document; and

b. the updates to its register of mortgages and charges;

xi. a copy of the board resolutions of the Secured Company authorizing:

a. its entry into and execution of the security document (if it is a party);

b. its register of members to be annotated (if commercially agreed); and

c. a transfer of Secured Shares upon the occurrence of a default under the security document; and

xii. a special resolution passed by the Secured Company with respect to certain changes to its memorandum of association and articles of association (the “M&A”), if required – refer to our guide entitled “Granting and protecting security over shares in a Cayman Islands exempted company” for further details.

A well-drafted share mortgage will include an irrevocable power of attorney granted by the security provider in favor of the secured party enabling it to date and complete the share transfer form in respect of the Secured Shares in the Secured Company and the other documents requiring completion on enforcement.

2. Enforcement rights and remedies

Cayman Islands law permits security over Secured Shares in a Secured Company to be governed by Cayman Islands law or foreign law. One advantage of adopting a foreign governing law clause in a security document is that it may make available certain additional remedies (such as appropriation) which are not available under Cayman Islands law.

Cayman Islands law governed equitable share mortgage

Power of sale

A secured party will usually acquire a power of sale:

i. as a matter of common law; and

ii. as a matter of contract pursuant to the terms of the security document.

It is not necessary to obtain a court order to exercise the power of sale, though it may be preferable to do so in certain circumstances. For example, if the secured party wishes to buy the Secured Shares in a Secured Company or sell them to a third party in a depressed market, a court order may protect the secured party from a claim that it did not receive the best price reasonably obtainable.

Receivership

A secured party will acquire the right to appoint a receiver as a matter of contract pursuant to the terms of any well-drafted security document. This is the most common method of enforcing share security and is an out of court procedure.

Once a receiver has been appointed, it can vote and sell the Secured Shares in the relevant Secured Company, as well as receive any distributions from the Secured Shares. A receiver will usually remove the Secured Company’s existing directors once appointed and liquidate the Secured Company’s underlying assets to facilitate repayment of the debt.

Taking possession

The secured party may also take possession of the Secured Shares in a Secured Company by becoming registered as the legal owner of the Secured Shares. It can do this by dating and completing the share transfer form and presenting it to the Secured Company’s registered office service provider for the purposes of updating the Secured Company’s register of members. It can then also exercise any shareholder rights that become available.

Foreclosure

If the secured party acquires legal title to the Secured Shares in a Secured Company, it also has a right of foreclosure. This remedy extinguishes the security provider’s legal and beneficial title to the Secured Shares in the Secured Company but not its obligation to pay any secured and unpaid sums. Foreclosure involves a time-consuming and costly court process and is not usually exercised in practice given its draconian nature.

Foreign law governed share security document

Where the security document is governed by foreign law, the:

i. security document should comply with the requirements of its governing law to be valid and binding; and

ii. remedies available to a secured party are governed by the governing law and the terms of the security document.

3. Application of proceeds of enforcement

Subject to any provisions to the contrary in the security document, all amounts that accrue from the enforcement of the security document are applied in the following order of priority:

i. firstly, in paying the costs incurred in enforcing the security document;

ii. secondly, in discharging the sums secured by the security document;

iii. and thirdly, in paying any balance due to the security provider.

4. Stop notices

If the secured party has concerns that the security provider may transfer the Secured Shares in the relevant Secured Company to a third party or pay a distribution with respect to them in breach of the terms of the security document before any enforcement action has been completed, it may be possible to obtain a stop notice.

A stop notice does not require a court hearing and is obtained from the Registrar of the Grand Court (the “Registrar of the Court”). Upon a successful application, the Registrar of the Court issues a stop notice requiring 14 days’ notice to be given to the secured party before any transfer of Secured Shares in the relevant Secured Company or any payment of a distribution with respect to them can occur.

5. Rectification of the register of members

To the extent that the registered office service provider of a Secured Company is uncooperative in updating the register of members of that Secured Company to reflect a transfer of Secured Shares, the secured party may apply to court to rectify the register on the grounds that there has been an unnecessary delay in entering it as a new shareholder.

This publication is not intended to be a substitute for specific legal advice or a legal opinion. For specific advice, please contact:

Peter Vas

Partner

Loeb Smith Attorneys

Hong Kong

T: +852 5225 4920

E: peter.vas@loebsmith.com

Cayman Islands exempted companies are widely utilized in structuring cross-border finance transactions. One of the key reasons for this is that the Cayman Islands provides a flexible and well-tested regime for secured financing transactions that is attractive to borrowers and lenders alike. The process for creating security in the Cayman Islands is also straightforward and will not typically impact the timeframe of a proposed transaction.

In this brief guide, we address certain of the key Cayman Islands law points pertaining to the creation and protection of security over shares (the “Secured Shares”) in a Cayman Islands exempted company (the “Secured Company”).

1. Creation of security

The Companies Act (as Revised) of the Cayman Islands (the “Act”) does not contain any provisions with respect to the creation of security over Secured Shares in a Secured Company. Therefore, the security should adhere to the following principles derived from common law:

it must be in writing;

- the security document must be signed by,

- or with the authority of, the security provider; and

- the security document must clearly indicate the intention to create security over the Secured Shares and the amount secured or how that amount is to be calculated.

Cayman Islands law recognizes various forms of security over assets, including equitable mortgages and charges which are most commonly taken over Secured Shares in a Secured Company.

2. Execution formalities and regulatory approvals

Cayman Islands law does not prescribe a particular mode of execution with respect to security over Secured Shares in a Secured Company and it is not necessary for such security to be certified, notarized or apostilled to make the security valid or enforceable from a Cayman Islands law perspective. That being said, in practice, a security document with respect to Secured Shares in a Secured Company is customarily executed as a deed.

From an execution standpoint, it is important to review the memorandum of association and articles of association (the “M&A”) of the relevant security provider and the relevant Secured Company, to the extent it is a party to the security document, to ensure compliance with any applicable signing formalities.

Unless security is being taken in a Secured Company which is a “regulated person”, such as a bank or a mutual fund, no regulatory approvals are necessary to create valid and enforceable security as a matter of Cayman Islands law.

3. Stamp duty and taxes

No stamp duty or taxes are payable with respect to the creation of security over Secured Shares in a Secured Company or upon any transfer thereof in an enforcement as a matter of Cayman Islands law so long as:

- the security document and any ancillary documents thereunder are not executed or delivered in, brought into, or produced before a court of, the Cayman Islands; and/or

- the Secured Company does not have an interest in land in the Cayman Islands, or shares in a subsidiary that has an interest in land in the Cayman Islands.

4. Governing law of the security

Cayman Islands law permits security over Secured Shares in a Secured Company to be governed by Cayman Islands law or foreign law.

In cross-border finance transactions, it is relatively common for the governing law of a security document over Secured Shares in a Secured Company to be aligned with the governing law of the principal finance documents. One advantage of adopting a foreign governing law clause in a security document is that it may make available certain additional remedies (such as appropriation) which are not available under Cayman Islands law. Care should however be taken to ensure that there are no conflicts of law issues where a security document is governed by foreign law. English, Hong Kong and Singapore law are frequently adopted to govern security over Secured Shares in a Secured Company and no major conflicts of law issues are likely to arise.

Cayman Islands law governed security document

Where the security document is governed by Cayman Islands law, so long as it is in customary form, the secured party is entitled to the following remedies in the event of a default:

- the right to take possession of the Secured Shares in the Secured Company (subject to redemption by the security provider upon the settlement of the debt);

- the right to sell the Secured Shares in the Secured Company; and

- the right to appoint a receiver who may:

-

- vote the Secured Shares in the Secured Company;

- receive distributions in respect of the Secured Shares in the Secured Company; and

- exercise other rights and powers of the security provider in respect of the Secured Shares in the Secured Company.

If the secured party acquires legal title to the Secured Shares in the Secured Company, it also has a right of foreclosure. This remedy extinguishes the security provider’s legal and beneficial title to the Secured Shares in the Secured Company but not its obligation to pay any secured and unpaid sums. Foreclosure involves a time-consuming and costly court process and is not usually exercised in practice given its draconian nature.

For further details regarding the enforcement of security over Secured Shares in a Secured Company, please refer to our guide entitled “Enforcing security over shares in a Cayman Islands exempted company”.

Foreign law governed security document

Where the security document is governed by foreign law, the:

i. security document should comply with the requirements of its governing law to be valid and binding; and

ii. remedies available to a secured party are governed by the governing law and the terms of the security document.

5. Application of proceeds of enforcement

Subject to any provisions to the contrary in the security document, all amounts that accrue from the enforcement of the security document are applied in the following order of priority:

- firstly, in paying the costs incurred in enforcing the security document;

- secondly, in discharging the sums secured by the security document; and

- thirdly, in paying any balance due to the security provider.

6. Security deliverables

The terms of a well-drafted Cayman Islands law governed security document with respect to Secured Shares in a Secured Company and the principal finance document will usually require the security provider to deliver the following documents to the secured party to assist with an enforcement:

- any original share certificate(s) with respect to the Secured Shares in the Secured Company;

- an undated share transfer form with respect to the Secured Shares in the Secured Company;

- an undated resignation letter from each director of the Secured Company;

- a letter of authorization from each director of the Secured Company authorizing the secured party to date each undated letter of resignation upon the occurrence of a default under the security document;

- an irrevocable proxy with respect to the Secured Shares in the Secured Company in favor of the secured party;

- a letter of instruction to the Secured Company’s registered office service provider containing, among other things, directions to register a transfer of Secured Shares in the Secured Company upon the occurrence of a default under the security document;

- a letter of acknowledgement from the registered office service provider with respect to the instructions referenced in the letter of instruction;

- if the security provider is a Cayman Islands exempted company, a certified copy of its register of mortgages and charges showing the security created over the Secured Shares in the Secured Company (see further below);

- a certified copy of the Secured Company’s register of members annotated to show the security created over the Secured Shares in the Secured Company (if commercially agreed – see further below);

- if the security provider is a Cayman Islands exempted company, a copy of the board resolutions of its board of directors authorizing:

a. its entry into and execution of the security document; and

b. the updates to its register of mortgages and charges;

- a copy of the board resolutions of the Secured Company authorizing:

-

- its entry into and execution of the security document (if it is a party);

- its register of members to be annotated (if commercially agreed); and

- a transfer of Secured Shares in the Secured Company upon the occurrence of a default under the security document; and

xii. a special resolution passed by the Secured Company with respect to certain changes to its M&A, if required (see further below).

7. Security protection steps

Register of mortgages and charges of a Cayman Islands security provider

Pursuant to section 54 of the Act, if the security provider is a Cayman Islands company, it must record particulars of the security created over any Secured Shares in the Secured Company in its register of mortgages and charges. The register of mortgages and charges must include:

- a short description of the property mortgaged or charged;

- the amount of charge created; and

- the names of the mortgagees or persons entitled to such charge.

There is no statutory timeframe within which the register needs to be updated. However, a well-advised secured party will request that the register is updated promptly so that third parties that inspect it are on notice of the security.

Any variations and releases of charge should also be reflected in the register of mortgages and charges.

As there is no statutory regime for registering security interests under Cayman Islands law, the common law rules of priority continue to apply. In general terms, these rules specify that priority between competing security interests is determined by the dates on which the relevant security interests were created. It is important to note that inserting details of mortgages and charges in the register of mortgages and charges of a Cayman Islands company does not confer priority on a charge in respect of the relevant secured asset.

Register of members of the Secured Company

A Secured Company may annotate its register of members to include:

- a statement that security has been created over the Secured Shares;

- the name of the secured party; and

- the date on which the statement and the secured party’s name are entered in its register of members.

Although it is optional to annotate a Secured Company’s register of members with details of any security that has been created, this puts third parties that inspect the register on notice of the security. Therefore, a secured party usually insists on this.

M&A of the Secured Company

A secured party will usually request the Secured Company to make certain changes to its M&A to ensure, among other things, that there are no restrictions on the transfer of Secured Shares in the Secured Company which may impede enforcement action. Any changes to the Secured Company’s M&A must be made by passing special resolutions. Although such resolutions need to be filed with the Registrar of Companies of the Cayman Islands within 15 days of being passed, they take effect upon signing.

This publication is not intended to be a substitute for specific legal advice or a legal opinion. For specific advice, please contact:

Peter Vas

Partner

Loeb Smith Attorneys

Hong Kong

www.loebsmith.com

Introduction

As the regulatory requirements and cost burden increase for investment management entities in the Cayman Islands, many of our clients are looking for other offshore solutions. Under the Cayman Islands’ Securities Investment Business Act (2020 Revision) as amended, all Cayman entities carrying on securities investment business as investment managers and/or investment advisers (“SIBL Managers and/or Advisers”) are required to either (i) register with the Cayman Islands Monetary Authority (“CIMA”) as a Registered Person, or (ii) apply to CIMA for a licence in order to carry on such business. The vast majority of these SIBL Managers and/or Advisers opt for the more straightforward status of Registered Person which requires the applicant to, among other things, (i) have at least two (2) Directors, (ii) comply with continuing reporting obligations to CIMA, (iii) appoint AML officers and have a compliance manual, and (iv) pay the fee of approx. US$6,098 for first registration with CIMA and thereafter pay the same fee to CIMA on an annual basis for continued registration.

The impact of the Economic Substance Act on Cayman Investment Managers

The logistical challenges and economic costs of complying with the Economic Substance Act has also caused a substantial increase in the number of existing Cayman Islands’ Investment Managers (who exercise discretionary authority over the investments they manage) either winding down their affairs and de-registering from CIMA or restructuring their relationship with investment funds in order to deal with these challenges and control costs. It has also meant that clients looking to establish new funds in the Cayman Islands, which continue to be the premier offshore jurisdiction for establishing investment funds, are increasingly looking for new offshore options for establishing an investment management entity.

BVI Approved Manager regime

One attractive offshore option is establishing an “Approved Manager” in the British Virgin Islands (“BVI”) under the Investment Business (Approved Managers) Regulations 2012 (As Amended) (the “Regulations”) and the Approved Investment Managers Guidelines. The BVI Approved Manager regime has less onerous regulatory requirements than the licensed regime in the BVI and is similar in a number of respects to the Registered Person regime in the Cayman Islands. However, there are some crucial differences.

Key features of the BVI Approved Manager regime

i. A BVI company or limited partnership can apply to the BVI Financial Services Commission (the “FSC”) for approval as an Investment Manager and if approved would become an “Approved Manager”.

ii. The application fee payable to the FSC is US$1,000 (significantly less than the application fee of circa US$6,098 payable for an Investment Manager with Registered Person status in the Cayman Islands).

iii. An application to the FSC must be submitted at least seven (7) days prior to the intended date for the commencement of relevant business and provided the applicant makes the submission to the FSC within this time period, the applicant may commence and carry on relevant business for a period of up to thirty (30) days from the date of submission of the application (such period being extendable for a further period of 30 days by the FSC). During this 30 day (or extended) period, the applicant will be deemed to have been approved under the Regulations if ultimately approved by the FSC.

iv. Significantly, an Approved Manager does not fall within the scope of the BVI economic substance law regime.

Significantly, an Approved Manager does not fall within the scope of the BVI economic substance law regime.

v. An Approved Manager has no capital adequacy or professional indemnity insurance requirements.

vi. Under the Approved Manager regime there is a US$400 million cap on assets under management for open-ended funds and a cap of US$1 billion of capital commitments for closed-ended funds. If these limits are exceeded, the Approved Manager must inform the FSC within seven (7) days. The funds it manages can be funds in the BVI or equivalent funds in another recognized jurisdiction (e.g. the Cayman Islands, China, Switzerland, Ireland, Luxembourg, Hong Kong, Singapore, the United Kingdom, and the United States). If these limits are breached, then within three (3) months of the limit being breached, the Approved Manager is required to either (i) apply for a licence under Part I of the BVI Securities Investment Business Act, or (ii) the funds which the Approved Manager manages or advises must have decreased back below the limits otherwise it must immediately cease carrying on relevant business on the expiry of the three (3) months period.

vii. An Annual Return for the Approved Manager is required to be filed with the FSC to confirm the Approved Manager and its senior team remain in compliance with BVI regulations, along with details of the funds under management and any significant complaints received from investors.

viii. An Approved Manager is required within fourteen (14) days of the change of any information submitted to the FSC during the application process to notify the FSC in writing of the change, providing details of the change and a written declaration in the prescribed form as to whether or not the change complies with the requirements of the Regulations.

ix. Financial Statements – Annual financial statements must be submitted, however these are not required to be audited.

x. Directors – Approved Managers must retain at least two (2) directors (as is the case under the Registered Person regime in the Cayman Islands) and always have a licensed authorised representative in the BVI.

xi. Annual Fee – The Approved Manager is required to pay an annual fee of US$1,500 (significantly less than the annual registration fee of circa US$6,098 payable for an Investment Manager with Registered Person status in the Cayman Islands) to the FSC for renewal of its approval as an approved manager.

xii. Anti-Money Laundering Compliance – Unlike the position for Registered Persons in the Cayman Islands, the Approved Manager is exempt from the requirement to appoint a compliance officer. However an Approved Manager is required (i) to appoint a money laundering reporting officer (MLRO) and (ii) maintain policies and procedures with respect to client identification, record keeping, internal reporting and internal controls and communications, which meet the requirements set out in the BVI Anti-Money Laundering Regulations and the BVI Anti-Money Laundering and Terrorist Financing Code of Practice.

For specific advice on the BVI Approved Manager regime, please contact your usual Loeb Smith attorney or any of:

E: elizabeth.kenny@loebsmith.com

E: santiago.carvajal@loebsmith.com

Share to WeChat

“Scan QR Code” in WeChat and tap ··· to share.

Cayman Islands exempted companies (“Cayman Companies” and each a “Cayman Company”) are widely utilized in structuring cross-border finance transactions. One of the key reasons for this is that the Cayman Islands provides a flexible and well-tested regime for secured financing transactions that is attractive to borrowers and lenders alike. The process for creating security in the Cayman Islands is also straightforward and will not typically impact the timeframe of a proposed transaction.

In this brief guide, we address certain of the key Cayman Islands law points pertaining to the creation and protection of security by a Cayman Company over its assets. For details with respect to the creation of security over Cayman Islands shares, please refer to our separate guide entitled “Granting and protecting security over shares in a Cayman Islands exempted company”.

This guide does not consider the additional steps that may be necessary for the purposes of creating and protecting security over specific asset classes, such as Cayman Islands registered aircraft and ships, or land located in the Cayman Islands.

1. Creation of security

The Companies Act (as Revised) of the Cayman Islands (the “Act”) does not contain any provisions with respect to the creation of security over the assets of a Cayman Company. Therefore, the security should adhere to the following common law principles:

i. it must be in writing;

ii. the security document must signed by, or with the authority of, the Cayman Company; and

iii. the security document must clearly indicate the intention to create security over the relevant assets and the amount secured or how that amount is to be calculated.

Cayman Islands law recognizes various forms of security over assets, including legal mortgages, equitable mortgages, charges and assignments by way of security. The type of security interest that is created will depend on the type of asset to be secured.

2. Execution formalities and regulatory approvals

Cayman Islands law does not prescribe a particular mode of execution with respect to security over the assets of a Cayman Company and it is not necessary for such security to be certified, notarized or apostilled to make the security valid or enforceable from a Cayman Islands law perspective.

It is important to review the memorandum of association and articles of association of the Cayman Company to ensure compliance with any applicable signing formalities.

No regulatory approvals are necessary to create valid and enforceable security as a matter of Cayman Islands law in respect of security that is created over a Cayman Company’s assets.

3. Stamp duty and taxes

No stamp duty or taxes are payable with respect to the creation of security over the assets of a Cayman Company or upon any transfer thereof in an enforcement as a matter of Cayman Islands law so long as:

i. the security document and any ancillary documents thereunder are not executed or delivered in, brought into, or produced before a court of, the Cayman Islands; and/or

ii. the assets do not comprise land in the Cayman Islands, or shares in a subsidiary that has an interest in land in the Cayman Islands.

4. Governing law

Cayman Islands law permits security over the assets of a Cayman Company to be governed by Cayman Islands law or foreign law.

In cross-border finance transactions, it is relatively common for the governing law of a security document over the assets of a Cayman Company to be aligned with the governing law of the principal finance documents or the lex situs of the secured asset. One advantage of adopting a foreign governing law clause in a security document is that it may make available certain additional remedies (such as appropriation) which are not available under Cayman Islands law. Care should however be taken to ensure that there are no conflicts of law issues where a security document is governed by foreign law. English, Hong Kong and Singapore law are frequently adopted to govern security over the assets of a Cayman Company and no major conflicts of law issues are likely to arise.

Where the security document is governed by foreign law, the:

i. security document should comply with the requirements of its governing law to be valid and binding on the Cayman Company; and

ii. remedies available to a secured party are governed by the governing law and the terms of the security document.

5. Security deliverables

The Cayman Company will typically be required to deliver the following documents to the secured party under the terms of the relevant security document and/or the other finance documents:

i. a certified copy of its register of mortgages and charges showing the security created over the secured assets (see further below); and

ii. a copy of the board resolutions of its board of directors authorizing:

a. its entry into and execution of the security document; and

b. the updates to be made to its register of mortgages and charges.

6. Register of mortgages and charges

Pursuant to section 54 of the Act, a Cayman Company must record particulars of the security created over any of its assets in its register of mortgages and charges. The register of mortgages and charges must include:

i. a short description of the property mortgaged or charged;

ii. the amount of charge created; and

iii. the names of the mortgagees or persons entitled to such charge.

There is no statutory timeframe within which the register needs to be updated. However, a well-advised secured party will request that the register is updated promptly so that third parties that inspect it are on notice of the security.

Any variations and releases of charge should also be reflected in the register of mortgages and charges.

A copy of the register of mortgages and charges (including a blank register if no prior security has been granted) must be kept at the registered office of the Cayman Company and is a private record that is not open to inspection by the public. However, any creditor or member of the Cayman Company may inspect the register at all reasonable times.

If a Cayman Company does not comply with the aforementioned provisions, every director or officer who authorizes or knowingly and willfully permits such non-compliance is liable to a penalty. This does not invalidate the validity, enforceability or the admissibility in evidence of the charge, however.

As there is no statutory regime for registering security interests under Cayman Islands law, the common law rules of priority continue to apply. In general terms, these rules specify that priority between competing security interests is determined by the dates on which the relevant security interests were created. It is important to note that inserting details of mortgages and charges in the register of mortgages and charges of a Cayman Company does not confer priority on a charge in respect of the relevant secured asset.